{kind=link}

Canadian Highlights

- The announcement of U.S. tariffs on the auto sector this week could be a major downside risk for the Canadian economy. Attention now turns to the April 2nd “reciprocal tariff” announcement and Canada’s response.

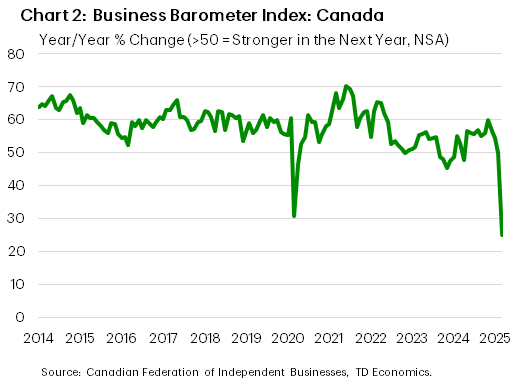

- Not surprisingly, a major survey of businesses showed that business confidence took a tumble in March.

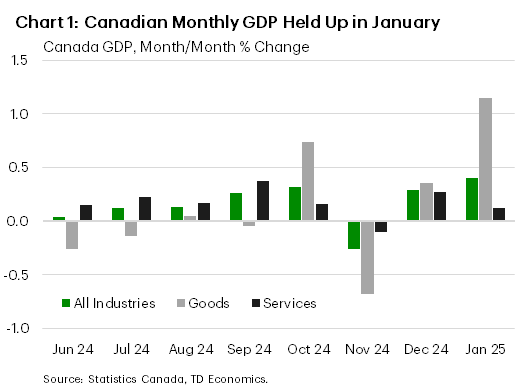

- Before trade tensions emerged as the most important issue for the Canadian economy, the latest data show the economy had held up in January, although the service sector did show some weakness.

U.S. Highlights

- This week’s announcement of new automobile tariffs caught markets by surprise. But now all eyes are focused on updates on reciprocal tariffs next week.

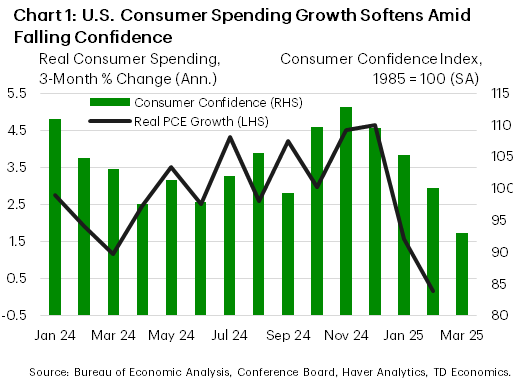

- The U.S. economy had been humming, but as uncertainty ramps up and consumer confidence continues to dip, the risks of a slowdown are building.

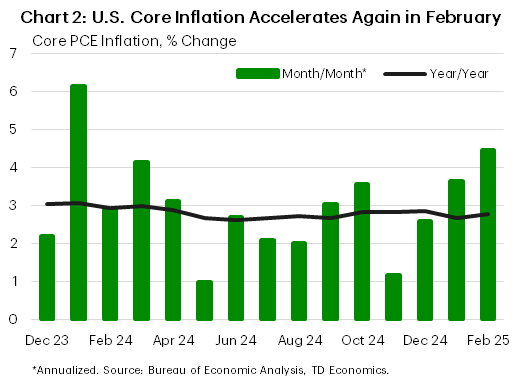

- Worryingly, inflation momentum picked up again in February suggesting price growth could be stickier than anticipated.

Canada – Bracing for Impact

Going into this week, April 2nd, the day that the United States is expected to announce reciprocal tariffs on all its trading partners, already loomed large over the Canadian economy. Many questions remained, such as the coverage of countries and goods, and the size of the tariff. Then the Trump administration surprised markets this week with an announcement of a 25% tariffs on the auto sector, scheduled to take effect on April 3rd. We covered what we know about these tariffs in our report yesterday but many questions remain, including exactly how high the tariff will be for Canada. As of now, there are some indications that Canada and Mexico may receive a lower tariff on autos than other countries. We expect that the full picture of U.S. tariff measures will remain somewhat in flux at least until April 2nd, and the same is likely true for any response from the Canadian government.

But the world still turns, and the data still come in. We released our commentary on today’s Canadian GDP by industry earlier this morning, which showed that Canada’s economy surged in January, on top of a healthy pace in December. The major driver of January’s pickup was mining and oil and gas extraction, which accounted for nearly a third of all growth in January. Manufacturing and construction also did well, while the major laggard was retail. These data show the state of the economy through January 2025, much of it from before the world realized tariff uncertainty would be omnipresent for the next two months. These data suggest that the goods-producing sector in Canada was on solid footing in January, as we can see in Chart 1. But much of that likely represented firms’ attempt to get ahead of impending tariffs. The next release may tell a different story, as the advance estimate for February is already pointing to no growth in monthly GDP.

We don’t have to wait to see some indication that tariffs are taking a toll already. After all, last week we saw soft retail sales and housing sales in February, the first major hard data prints for the month. This week, the CFIB Business Barometer for March was released, and it showed that business confidence in Canada has taken a major hit, falling to the lowest in ten years and lower than at any point during the COVID-19 pandemic. It seems businesses are bracing for a difficult year ahead.

The new Quebec budget released earlier this week underscored that these concerns are top of mind across Canada. It included measures to give relief to consumers and businesses hurt by tariffs, and to support infrastructure investment, as we discussed in our report earlier this week. The Bank of Canada also released their summary of deliberations from their las interest rate cut decision. These emphasized how much tariff threats are weighing on their outlook. The BoC likely would not have cut interest rates in March were it not for tariff threats and elevated uncertainty. Next week, we’ll see how the Canadian labour market has held up through March, and we’ll receive international trade data, which may also contain some clues about how businesses have been managing the shifting trade environment. But all eyes and ears are going to be on the April 2nd tariff announcement and Canada’s response.

U.S. – Waiting for April 2nd

After steadily rallying since mid-March, markets took a step back this week when new U.S. tariffs on automobiles and parts were announced. The news comes ahead of next week’s much anticipated update on reciprocal tariffs that are expected to cover major U.S. trading partners. In the meantime, February’s Personal Income and Outlays report showed that core inflation picked up again, while spending growth failed to recover from last month’s decline. The U.S. economy had been humming, but as uncertainty ramps up and consumer confidence continues to dip, the risks of a slowdown are building. All eyes are now firmly focused on next week’s tariff announcement for more clarity on the operating environment going forward.

The big news this week was President Trump’s announcement of new tariffs on automobile imports of 25%, set to take effect on April 3rd. This comes ahead of the expected announcement next week on reciprocal tariffs that markets had been bracing for. At the time of writing, most countries had held off on any new retaliation, likely opting to wait and see what’s in store from next week’s announcements before proceeding. As we wrote, the full impact of the autos tariffs will depend on their duration and how much of the cost firms pass along to their customers.

Yet, while we await more clarity on the import taxes, consumer confidence continues to dip, and the darkening moods appear to be flowing through to behavior. The Conference Board measure of consumer confidence has fallen to its lowest level since early-2021. With sinking sentiment, an adjustment in consumer spending appears to be unfolding as real outlays in February failed to recover from the tumble they took in January (Chart 1). This leaves the three-month annualized change in real consumer spending at 0.2%, well short of the 4.6% clip recorded in December. First quarter consumer spending is now tracking only a 0.5% annualized pace, a downgrade from our recent forecast. Importantly, the pullback in real spending is coming at a time of still-healthy income growth, so with the savings rate ticking up to 4.6% (its highest level since June of last year), this suggests that some precautionary savings could be taking place.

Part of the story is that inflation looks to be heating up again. Higher price growth is cutting into consumers’ purchasing power, restraining real outlays. The core personal consumption expenditures price index saw its biggest monthly gain since January of last year, taking the annual pace to 2.8% (Chart 2). Inflation momentum appears to be gaining steam, and consumer are noticing. Inflation expectations for the year ahead jumped to their highest levels since late-2022.

For the Fed, the combination of softening growth and rising inflation are troublesome. Yet, what could make it more complicated is if inflation expectations continue to rise, creating a self-reinforcing loop of greater price pressures. For now, though, we wait for next week for more clarity on the next set of tariffs to better guide our assumptions around the forecast.