{kind=link}

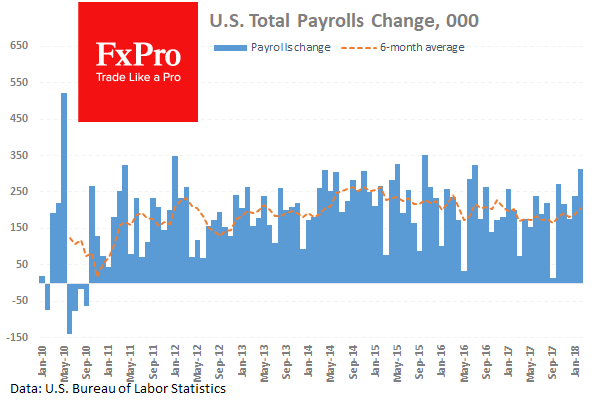

The US Nonfarm Payrolls data released on Friday showed a strong increase in job creation and, combined with the lower than expected increase in Hourly Earnings, sent the markets into risk-on mode. This was a complete reversal of the previous month’s reaction to this data series when positive sentiment evaporated as fears of inflation and interest rate hikes took over. This time, data indicated that the labour market, despite being the tightest it has been in decades, is not putting pressure on wages and, therefore, keeping inflation low. US stock markets roared higher with the Dow up 440 points or 1.77%, the NASDAQ up 1.79% and S&P 500 up 1.74%. Treasury Yield moved higher, as the expectation of 4 rate hikes increases but at a gradual pace. The US dollar was weaker against the AUD, NZD, CAD and GBP but managed to gain against the JPY.

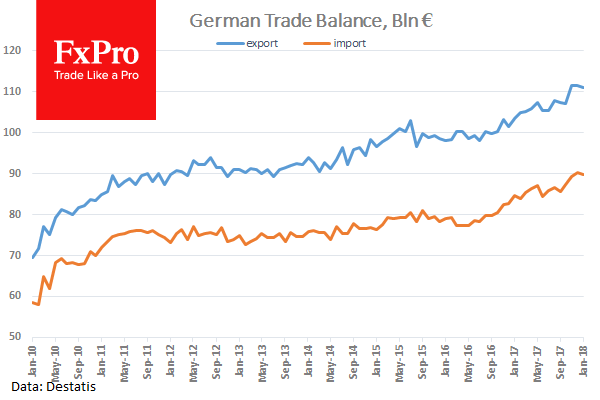

German Current Account n.s.a. (Jan) was €22.0B v an expected €17.2B against a previous €27.8B. Exports (MoM) (Jan) were -0.5% v an expected 0.3%, against 0.3% previously. Imports (MoM) (Jan) were -0.5% v an expected 0.0%, against 1.4% previously. Trade Balance s.a. (Jan) was €21.3B v an expected €21.1B, against a prior €21.4B. The trade balance is showing a slight fall but is inside normal range, with imports down and exports steady. EURUSD fell from 1.23209 to 1.23108.

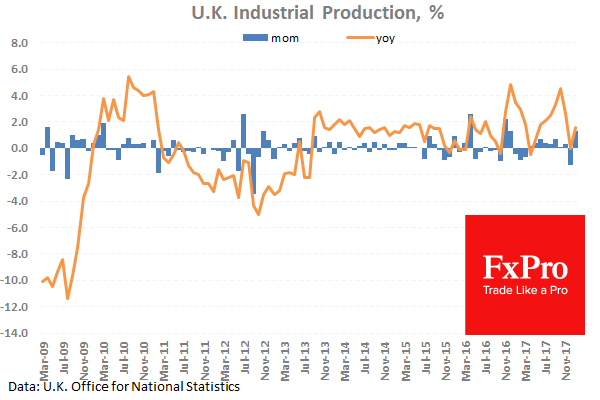

UK Industrial Production (YoY) (Jan) was 1.6% v an expected 1.8%, against a previous 0.0%. Manufacturing Production (MoM) (Jan) was 0.1% v an expected 0.2%, against 0.3% previously. This figure had been less volatile during much of 2017, with readings staying positive but close to zero. Industrial Production (MoM) (Jan) was 1.3% v an expected to be 1.5%, against -1.3% previously. Seasonally, there is generally a downturn in this figure, with a drop in negative territory early in the New Year. This month’s number shows strong performance and is one of the best March readings on record, even if it did miss expectations. Manufacturing Production (YoY) (Jan) was 2.7% v an expected 2.8%, against 1.4% previously. GBPUSD moved between a high of 1.38152 and a low of 1.38014 because of this data release.

UK NIESR GDP Estimate (3M) (Feb) was as expected at 0.3%, against 0.5% prior, which was revised down to 0.4%. The data point has been moving closer to 0.0% since hitting a high of 1.0% in May 2014. However, it has managed to remain positive in that time, with a 0.4% average. GBPUSD reached a high of 1.38407 but fell to a low of 1.38426 after this data release.

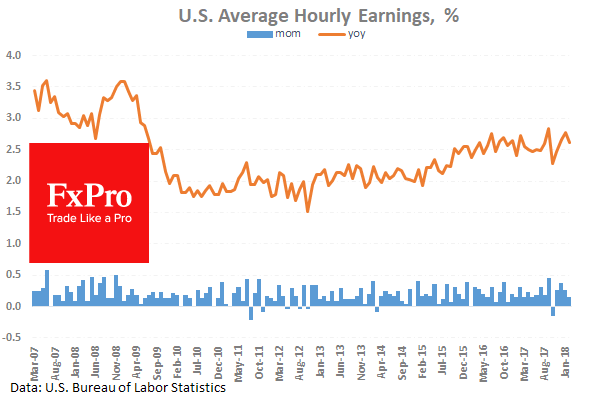

US Non-Farm Payrolls (Feb) beat the consensus, coming in at 313K against an expected 200K, from a prior 200K, which was revised up to 239K. The Unemployment Rate (Feb) was 4.1% v an expected 4.0%, with a prior of 4.1%. This measures the percentage of the total workforce unemployed and actively seeking employment during February. Average Hourly Earnings (YoY) (Feb) was 2.6% v an expected 2.8%, against 2.9% previously, which was revised down to 2.8%. Average Weekly Hours (Feb) was 34.5 v an expected 34.4, against a previous 34.3. Labour Force Participation Rate (Feb) was 63.0% v an expected 62.5%, against a prior reading of 62.7%. Average Hourly Earnings (MoM) (Feb) was 0.1% v an expected 0.2%, against 0.3% previously. It was this data release on the 2nd of February that resulted in the pullback in equity markets last month. On Friday, the opposite occurred, as the combination of strong job creation but low hourly earnings hit a sweet spot for markets and eased fears of higher inflation. EURUSD tested lows at 1.22732 before moving higher to 1.23339, while the S&P 500 rallied from 2733.60 to close the day at highs of 2783.70 due to these data releases.

Canadian Unemployment Rate (Feb) was 5.8% v an expected 5.9%, against a previous 5.9%. Participation Rate (Jan) was 65.5% v an expected 65.6%, against 65.5% prior. Net Change in Employment (Dec) was 15.4K v an expected 20.0K, against a prior -88.0K. Unemployment in Canada is hovering around the lowest levels in ten years. GBPCAD fell from 1.77960 to a low of 1.77374 after this data came out.

Baker Hughes US Oil Rig Counts was released with a headline number of 796, down from last week’s number of 800. WTI Oil can become volatile around this data release and will be in traders’ minds when trading resumes on Monday.

EURUSD is up 0.13% overnight, trading around 1.23197.

USDJPY is down -0.17% in early session trading at around 106.634.

GBPUSD is up 0.08% this morning, trading around 1.38603.

Gold is largely unchanged in early morning trading at around $1,322.90.

WTI is unchanged this morning, trading around $61.85.