to 3.93%.){kind=link}

Canadian Highlights

- Canada initially appeared to have dodged tariffs on Trump’s Liberation day. But still facing three separate tariff actions, Canada’s effective tariff rate is close to 10%.

- Canada’s job market is already starting to show some softness, with net job losses and a higher unemployment rate in March.

- The jobs data has shifted market expectations towards an interest rate cut in April. We think further support is needed for Canada’s economy.

U.S. Highlights

- The U.S. announced sweeping ‘reciprocal’ tariffs due to go into effect over the next week, with all countries exporting to the U.S. soon to be subject to double digit surcharges.

- The employment report for March showed 228k new jobs added, illustrating robust health in the labor market prior to the recent volatility.

- Federal Reserve officials, including Chair Powell, noted that recent tariffs would add upside risks to inflation.

Canada – Trump’s Tariffs Sideswipe Markets

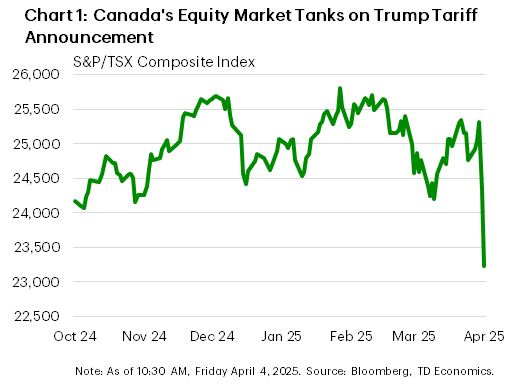

President Trump’s dreaded “Liberation Day”, saw the President make good on his campaign promise for a 10% universal tariff. Some countries received higher levies based on a bizarre calculation of trade “barriers” based on the size of the goods trade deficit with the U.S., with rates as high as 46% for Vietnam and 20% for the EU. Investor sentiment soured quickly; with many forecasters predicting the levies would tip the U.S. economy into recession. Global equity markets saw their largest one-day drops since 2020 on Thursday, with Toronto’s S&P TSX index dropping 3.8% (Chart 1). We don’t view this as an overreaction. We were not alone in pointing out that the market’s initial euphoria over Trump’s election win seemed to be favouring the economic positives of tax cuts and deregulation, rather than the disruption of upending 80 years of U.S. trade policy.

For Canada, there was some initial relief that we were not hit with any reciprocal tariff (see commentary). But zooming out, Canada already faces an effective tariff rate around 10%, depending on the degree of USMCA compliance among goods exports. Canada faces three separate 25% import tariffs: the 25% “fentanyl/illegal immigration” tariff, with 10% on energy and potash with a carve out for goods that are USMCA compliant, the 25% steel and aluminum tariff and a 25% tariff on finished vehicle imports. Fortunately, it is estimated that 80-90% of exports can become USMCA compliant, which would take down the effective tariff rate to roughly 4-5%. That is still double the 2% rate pre-Trump.

The current projected rate is only slightly lower than the 12.5% we assumed in our recent Quarterly Economic Forecast. If those tariffs remain in place for six months, Canada’s economy slips into a shallow recession.

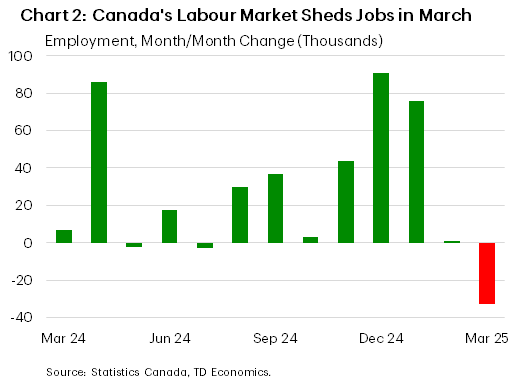

Canada’s job data for March reinforced a softer economic message. The labour market shed positions for the first time in more than three years (Chart 2), taking the unemployment rate higher by one tenth to 6.7%. There weren’t many silver linings in the report either. Job losses were in full-time positions in the private sector, and across most demographic groups. The share of people unemployed long-term also rose, and wage pressures eased. The job market may not be flashing red warning signs yet, but it is certainly yellow, and has softened significantly relative to the early post-pandemic period.

Looking at trends by sector, the losses in March were largest in the services sector, led by wholesale and retail trade (-29k; -1.0%), and information, culture and recreation (-20k; -2.4%). Although manufacturing (-7k; -0.4%) and construction (-4k; -0.2%) also saw job losses. Given the layoffs already announced in the auto sector this week, more are likely to come.

The Bank of Canada’s next interest rate announcement is on April 16th, and decision makers will still get to digest the BoC’s Business Outlook Survey and the March inflation report before then. Market odds of a rate cut increased sharply in the wake of the jobs data, to becoming the consensus view. We have argued that the Bank should cut rates further to support Canada’s economy in the face of the tariff threat, despite the risk of slightly higher inflation in the short run.

U.S. – A Return to Turbulent Times

We kicked off the second quarter this week with what has likely been the most anticipated day of the year so far. On it’s so-named ‘Day of Liberation’, the administration announced broad-based tariffs set to go into effect over the coming week. Equity markets and U.S. Treasury yields fell sharply over the following days on concerns over the economic impact of the policies. As of the time of writing, the S&P 500 is down 7.4% on the week, while the U.S. Treasury 10-year yield fell 33 basis-points (bps) to 3.93%.

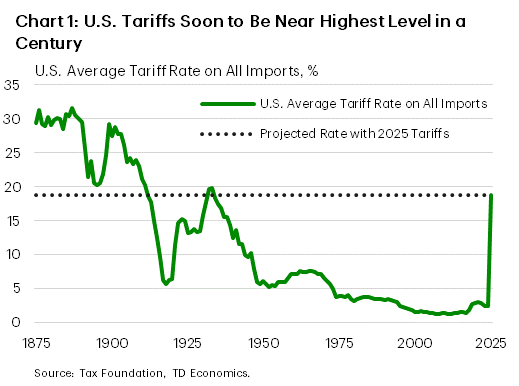

The tariffs announced by President Trump this week included a baseline 10% tariff on nearly every country that the U.S. trades with, scheduled to go into effect on April 5th, with varied upward revisions subsequently applied to 60 countries on April 9th. The latest tariffs will bring the effective tariff rate charged by the U.S. to its highest level in nearly a century (Chart 1). The countries likely to be the most impacted include China (which now faces a total stacked tariff rate of over 54%), the European Union (20%), and Vietnam (46%), although the effects, like the policy, are expected to be widespread. China has already announced that it will retaliate in equal force while the EU is preparing countermeasures. Some hope remains that negotiations can lead to the removal or some reduction of the tariffs before their full impact is felt, but for the time being it appears that we are witnessing the start of a trade war unlike any seen in generations.

Even before the most recent tariffs were announced, we were already starting to see some softening in the economic data. The ISM manufacturing and services purchasing manager indexes for March both showed a slowdown in demand and hiring activity, with business sentiment weakening on trade uncertainty. However, we have also seen consumers and businesses attempt to front-load purchases in advance of tariffs, with March vehicle sales hitting a four-year high and imports remaining more than 20% above year-ago levels through February.

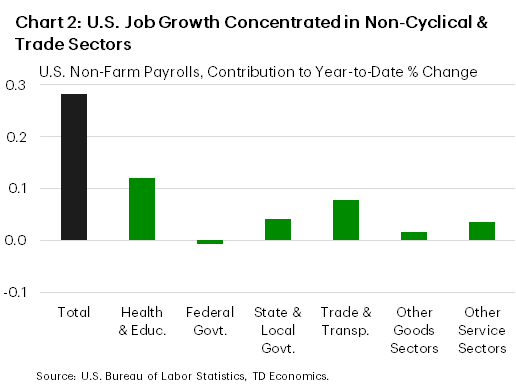

This behavior helped to keep the labor market healthy on aggregate in March, as 228k new jobs were added. Non-cyclical sectors, like health and education, as well as trade-exposed sectors contributed the lion’s share of the employment gains (Chart 2). While this was undoubtedly a solid report on the health of the labor market, we are likely to see some slowing in hiring over the coming months as trade policy uncertainty further weighs on business and consumer sentiment and tariffs begin to influence economic activity.

The next Federal Reserve meeting is still roughly a month away, but the views of Fed officials have likely become more consequential amid elevated uncertainty. During a presentation on Friday, Chair Powell noted that while the impact of tariffs remains uncertain, tariffs were likely to weigh on growth and raise inflation. As of the time of writing, markets are pricing in an 80% chance for 100bps in rate cuts by year-end. Next week’s CPI data release and the March FOMC meeting minutes will be parsed closely for further hints of the future direction of monetary policy as the administration’s ‘reciprocal’ tariffs are scheduled to come into effect. Assuming no changes occur between now and then, we will be entering a structurally different reality for global trade and finance.