{kind=link}

Canadian Highlights

- The Bank of Canada held the policy rate at 2.75% and, in a break from tradition, refrained from publishing its usual forecast.

- The Monetary Policy Report outlined two illustrative scenarios depending on different U.S. tariff policy paths. Both marked a downgrade from January’s projections.

- Economic data released this week showed that the housing market continues to crack, while inflation edged lower.

U.S. Highlights

- News on the trade front this week included the U.S. administration tightening rules on chips exports to China and promising tariffs on imports on electronics in the near future.

- Retail sales report showed that the prospect of tariff-driven price hikes spurred consumers to go on a pre-emptive shopping spree in March to replace aging vehicles and stock up on materials for home renovations.

- Fed Chair Jerome Powell acknowledged the trade conflict presents a “challenging scenario” for the central bank, but re-iterated that the central bank was “well positioned to wait for greater clarity”.

Canada – Monetary Policy Can’t Fix a Trade War, All Eyes on Fiscal Policy

For a short Easter week, there was no shortage of eggs to crack open, but the biggest one was the Bank of Canada’s decision and the accompanying Monetary Policy Report (MPR). After cutting interest rates for the past seven consecutive announcements, the Bank chose to hold the policy rate steady at 2.75%. The Bank pointed out that it had already reduced interest rates 25 basis points in both January and March in the face of tariff uncertainty, but with the path ahead no clearer decided to leave the policy rate unchanged “as we gain more information about both the path forward for US tariffs and their impacts”. The Loonie edged higher on the news, while both bonds and equities posted modest gains.

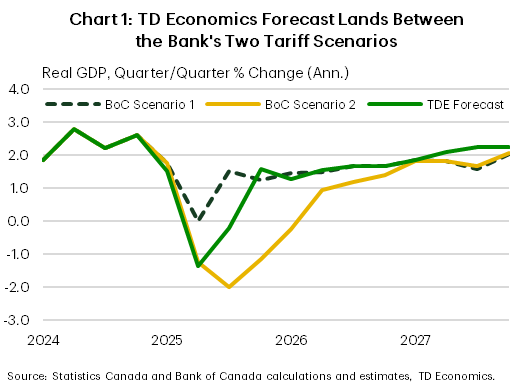

In a break from tradition, the Bank didn’t lay its usual forecast egg. Instead, it offered two illustrative scenarios that explore different paths for U.S. tariff policy. This isn’t the first time the Bank has skipped publishing point forecasts. Five years ago, during the early days of the pandemic, it omitted its usual projection tables and instead offered illustrative scenarios, with outcomes tied to how quickly the virus would recede. This time, the outlook hinges on trade policy. Scenario 1 assumes limited tariffs, weaker growth, and inflation sticking close to 2%. Scenario 2 involves a full-blown year-long trade war, resulting in a recession in both Canada and the U.S. and inflation rising to 3% by 2026. Our own forecast, which assumes tariffs remain in place for six months, lands roughly in the middle (Chart 1).

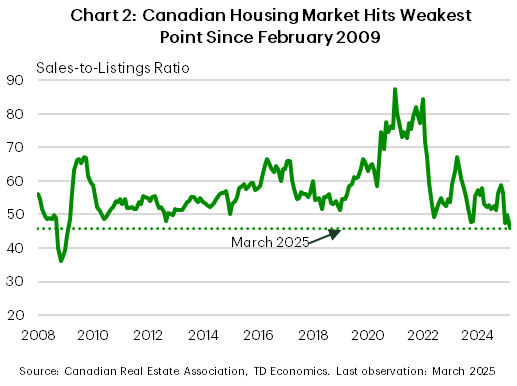

Either way, both scenarios mark a downgrade from January’s MPR. And the Bank acknowledged that the real economy is already softening. The labour market has weakened, and consumer and business recession expectations have risen. Now the housing market has cracked: a combination of weaker sales and rising listings pushed the national sales-to-new listings ratio down to 45.9% in March — a buyer’s market and the lowest level since February 2009 (Chart 2).

On the inflation front, the Bank expects “tariffs and supply chain disruptions to push up some prices”, but this will depend on the evolution of tariffs and how quick businesses are to pass on costs. March CPI offered some relief, with cheaper gas and travel tour prices easing year-over-year inflation, despite upward pressure from the full reinstatement of the GST/HST. The Bank now expects inflation to dip further in Q2, due to the elimination of the consumer carbon tax and lower global oil prices. In both scenarios, tariff-related inflation is expected to peak next year. From an inflation risk perspective, the Bank sees a fairly balanced outlook, with potential supply chain disruptions and higher inflation expectations on the upside, and a weaker-than-expected economy and financial stress on the downside.

Still, it’s fair to ask: why pause rate cuts now, when inflation is relatively under control and its risks balanced, while growth clearly tilting lower? We think the answer lies in policy uncertainty. The Bank is waiting for more clarity on what tariffs look like and the fiscal policy response—something that won’t arrive until after the election on April 28th. As the Bank has pointed out, monetary policy cannot offset the impacts of a trade war, nor can it resolve policy uncertainty. The Bank doesn’t want to count its chickens before they hatch and for now, caution is the name of the game.

U.S. – Tariffs Create A “Challenging Scenario” For The Fed

Trade policy developments remained in sharp focus during this holiday-shortened week. Markets continued to be whipsawed by what have become near-daily updates on the trade front. Investors breathed a sigh of relief after news broke that some electronics imports from China would be exempt from the 145% tariff, and instead only face the smaller 20% IEEPA tariffs. However, the relief was short lived as both President Trump and Commerce Secretary Lutnick noted that these products will fall in scope under the broader Section 232 review of semiconductors, which is likely to be announced over the coming weeks/months. In blow to the tech industry and advanced manufacturing, the U.S. tightened the rules on exports of chips to China, produced by Nvidia and ADM.

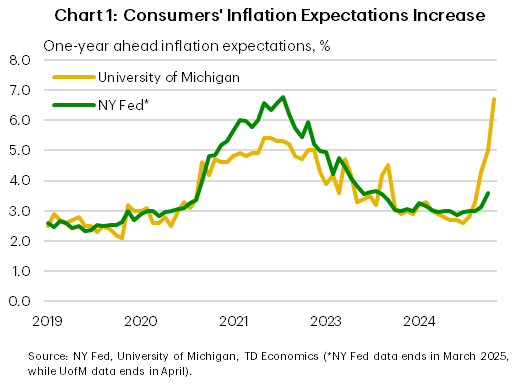

The market selloff intensified following comments from Fed Chair Jerome Powell, who acknowledged the trade conflict presents a “challenging scenario” for the central bank. With tariffs likely to push prices higher while slowing economic growth, the Fed faces a tough choice: maintain elevated interest rates to support price stability or cut rates to support the labor market. Powell offered no clear guidance. However, recent communications from Fed officials suggest rising inflation expectations and steeper-than-expected tariffs have the FOMC more concerned about long-term inflation risks and willing to tolerate some economic softening (Chart 1).

Anticipation of higher prices may already be influencing consumer behavior. Wednesday’s retail sales report showed that the prospect of tariff-driven price hikes spurred a pre-emptive shopping spree in March. Retail sales jumped 1.4%, as consumers rushed to dealerships and stores to replace aging vehicles and stock up on home renovation materials. Sales of vehicles and auto parts, as well as building materials and equipment, saw strong gains. A pull-forward in demand was also evident in electronics and sporting goods.

Some of this behavior may carry over into April, spurred by the intensifying trade dispute with China. However, we expect it to mark a final burst before consumers begin tightening their purse strings as the price impacts from tariffs are passed onto the consumer and erode household purchasing power. Based on the rates announced to date, we estimate the average household will face an increase in living costs of approximately $3,600 per year. Tax cuts could provide some offset. If President Trump’s promised tax cuts are fully implemented, we estimate that it would lift household’s income by around $2,700. This is $900 short of offsetting the tax hike from tariffs, leaving the average household worse off.

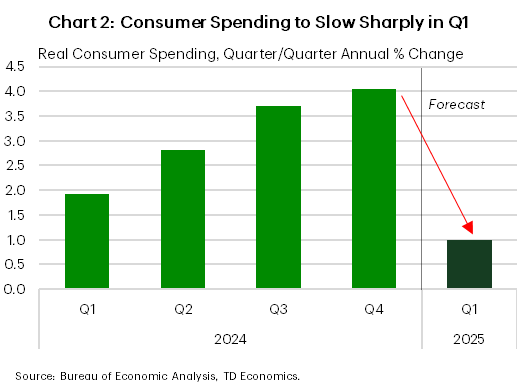

A hit to household wealth, higher goods prices and rising unemployment down the road rate will put the brakes on spending. A notable slowdown is likely to show up in Q1, with consumer spending expected to expand by just 1% (annualized) – down sharply from 4.0% in Q4 of 2024. A further softening in Q2 is looking increasingly likely (Chart 2). Without the backing of strong consumer spending, the U.S. economic engine could sputter this year. While we still believe a recession can be avoided, risks to the outlook are increasingly tilted to the downside.