{kind=link}

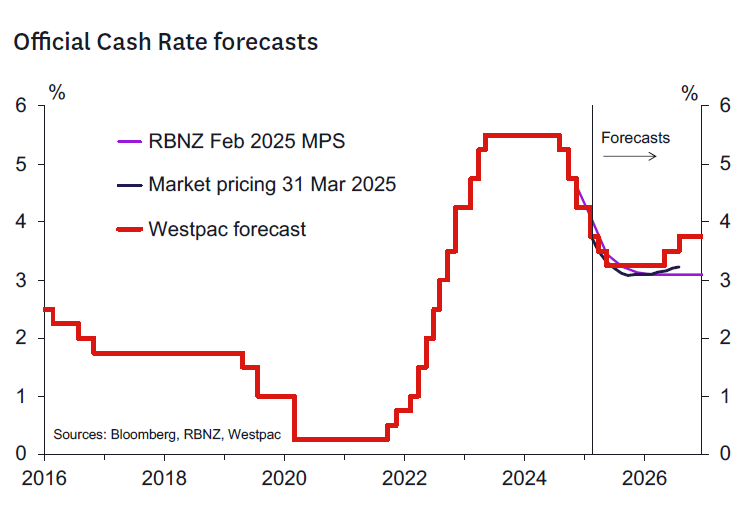

- We expect the OCR will be cut 25bp to 3.5%.

- The RBNZ will retain an easing bias.

- Global uncertainties and the perception the OCR is above the neutral rate will drive the easing bias.

- We are alert for signs of greater data dependency around future moves compared to the forward guidance in recent meetings.

- “No change” in the OCR will return to the set of plausible options for future meetings.

- The recent stronger data flow will be acknowledged and may be used to justify less confidence around cuts after the May Monetary Policy Statement.

- This OCR cut is likely the wrong thing to do. A more mandate consistent approach would be to leave the OCR unchanged at this meeting and consider a 25 bp cut at the May Monetary Policy Statement.

RBNZ decision and communication.

We expect the RBNZ to act on past signalling and cut the OCR by 25bp to 3.5% and signal a more data dependent easing bias looking ahead.

The RBNZ will likely note the economy was stronger than expected in late 2024 and that the recent data flow suggest growth has continued. This assessment will give the impression that another cut at the May Monetary Policy Statement is more likely than not but that cuts after May are more speculative than indicated at the February Monetary Policy Statement. The RBNZ is likely to note the inflation outlook remains at least as firm as previously expected and that developments on that front will be an important driver of the need for further OCR cuts in 2025.

We expect commentary on the weakening in the outlook in some trading partner economies, but also uncertainty on how the global activity will evolve. This is the stance other central banks have taken to date and should be a blueprint for the Monetary Policy Committee’s stance on this score.

We think the MPC’s objective will be to leave the option of pausing the easing cycle on the table at each meeting from here. We expect this will be in line with our forecast that the end of the cycle will come with the May Monetary Policy Statement and an OCR of 3.25%.

One thing to note is the key Q1 QSBO is released immediately ahead of the MPR. This data will be available to the Monetary Policy Committee in its deliberations. Should this survey indicate sharply reduced excess capacity and robust pricing pressures as evident in the monthly ANZBO survey then it’s possible our view of the MPR outcome will be revised.

Recent data flow and impact.

The key data since the February MPS release is as follows:

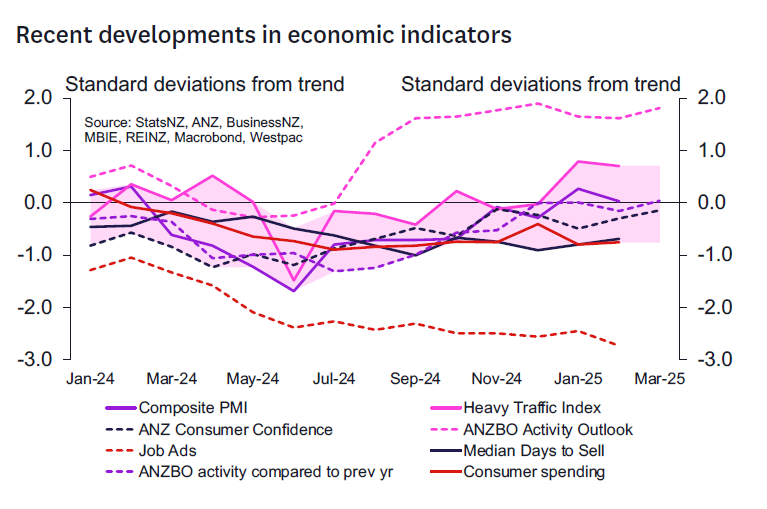

GDP: Activity grew 0.7%q/q in Q4, above the RBNZ’s February MPS estimate of 0.3%q/q. Private consumption spending was weaker than the RBNZ had estimated, but business capex and exports were stronger than expected (the latter probably reflecting the strength seen in services exports). Given the usual approach, the RBNZ will likely now assess that the negative output gap is narrower than the 1.7% of GDP that had been estimated for Q4. This data also provides confidence that the base level of growth in the economy in late 2024 was at least as strong as previously projected, which should increase confidence in the Bank’s growth forecasts in coming quarters.

Inflation: Based on selected prices data for the first two months of the quarter, we estimate that the CPI will increase 0.8%q/q in Q1 (data to be released on 17 April). Our estimate is in line with the RBNZ’s MPS forecast. The pricing intentions gauge in the ANZ’s business survey has increased in recent months and continues to sit at levels that historically have not been consistent with inflation remaining inside the target range. Given that the survey points to an expectation of subdued wage growth, these readings could reflect the factors such as rising global food prices and a weaker NZ dollar. Firms may also be optimistic that they can rebuild margins once the economy strengthens.

Employment: Based on filled jobs data for the first two months of the quarter, we estimate that household employment will likely print broadly flat in Q1, in line with the RBNZ’s February MPS forecast. Given growth in the working age population, we currently expect that the unemployment rate will rise to 5.3%, just above the RBNZ’s forecast of 5.2%. At this stage job advertising levels are yet to show a discernible lift from the cyclical lows reached last year.

Confidence: Consumer confidence (both Westpac and ANZ measures) has slipped a little in the last month or so but remains on an improving trend. The recent tick lower in confidence may reflect uncertainty associated with the global outlook as well as lingering concerns about job security. Ahead of the release of the QSBO on 8 April, business confidence – as measured in the ANZ’s Business Survey – has remained at an historically high level, with firms also very upbeat about the year-ahead outlook for their own activity.

Other activity indicators: The BusinessNZ manufacturing PMI posted a welcome lift to 53.9 in February – the first reading above 50 for two years. However, the services PMI fell back to 49.1 in February after rising above 50 in January for the first time in 12 months. Overall, most activity indicators confirm an improving underlying trend in activity – albeit with considerable month to month volatility as is inherent in these indicators.

Housing market: Both house sales and mortgage approvals point to increasing levels of housing activity since the second half of last year, trending higher as mortgage rates have been progressively lowered. House prices are on an improving trend but not booming as there remains a considerable stock of inventory on the market for demand to work through. At this stage the RBNZ will probably regard housing developments as tracking close to what was envisaged in the February MPS.

Kelly’s take – this cut is the wrong approach.

The main case for cutting at this meeting is the RBNZ essentially promised it at the February Monetary Policy Statement. However, I believe moving more slowly is more likely to be appropriate notwithstanding those past communications.

An evaluation of the data flow in recent months shows both an improving economy and robust inflation. Given the mandate is solely focused on inflation it’s hard to make the case for cutting rates at every meeting from here. A cut at the May Monetary Policy Statement is likely still to be justified. But its less clear further cuts would be required from there. Hence, we have reached the point where there is a difference between what I think the RBNZ will do as opposed to what they should do.

The RBNZ has put considerable weight on a view that the neutral OCR is around 3%. But this variable is unknown and unmeasurable in real time. Interest rates may also already be at neutral. Mortgage rates are likely at stimulatory levels now given rates between 1-3 years are around 5%. Stopping the easing cycle at either 3.5 or 3.25% may prove appropriate and would still deliver monetary conditions close to where they are today.

The exchange rate is also likely at stimulatory levels – evidence for that is clear in indicators of regional consumer demand and house prices.

The neutral OCR is an unhelpful concept for policy formulation now the OCR is no longer at obviously tight levels.

Another case for easing is concern on downside risks from the external outlook. Here I disagree that a proactive approach is appropriate. The starting point for the external sector is one of rude good health. If a negative shock is coming, the external sector is as well placed to deal with it as it could be. We have no idea if the global trade and tariff situation will meaningfully undermine the NZ economy. Any response to a negative external shock should be considered once the shock occurs and not before.

The exchange rate is playing the appropriate role as shock absorber. This should continue – cutting interest rates to somehow support asset prices to offset a permanent competitiveness loss from tariffs is unwise and inappropriate. How does pushing up NZ house prices to gee up domestic demand for a little while make NZ Inc better off right now? Especially when forecasts of inflation remain in the top half of the target range.

Conditions in the economy could deteriorate to the extent that inflation falls to the bottom half of the target range. That would justify an easing bias to be acted on when the data shows this to be happening. Guessing it might happen when inflation is heading towards 3% is not consistent with the MPC’s mandate.

The RBNZ has already cut rates aggressively – pretty much as quickly as seen in the Global Financial Crisis. We don’t have a crisis right now. Given the significant easing that’s already occurred, the stronger case is to step back and assess the impact of what’s already been done. No change in the OCR is appropriate.

While past communication appeared to promise a cut next week almost unconditionally, decisions should always be based on the situation on the ground. No change with an easing bias would be the right thing to do.