{kind=link}

Business confidence remains high, but cost pressures are becoming more of a feature.

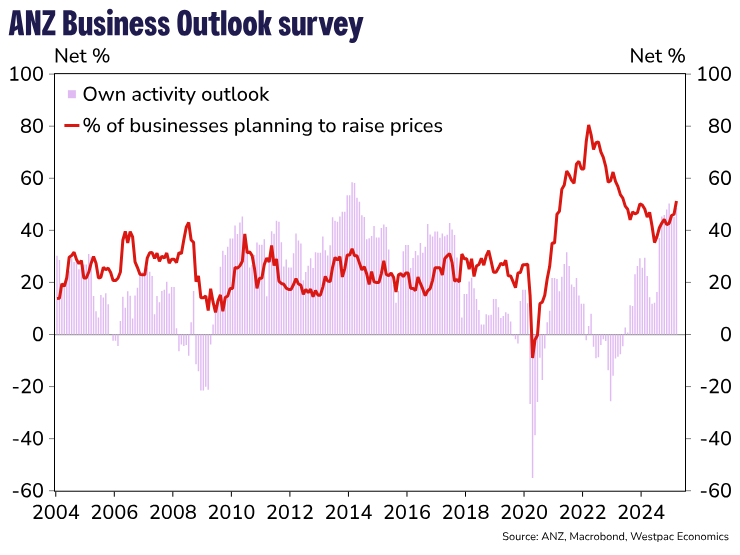

Key results, March 2025

- Business confidence: 57.5 (Prev: 58.4)

- Expectations for own trading activity: 48.6 (Prev: 45.1)

- Activity vs same month one year ago: 0.8 (Prev: -2.9)

- Inflation expectations: 2.63% (Prev: 2.53%)

- Pricing intentions: 51.3 (Prev: 46.2)

Business sentiment has remained upbeat in the early part of this year. The March ANZ business outlook survey saw marginal movements in the two headline measures – general confidence down slightly, firms’ own-activity expectations up – but with both remaining close to ten-year highs. Compared to a year earlier, a net 1% of firms reported that they were ahead, compared to a net 3% in February who felt they had gone backwards.

Notably, the inflation gauges of the survey are showing some signs of stirring. Firms’ reported costs have remained elevated since Covid, and they rose again in the March survey. Concerns about the impact of the weaker New Zealand dollar on the cost of imported inputs may be a factor here. Perhaps more importantly, firms believe that they will be able to pass on these cost increases: pricing intentions have been drifting higher for several months, and they took a notable step higher in March.

Overall, the survey results are well aligned with our recently-refreshed economic forecasts for New Zealand. We expect the pickup in GDP since the last quarter of 2024 to continue, albeit not reaching above-trend growth rates until the second half of this year. Annual inflation is expected to pick up temporarily as a result of the weaker NZD, peaking at 2.6% at the end of this year, but otherwise remaining within the target range. In that light, the RBNZ is still likely to deliver the OCR cuts that it signalled for the April and May policy reviews, but beyond that point we don’t think there will be a compelling case for further cuts.