{kind=link}

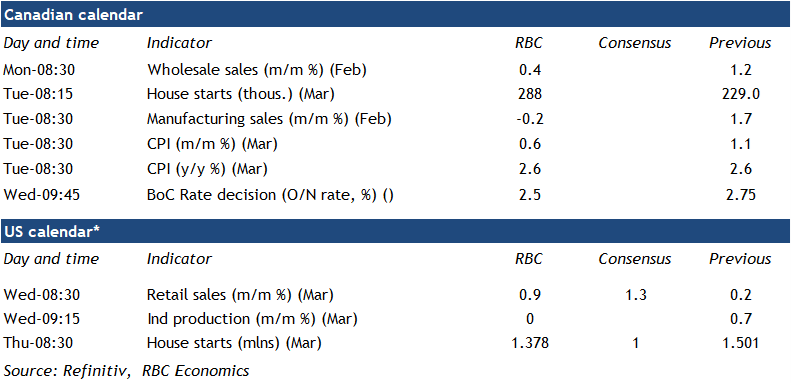

Wednesday’s interest rate decision for the Bank of Canada will be another close call for policymakers, but we expect they will ultimately opt to add another “insurance” 25 basis point cut in the face of escalating U.S. tariff risks.

Minutes from the last BoC meeting largely confirmed that the central bank would have foregone a cut to the overnight rate in March if not for heightened trade risks. We continue to think that fiscal policy is better positioned to provide the kind of timely, targeted, and temporary support needed for the economy as needed than changes in interest rates.

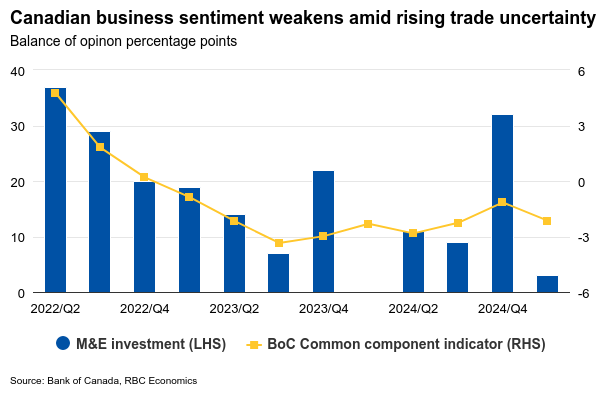

Our tracking of consumer spending has been more resilient than the plunge in consumer confidence measures in March alone would suggest. But, business investment and hiring intentions have weakened considerably with employment plans falling below pandemic-era lows in the BoC’s Q1 Business Outlook Survey . About 32% of firms surveyed now expected a recession in the next 12 months, up from 15% in the previous quarter. March employment data reinforced these concerns with the job count falling and unemployment rising. And, housing markets have shown clear signs of slowing—reducing the odds that near-term interest rate hikes will lead to another round of surging house prices.

Complicating the BoC’s decision is inflation has broadly surprised to the upside in recent months. We expect March’s headline inflation will hold at 2.6% year-over-year on Tuesday, matching February’s rate with lower gasoline prices in March offset by further unwinding of the GST/HST tax holiday that ended mid-February. Much of that increase outside of the drop in fuel costs is expected to show up in after-tax prices for restaurant meals.

Week ahead data watch

U.S. retail sales likely bounced back in March, fueled by a 10% jump in unit auto sales as buyers rushed to get ahead of tariffs imposed on motor vehicles starting in April. Sales at gasoline stations likely declined on lower prices at the pump.

Canadian housing starts are anticipated to come in at 288,000 in March, up from 229,000 in February. This partly reflects a rebound from a weather-induced drop in February, while building permits have been exceptionally strong this year.

We expect Canadian core wholesales sales to tick up 0.4% in February, in line with Statistics Canada’s preliminary estimate, and slower than 1.2% growth in the prior month. Most of that growth was supported by higher sales in the machinery, equipment and supplies’ subsector.

Canadian manufacturing sales likely dipped 0.2% in February, following a solid print (1.7%) in January. The largest sales declines came from the food, petroleum and coal subsectors.