{kind=link}

Above-target inflation and relatively robust activity growth have allowed the Bank of Japan to slowly step away from the zero lower bound. But Japan now faces the challenge of negotiating a trade agreement with the US while trying to support the confidence that has been key to this success.

The world has shifted monumentally since the Bank of Japan’s last meeting. Above-target inflation and relatively robust activity growth has allowed the Bank to slowly step away from the zero lower bound. But Japanese authorities are now faced with the challenge of negotiating a trade agreement with the US while supporting the confidence that has been so critical to their success with inflation and growth. Success will be critical if the policy rate is to reach the 1.0% ‘neutral’ terminal rate as hoped.

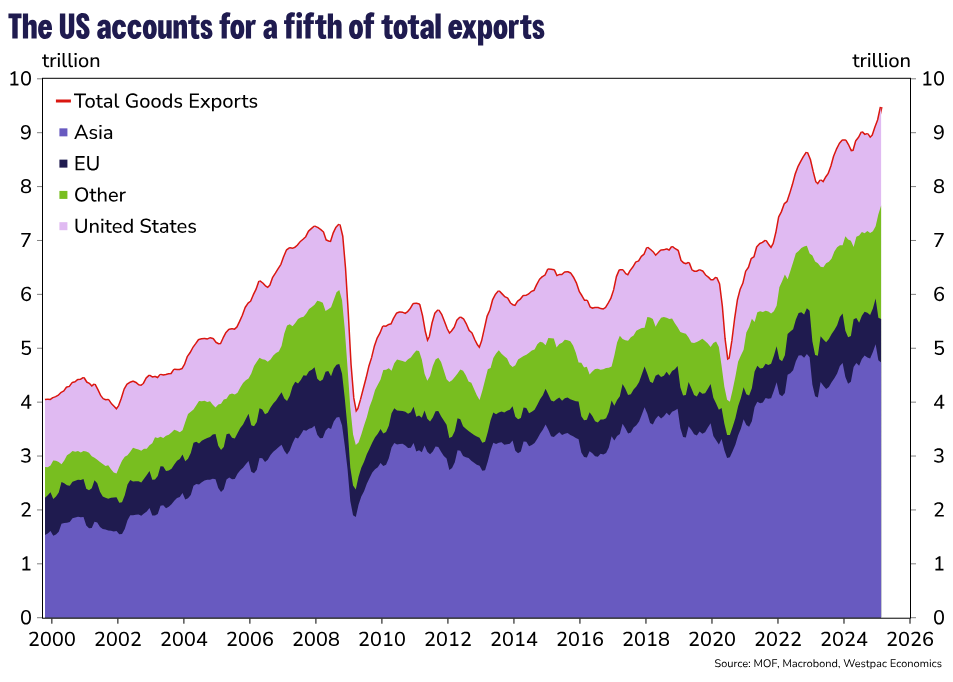

In considering what is at stake for the Japanese economy, it is worth contextualising the US-Japan trade relationship and its links to the domestic economy. Just over 20% of Japan’s goods exports go to the US, over 70% of which is machinery and transport equipment, an industry that accounts for 15% of GDP. The OECD estimates that the value added in exports to the US equate to 2% of Japan’s GDP.

The US ‘reciprocal’ tariffs included a 24% tariff on Japanese goods. The 90-day pause has set that back to 10% with the whole tariff reportedly up for negotiation. Any Japanese deal is likely to see some of its manufacturing relocated to the US in exchange for softer tariffs.

At present, many Japanese companies have factories across Asia to capitalise on cheaper labour. We have previously argued this poses structural downward pressure on the yen as earnings from these subsidiaries are often reinvested back into offshore operations instead of being repatriated. Increased investment by Japan into US auto manufacturing is likely to be a key part of the expected agreement.

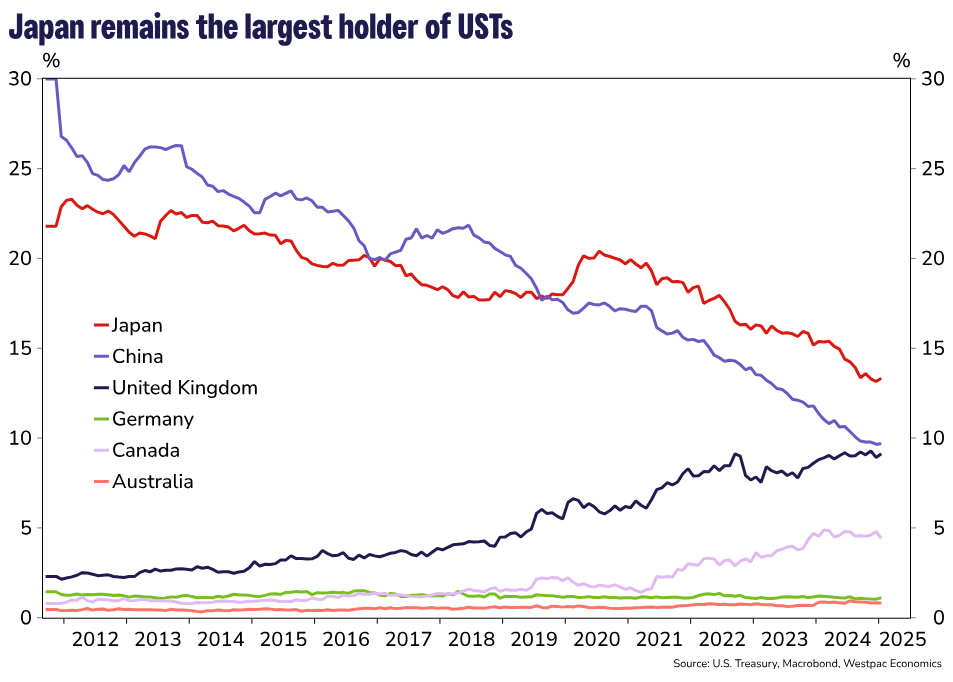

Japan comes to the negotiating table with its own strengths. Japan is the second largest holder of long-term US securities. US holdings of Japanese securities are about half that of Japanese holdings of US securities. Japan is also currently the largest single-country holder of US Treasuries according to US Treasury International Capital data. Looking ahead, the US will need buyers for its Treasuries as deficits persist and if, as Westpac Head of Financial Markets Strategy Martin Whetton noted, US government bonds erode their status as a safe haven, this task will become increasingly difficult. Japan’s status as an ‘investor to the developed world’ will likely hold significant weight in these negotiations, even if a pledge to continue investing in Treasuries is not explicitly made.

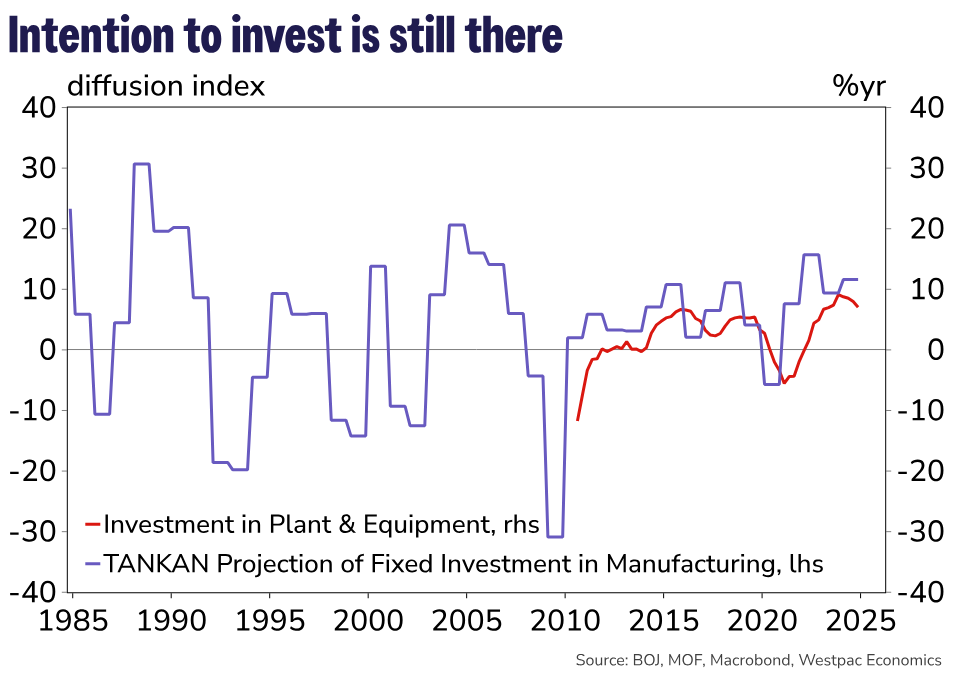

The manufacturing sector has been a bedrock of the Japanese economy for decades. Looking ahead, with a declining population, it is difficult to see output in the economy expanding on the back of services alone, which tends to be quite labour intensive with moderate-to-low marginal returns on capital. Investment into efficient manufacturing and strength in exports will be a key support of economic growth for years to come and is required for a neutral monetary policy rate meaningfully above the zero-lower bound to be sustained. While the fruits of productive expansion may seem like a thought for the distant future, the investment needed to yield those outcomes is required now.

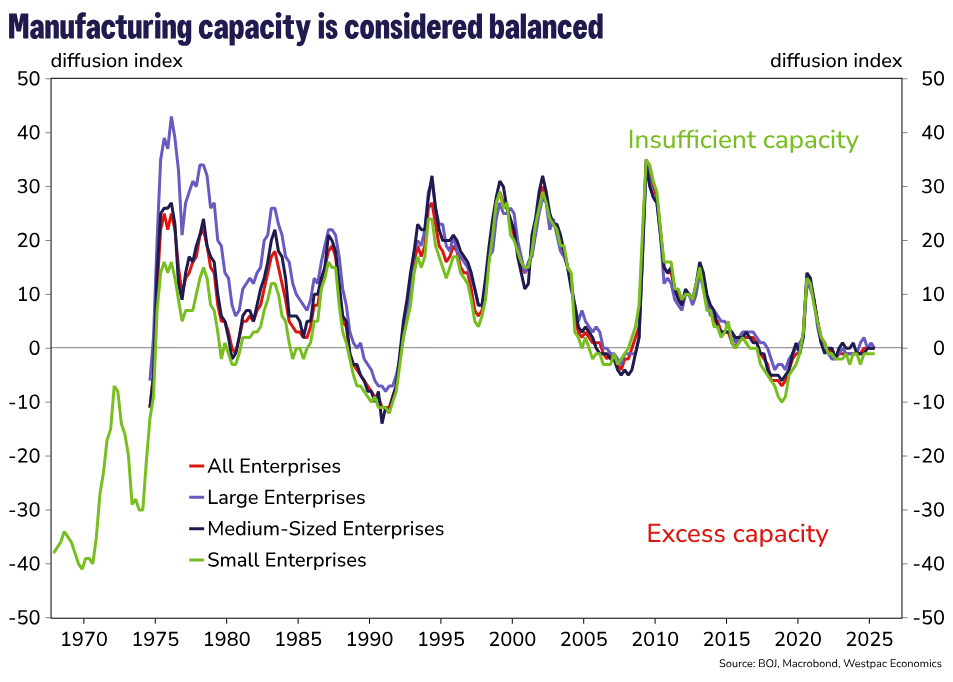

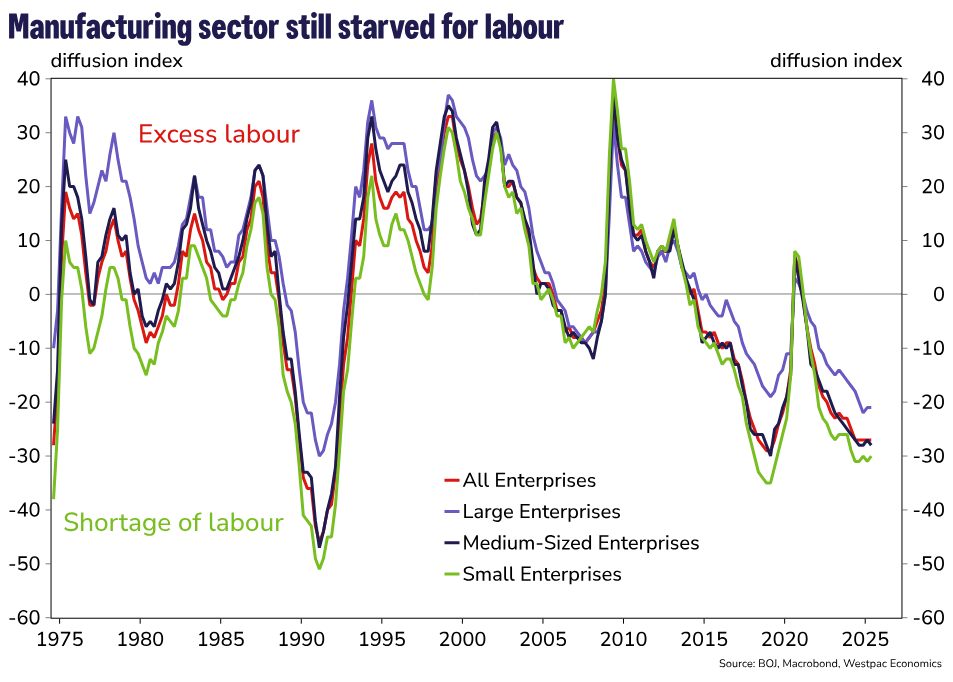

Crucially, it is confidence amongst Japanese businesses that will help the nation realise its economic potential. The latest Tankan results, which were collected prior to recent trade developments, showed manufacturing firms expect a relatively higher degree of labour shortages versus history and a net neutral assessment of productive capacity in the future. That is, there is no expectation for excess capacity across the manufacturing sector.

Sentiment around investment, as reported in the annual survey in December, was near the pre-Asian financial crisis peak. Japanese businesses have also walked the walk – investment in plant and equipment has not been this high on a sustained basis since data collection began in 2010. The appetite for investment has certainly been there but it may have been lost in the chaos of the US tariff shock.

Maintaining business confidence through successful trade negotiation with the US will be crucial in determining how the path for policy evolves. Despite the enormity of the challenge, we anticipate Japan’s strong position as an exporter of manufactured goods and net lender to the world will help secure favourable terms for Japan-US trade with limited concessions.

Our baseline view is that tariffs on Japanese goods remain capped at 10%, explicitly or implicitly in exchange for continued purchases of US Treasuries and further investment and collaboration between Japan and the US in the auto industry.

We now anticipate that the Bank of Japan will raise rates once more in 2025 at the July meeting and again in March 2026 to a 1.0% terminal rate. By July, there should be greater clarity on trade policy in the US as well as Japanese domestic policy as it relates to the House of Councillors elections. From there, the outlook is predicated on how businesses adapt to a new world of tariffs and whether this hampers their ability to raise wages for FY2026. Another strong wage print will help justify the case for a final hike in 2026.