{kind=link}

Canadian Highlights

- Next Monday’s federal election will be the show stealer. The Liberals are ahead in the polls, and if they do indeed prevail, we could see more government spending than what we baked into our forecast.

- Even with a potential government stimulus boost, the economy is still likely poised to sour in the coming months. We expect that will lead the Bank of Canada to trim its policy rate.

- February was a soft month for consumer retail spending. March looks to have been a firmer month, but we’re retaining our view that consumption is headed for a slowdown.

U.S. Highlights

- Trade tensions between the world’s two largest economies simmered this week, with the U.S. administration hinting that the tariffs on China would likely be lowered in the very near future.

- But President Trump appeared frustrated with the lack of progress among other countries, and threatened to reimpose the reciprocal tariffs in the coming weeks if trade deals weren’t signed.

- Amidst all the uncertainty, the housing recovery appears to be on hold. Existing home sales declined to a six-month low in March.

Canada – Election Anticipation

Some optimism returned to Canadian financial markets this week. Equities breathed a sigh of relief, with the TSX on track to rise about 2.5% on the week. President Trump signaled a de-escalation of the U.S. trade war with China and assured that he would retain Federal Reserve chief Powell, despite disagreeing with his stance on monetary policy (to put it lightly). Bond yields were also slightly higher at time of writing, although the Canadian dollar dipped a touch on the back of some upward movement in the USD. It wasn’t completely smooth sailing, however, with the U.S. President warning that the 25% tariff in place on cars imported from Canada could go up. He also re-iterated some of his grievances with his northern neighbour when questioned about the upcoming Canadian election.

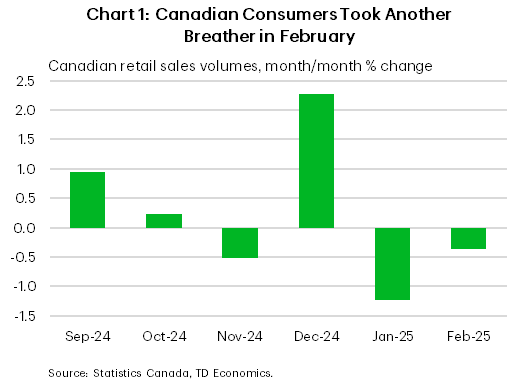

This week also offered a pulse-check on the state of the Canadian consumer via the February retail spending report, and the results were less than encouraging. Retail sales volumes declined 0.4% month-on-month, pulled down by weakness in new vehicle purchases (which continued to pullback after surging in the back half of last year) and housing-related sales (mirroring the weakness in the housing market). Some of the drop in overall sales volumes may have been weather-related given major winter storms that took place that month. Still, it marked the second straight monthly decline (Chart 1). Statcan’s flash estimate showed a 0.7% m/m rebound in March, but given all of the headwinds facing the consumer, we still expect spending growth to cool moving forward.

All eyes are on next Monday’s federal election. It’s a two-horse race between the Liberals and Conservatives, with both parties releasing their costed platforms this week. Net new stimulus measures in the Liberal plans amount to an average of about 1% of GDP over the forecast horizon, driven by spending and abetted by tax cuts. In contrast, tax reductions are the name of the game for the Conservatives, with relief pledged for household incomes, housing, and seniors to name a few. On the opposite side of the ledger, the Conservatives are pledging to scale back spending slightly, instead leaning on a bevy of tax cuts to support the economy and, ultimately, grow revenues. The Liberal plan sees the deficit averaging about 1.7% of GDP over the next several years. It’s lower under the Conservative plan, but the party included a projected boost to revenues from the anticipated lift to economic growth from their new measures, which is something the Liberals largely didn’t do.

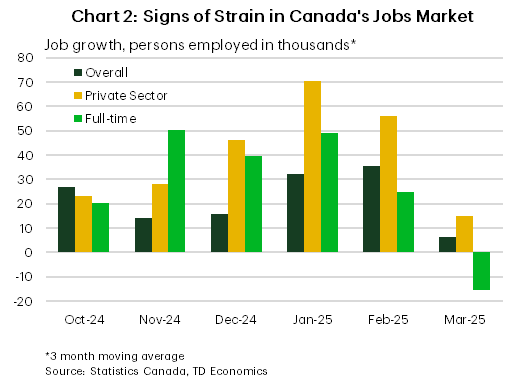

As of now, polling and betting markets are leaning towards a Liberal victory. If that occurs, there is some upside risk to our assumption that fiscal stimulus across all levels of government would amount to 1% of GDP. All else equal, a larger-than-expected dose of government stimulus could offer a boost to the economy. However, a large chunk of new spending in the Liberal plan is capital investment, and so could take longer to have an impact on the economy as projects take time to get up and running. More importantly, the economy is likely to sour in short order, with next week’s GDP report set to show that growth softened in February and Canada’s labour market already displaying signs of cooling (Chart 2). As such, the Bank of Canada remains on course to trim their policy rate in the coming months.

U.S. – Searching for the Signal Amidst A Lot Of Noise

Disentangling the signal from the noise on U.S. trade matters is becoming an increasingly difficult task. This week, President Trump and U.S. Treasury Secretary Scott Bessent both called out the tariffs on China as being “too high”. At 145%, Bessent said trade with China becomes “unsustainable” and that he expects the current situation to de-escalate in the “very near future”. China appears open to negotiations and even went as far as exempting some U.S. goods from its retaliatory tariffs. The abrupt U-turn in the administration’s tone alongside President Trump’s assurance that he will not remove Fed Chair Powell, helped to fuel a mid-week rally in U.S. equities, with the S&P 500 ending the week up 3.5%. But investors remained skeptical of whether the move to de-escalate was the beginning of a broader pivot or simply backpedaling on the overly punitive levies imposed on China given the significant economic repercussions.

Despite claims of over 90 countries having offered to negotiate trade terms, President Trump appears to be growing frustrated with the lack of progress made on reaching deals. He even went as far threatening to re-impose the “reciprocal” tariffs on some countries over the coming weeks if trade deals weren’t signed.

But even if there’s a big push on trade negotiations over the coming weeks, at least some economic damage has already been done. In the April release of the Federal Reserve’s Beige Book, several districts noted a considerable worsening in the economic outlook amid heightened uncertainty stemming from tariffs. Spending on both business and leisure travel were down, with some districts seeing an outright decline in international visitors. On inflation, many businesses noted that they’re already seeing input costs rise and that they expect to pass-on at least some of the additional costs to consumers. But this may not be possible for some consumer-facing sectors, who are already reporting more tepid demand.

Estimates done by Reuters suggest that of the S&P 500 companies who have already reported quarterly earnings, over 90% have mentioned tariff risks in their earnings transcripts. This is more than double what was mentioned the prior quarter and underscores how today’s uncertainty is touching nearly all industries. This does not bode well for capital spending.

The housing recovery is also looking to be on hold. Existing home sales declined 5.9% m/m in March, falling to a six-month low of 4.0 million units (Chart 1). With mortgage rates again within spitting distance of 7%, and households increasingly worried about employment prospects, we’re likely to see a further pullback in sales activity over the coming months. Construction activity was also sharply lower in March, amid elevated trade uncertainty and higher input costs. Homebuilder confidence for April remained soft, suggesting little rebound in near future.

Our current tracking for first quarter real GDP (released April 30th) suggests economic growth grew by just 0.3% annualized after expanding by an above trend pace of 2.9% through the second half of 2024 (Chart 2). But the GDP release will play second fiddle to next week’s more timely April jobs report. Expectations are that the economy added 130k jobs in April, a meaningful stepdown from March’s 228k pace.