{kind=link}

Summary

- The Eurozone economy showed a degree of resilience late last year, though some notable policy developments in early 2025 have since had some significant implications for the region’s medium-term outlook. The likelihood of higher tariffs of imports from the European Union should restrain Eurozone growth in 2025, and our GDP growth forecast is unchanged at 0.8%. However, landmark fiscal stimulus from Germany has in our view brightened prospects for both Germany and the broader Eurozone, prompting us to raise our 2026 Eurozone GDP growth forecast to 1.6%.

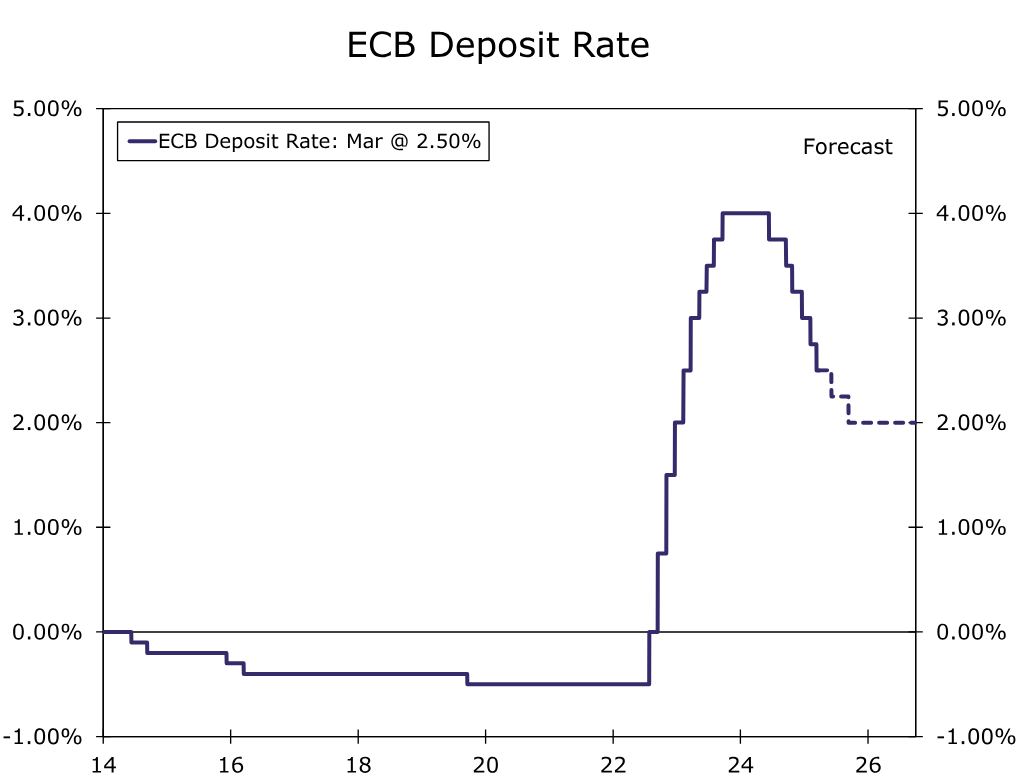

- A brighter and more balanced medium-term outlook for the Eurozone means we also now expect a less dovish monetary policy approach from the European Central Bank (ECB). With downside growth risks lessening, and inflation pressures still easing relatively gradually, we expect even more careful and considered deliberations by ECB policymakers at upcoming meetings. We now forecast 25 bps ECB rates cuts in June and September (that is, every other meeting). That would see the ECB’s policy rate reach a low of 2.00% by September, compared to our previous outlook for a policy rate low of 1.75%.

- A firmer medium-term growth outlook and less dovish European Central Bank also has implications for the outlook for the European currency, especially when juxtaposed against our evolving U.S. outlook which sees softer GDP growth in 2025, and slightly faster Fed easing this year. We now expect only a gradual pace of euro depreciation over time, targeting a EUR/USD exchange rate of $1.02 by Q3-2026.

Eurozone’s Economic Landscape Evolving, Medium-Term Prospects Brightening

The Eurozone economy showed a degree of resilience late last year, offering some encouragement that the region’s recovery could gather further momentum in 2025. In the early part of this year, however, there have been some notable policy developments, with significant implications for the Eurozone outlook. The increasing threat of tariffs from the United States could weigh on growth this year, but the prospect of more expansive fiscal policy in Germany has, in our view, improved the region’s medium-term growth outlook. Our forecast for Eurozone GDP growth for 2025 is unchanged at 0.8%, while we have revised our forecast for Eurozone 2026 GDP growth higher to 1.6%.

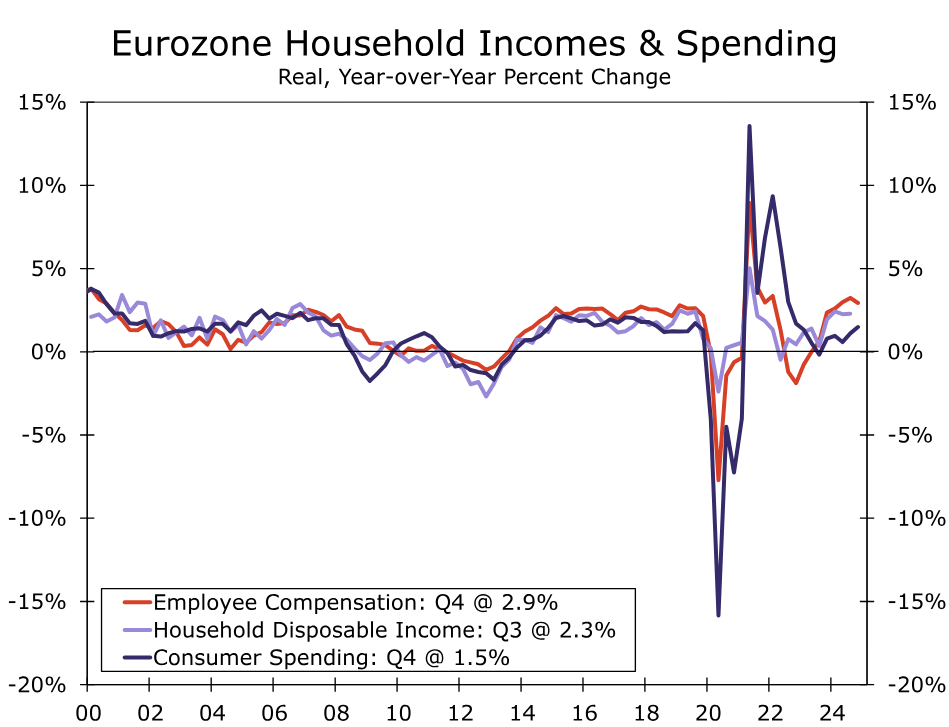

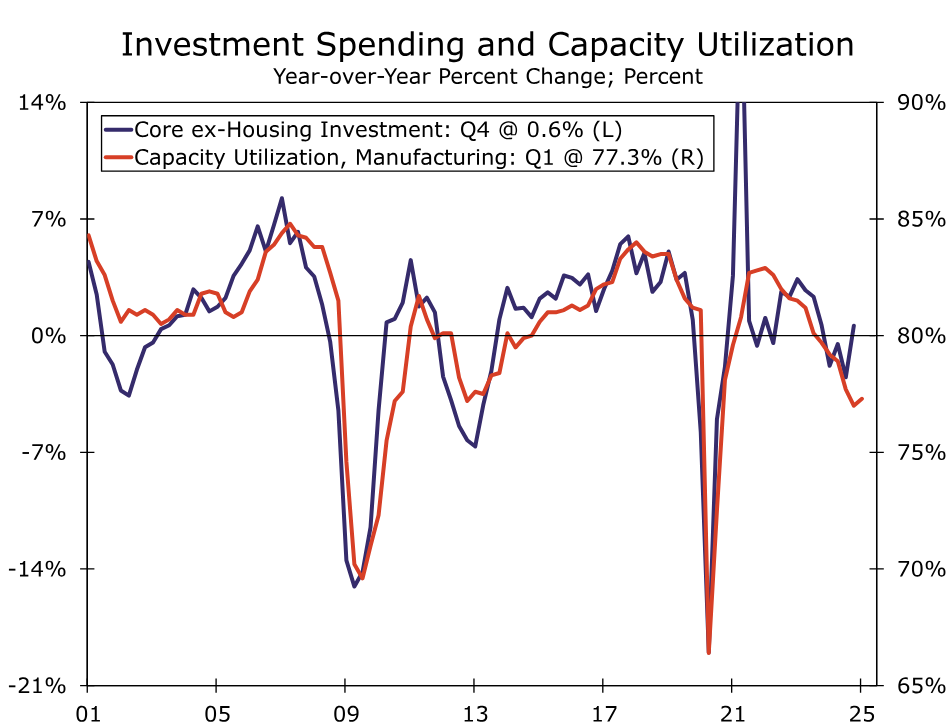

Eurozone GDP rose a moderate 0.2% quarter-over-quarter in Q4-2024 though, with upward revisions to prior quarters, that helped boost growth to 1.4% year-over-year. For the fourth quarter specifically, the expansion in economic activity was quite broad-based, as household consumption rose 0.4% quarter-over-quarter, government consumption also rose 0.4%, and investment spending rose 0.6%. The increase in investment spending was also notable in that it included an increase in core ex-housing investment (that is, excluding the volatile intellectual property products component). For now, growth in employee compensation and household disposable income continues to run ahead of consumer spending, suggesting there remains room for a further modest consumer recovery over the course of this year. The near-term outlook for investment spending is more mixed, however, given softening corporate profits and still-low levels of manufacturing capacity utilization.

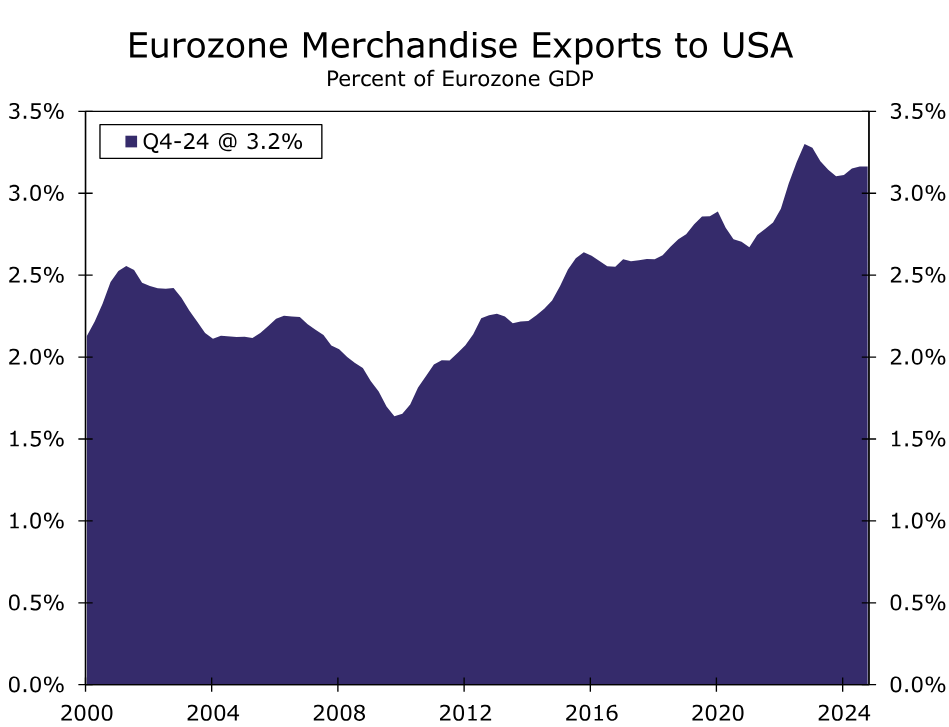

Indeed, the uncertain near-term outlook for investment spending and broader economic activity has been compounded by the growing threat of higher tariffs from the United States. President Trump has often highlighted the large trade imbalance with Europe, as well as some internal taxes within Europe. The latest available figures highlight that trade imbalance, with the Eurozone running a €183 billion merchandise trade surplus with the United States in the 12 months through January. Considering this backdrop, we anticipate the European Union will indeed face higher tariffs from the United States. From Q2-2025 and through the end of our forecast horizon (Q4-2026), we assume a 10% effective tariff rate on goods imported from the European Union, with a similar level of retaliation from Europe on the United States.

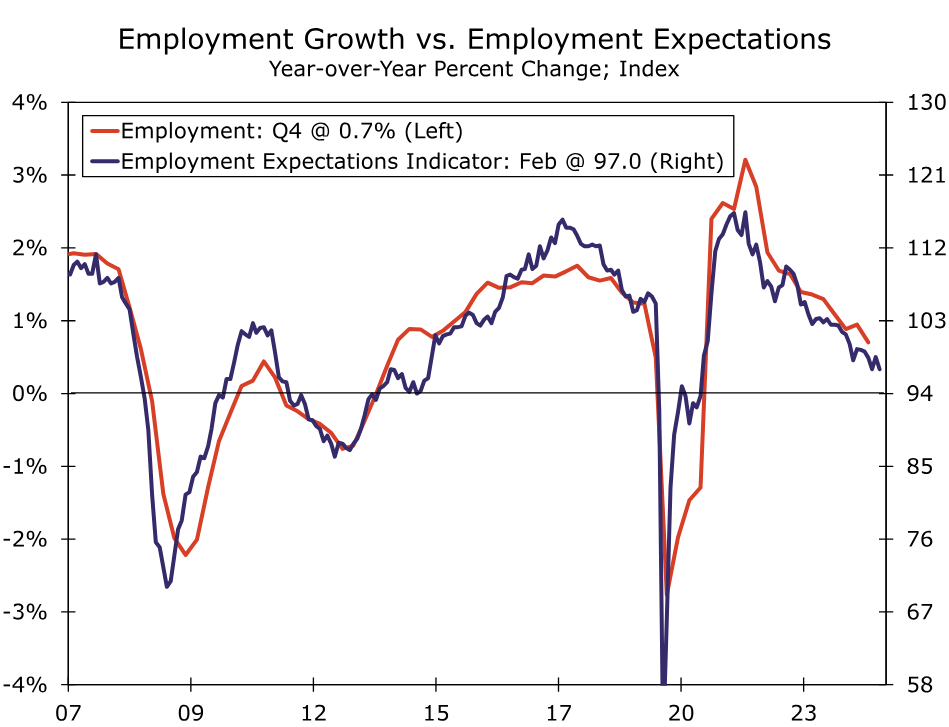

The direct impact of higher tariffs on the Eurozone will, we think, be moderate, with merchandise exports to the United States accounting for a little more than 3% of the region’s GDP in 2024. That said, given the increased uncertainty stemming from increased trade and tariff tensions, the indirect effects on activity could be more pronounced. Indeed, there are signs that a more uncertain environment is already weighing on employment and spending decisions. For example, the European Commission Employment Expectations Indicator fell further to 97.0 in March, extending what had been an overall declining trend since early 2022. The further drop in the indicator suggests that employment growth, which was already just a tepid 0.7% year-over-year in Q4, could slow even further this year.

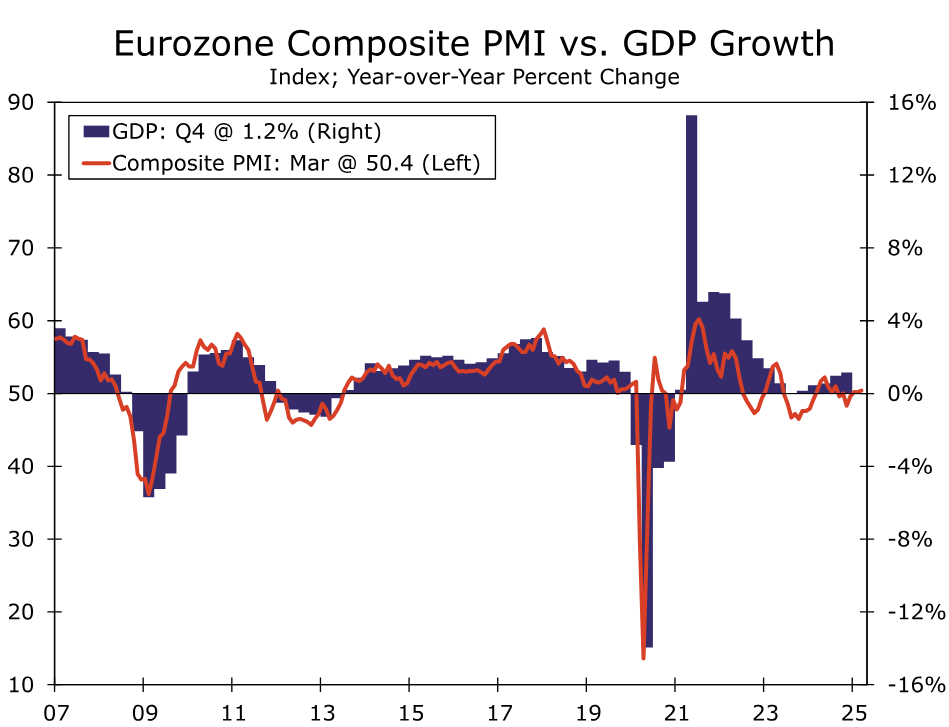

Meanwhile, sentiment surveys are, for now, consistent with only a modest pace of growth. In March, the manufacturing PMI rose to 48.7. While the improvement perhaps reflects increased hopes for spending on infrastructure and defense, a topic we will return to later, the index is nonetheless still at levels historically consistent with a contracting industrial sector. The Eurozone services PMI slipped to 50.4 in March, a third straight decline and suggests the economically significant services sector is struggling to gather any momentum during the early part of 2025. Overall, the composite or economy-wide PMI edged up to 50.4, a level also historically consistent with only modestly positive GDP growth. With some hints of slower employment and investment in early 2025, and considering the downside impact from higher tariffs, we do not envisage a Eurozone growth upswing this year. We forecast Eurozone GDP growth of 0.8% in 2025, broadly similar to the pace of expansion seen last year.

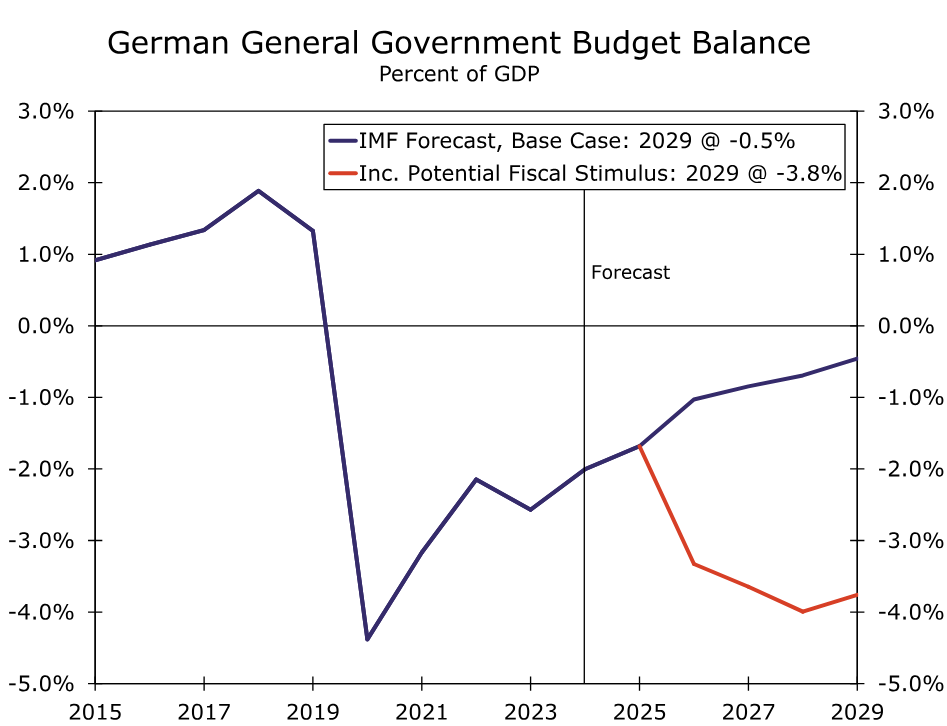

We do, however, believe Eurozone growth prospects for 2026 have improved considerably, primarily reflecting political developments in Germany and a landmark shift in German fiscal policy. Germany has traditionally been the Eurozone’s most fiscally cautious economy and, since 2009, has incorporated the “debt brake” as part of the country’s constitution. In recent years, debt brake laws have required the federal government to limit its structural budget deficit to no more than 0.35% of GDP and required German states to run balanced budgets except for times of national emergency or recession. However, following the late February election that has changed dramatically. After two years of economic contraction and as geopolitical developments have heightened European security concerns, Germany’s Chancellor-in-waiting Friedrich Merz has engineered a remarkable fiscal stimulus despite coalition negotiations that are still in progress. The key elements of Germany’s new fiscal measures include:

- Excluding defense spending in excess of 1% of GDP from the constitutional debt restriction. Germany reported to NATO that it spent around €90 billion on defense in 2024, through a combination of its regular budget, the use of special off-budget funds and some additional expenses.

- Allowing Germany’s 16 states to borrow as much of 0.35% of their GDP as opposed to being required to run balanced budgets

- Establishing a special off-budget infrastructure fund that will be empowered to borrow as much as €500 billion over 12 years, or just under €42 billion per year. Of that amount, €100 billion will be transferred to the Climate and Transition Fund, while states will receive €100 billion for regional projects.

Altogether, the measures could be a momentous change for the German economy, and ultimately (though to a lesser extent) the broader Eurozone economy. To the extent an exemption of defense spending from the debt brake frees up room for spending that previously counted against the deficit limits, it could create potential space for ~1% of GDP for spending in other areas going forward. Should the federal government and states be able to fully utilize the leeway from the constitutional changes, that would equate to fiscal stimulus of 1.35% of GDP, while the infrastructure fund would equate to another 1% of GDP. While increased spending might not ramp up immediately, that suggests potential German fiscal stimulus of around 2.3% of GDP over the next several quarters, a development that should be beneficial for the 2026 growth outlook in particular. Should German defense spending indeed rise, German overall fiscal stimulus could amount to more than 3% of GDP over the next several years. That overall magnitude of German fiscal stimulus is also equates to Eurozone fiscal stimulus of 0.7%-0.9% of Eurozone GDP over the next several quarters to years. Even with higher tariffs, we view more expansive fiscal policy as a net positive for the region’s economy, and have lifted our forecast Eurozone GDP growth forecast for 2026 to 1.6%. We also expect fiscal stimulus to kickstart Germany’s economy, which has been a significant underperformer within the Eurozone in recent years.

European Central Bank to Shift to a More Gradual Easing Pace

The brighter medium-term outlook for the Eurozone is in our view likely to alter the destination, as well as the path, for the European Central Bank’s monetary policy interest rate. For the past several meetings, up to and including its early March announcement, the ECB has been lowering its Deposit Rate at a steady 25-bps-per-meeting cadence. Although core inflation, and more particularly services inflation, have been decelerating at a rather gradual pace, the significant downside risks to the Eurozone economic outlook have given ECB policymakers the motivation, and the comfort, to reduce interest rates at a steady clip. With the Eurozone growth outlook now firmer and more balanced, that could argue for even more careful and considered deliberation by ECB policymakers at upcoming meetings.

One might in fact suggest that ECB policymakers took a small step toward this more cautious approach at their March announcement. In its introductory statement, the ECB, in a change of language, said “monetary policy is becoming meaningfully less restrictive,” while repeating that it will follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance. The ECB also repeated that it is not pre-committing to a particular rate path.

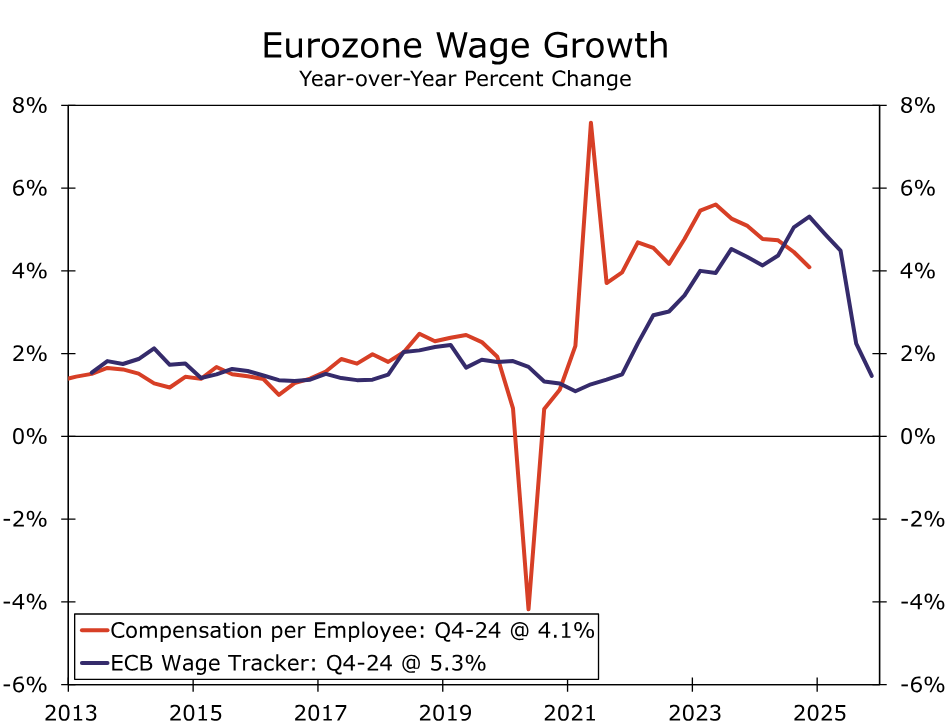

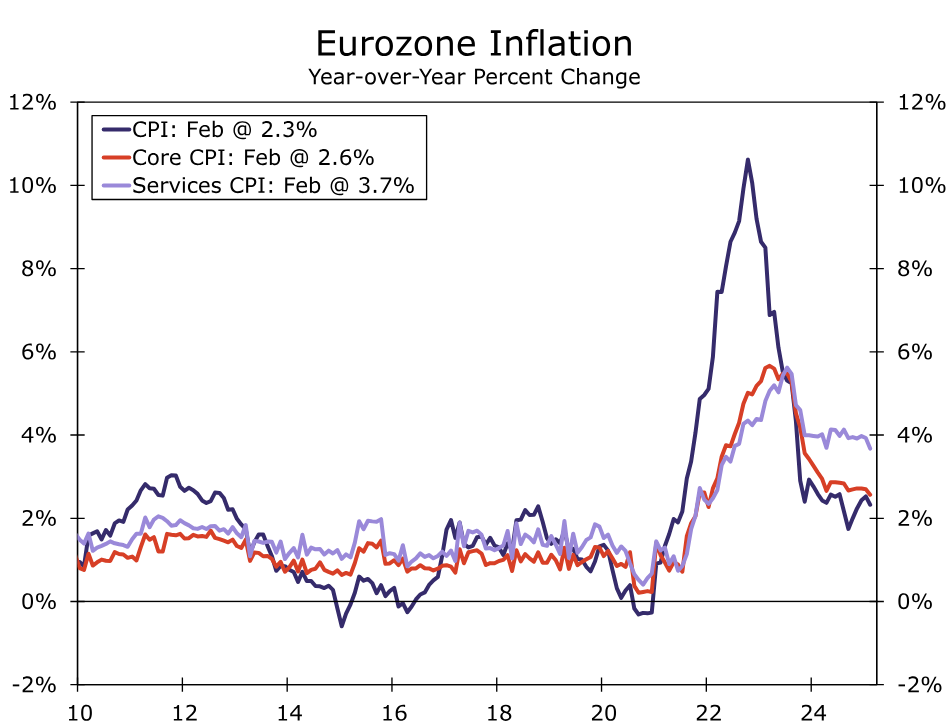

While most wage and inflation indicators are moving in a favorable direction, they remain at levels that are likely not consistent—not just yet, at least—with CPI inflation converging sustainably toward the central bank’s 2% inflation target. Q4 compensation per employee slowed to 4.1% year-over-year, with productivity on a per-person basis up just 0.4% over the same period, unit labor costs also rose 3.7%. We would view wage growth of closer to 3%, and unit labor cost growth of closer to 2%, as more consistent with inflation converging sustainably towards target. That is particularly the case given the possibility of a modest uptick in goods inflation amid a global backdrop of higher tariffs. The ECB’s Wage Tracker offers some encouragement that wage growth will indeed slow further, but amid a more balanced growth backdrop, policymakers may wish to see confirmation of that deceleration before proceeding with further easing. From a price perspective, the latest CPI reading for February saw core inflation at 2.6% year-over-year and services inflation at 3.7%. The latter would require a persistently low level of goods inflation to sustainably achieve the 2% target, a low level of goods inflation that might be more difficult to achieve given the current tariff dynamics.

Finally, the ECB earlier this year published research suggesting the neutral policy rate for the Eurozone lies in a region of 1.75% to 2.25%, though of course that estimated range is subject to inherent uncertainty. Still, given a more balanced outlook, we see less need for the ECB to “undershoot” its neutral policy rate, but rather simply return its policy interest rate towards a neutral range. In addition, a more balanced outlook perhaps argues for less urgency in adjusting the central bank’s monetary policy setting. To be sure, an April rate cut is still possible, and may depend on whether there is a further significant deceleration is services inflation in March. Our base case, however, is for more gradual and less pronounced ECB monetary easing than we had previously envisaged. We expect the ECB to pause in April, cut rates 25 bps in June, pause in July, and cuts rates 25 bps in September, for the ECB’s policy rate to reach a low of 2.00% by later this year. A firmer medium-term growth outlook and less dovish European Central Bank also has implications for the outlook for the European currency, especially when juxtaposed against our evolving U.S. outlook which sees softer GDP growth in 2025, and slightly faster Fed easing this year. In terms of our medium-term forecast we see a much more gradual pace of euro depreciation over the next several quarters than previously, and target a EUR/USD exchange rate of $1.02 by Q3-2026.