{kind=link}

The United States’ administration’s announcement on reciprocal tariffs on Wednesday threatens to overshadow normally key job market reports for February in Canada and the U.S. on Friday.

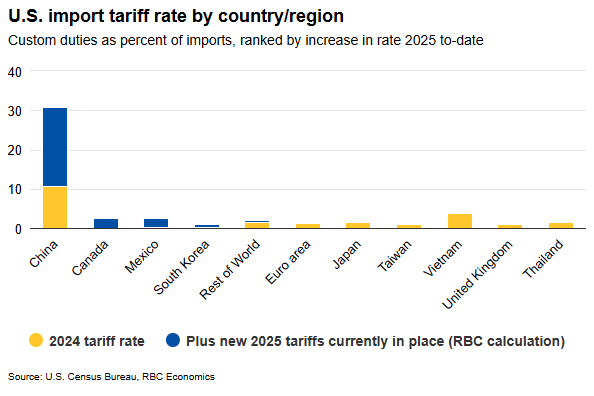

The start and stop of trade threats and actions from the U.S. have been dizzying, but as much as the uncertainty has intensified, U.S. tariffs implemented so far have not been large enough to cause a recession in Canada. By our count, the effective average U.S. tariff on imports from Canada has increased to about 2.5% from essentially zero in January.

The vast majority of U.S. imports from Canada that are USMCA/CUSMA compliant were quickly exempted from the more severe blanket 25% tariff imposed in early March. The additional steel and aluminium tariffs implemented on March 12 are large, but products impacted account for a relatively small share (about 4%) of Canadian exports to the U.S.

U.S. tariffs on finished motor vehicle exports announced this week are scheduled to kick in on April 3, and would add roughly another percentage point to that Canadian rate by our count. Still, most motor vehicle parts are (critically) not included in the initial auto tariff announcement and the value of U.S. intermediate products embodied in those finished vehicles, accounting for roughly half of the total value in Canada’s case, are set to be excluded.

Canada has seen the second largest increase in the effective tariff rate applied by the U.S. to-date, but most (about 80%) of the doubling in the total U.S. tariff rate on all countries has still come from the additional 20% blanket tariffs imposed on China.

Activity hasn’t softened as much as sentiment suggests but unemployment ticked higher

Measures of business and consumer confidence have already pulled back significantly in Canada. Consumer confidence hit all-time lows in March. But, early reports on actual spending and hiring decisions have held up better than softening sentiment alone suggests.

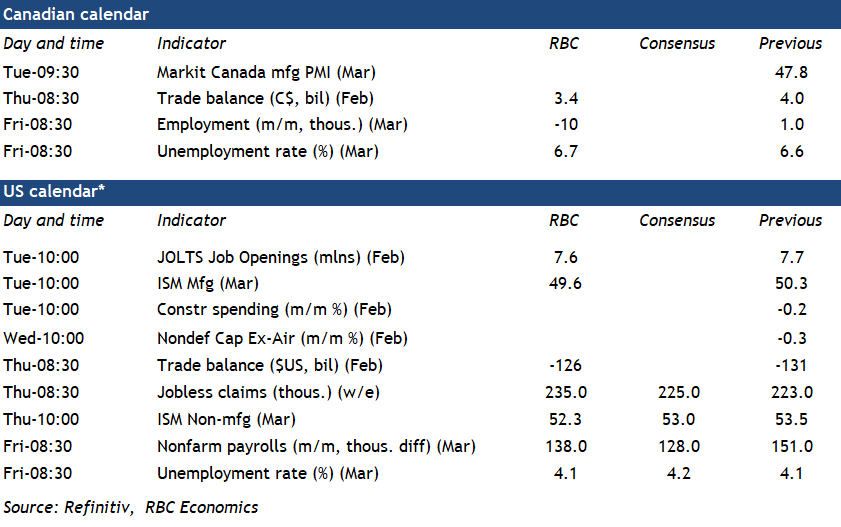

Our tracking of consumer purchases showed a mild pullback in retail spending in February, coinciding with the end of the federal tax holiday and a severe snowstorm in parts of Ontario. Hiring demand has showed some signs of slowing, but remains relatively resilient. Job openings posted on indeed.com have declined, but remain 11% above lows in October last year. We expect February’s pause in Canadian employment growth extended to a 10,000 decline in March and the unemployment rate rose to 6.7% from February’s 6.6%, but it still remains below November’s 6.9% peak.

Watch out for Canada’s rank as well as rate in reciprocal tariffs

Backward looking economic data in Canada still looks relatively resilient, but international trade risks are clouding the outlook. We know the U.S. reciprocal tariffs announcement is meant to represent a catch-all trade response to tariffs charged by trading partners, as well as a broad range of other policies the U.S. administration views as unfairly disadvantaging them (e.g., perceived currency manipulation, digital services taxes, value added taxes like Canada’s GST—see the Issue in focus here for more).

What exactly those measures look like remains highly uncertain, but targeting a broader swath of U.S. trade partners would mark a shift from measures announced so far that have been focused on the U.S.’s largest trade partners, namely China, Canada, and Mexico. We expect that where Canada ranks on the list of potential tariff increases next week compared to other regions will be as important as the rate itself. Canada was the U.S.’s second largest trade partner in 2024 in total export and import flows, but ranked as just the 9th largest source of the U.S. merchandise trade deficit (the deficit coming entirely from oil and gas products).

We have argued before that tariffs are unlikely to shrink the total U.S. trade deficit in the near-term (beyond potential distortions like the front-running of imports ahead of expected tariff hikes). But one of the major concerns from tariff measures to-date has been the narrow focus on a handful of countries including Canada, which provides a strong incentive for U.S. buyers to shift purchases away to other exporters. There are no absolute winners in a trade war, and the threat also remains that blanket tariffs briefly imposed on Canadian exports in early March could be re-imposed. But, a smaller tariff rate gap between Canada and other countries/regions could also arguably be a less damaging scenario for Canada than the current status quo.

Week ahead data watch

We expect Canadian employment edged down 10,000 in March after slowing to just 1,000 in February. It retraces only a fraction of the 76,000 jobs jump in January. Job openings from indeed.com into the second half of March are pointing to relatively resilient, but still softening hiring demand. Growth in the available labour supply will increasingly be restricted by slower population growth.

We expect the Canadian trade balance to come in at $3.4 billion in February, slightly down from the $4 billion in the prior month, but still elevated at least in part due to inventory building ahead of threatened U.S. import tariffs. We expect both exports and imports declined during that month given a 5% decline in oil prices lowering the energy trade balance. Rail carloading activities were also lower in February.

We expect U.S. payroll employment rose by 138,000 in March—roughly in line with the average increase over the prior two months. Hiring is expected to continue to slow in the public sector. We expect the unemployment rate to hold steady at 4.1%.

The advance estimate of the U.S. goods trade deficit edged lower, but remained wide after spiking higher in January. A 4% jump in exports was led by higher by auto products in the advance report, while imports remained high dipping just 0.2% after a 12.5% jump in January. Imports of industrial supplies edged down 5% after surging in the prior months on larger imports of non-monetary gold.