{kind=link}

Canadian Highlights

- Canadian economic data are giving a glimpse of what could be in store for the rest of 2025, with weak consumer activity and higher inflation at the forefront.

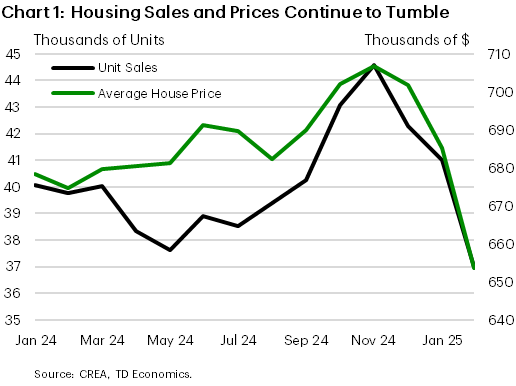

- Housing sales dropped by the largest amount since the Bank of Canada (BoC) started its aggressive rate hiking cycle in 2022. Retail sales also plunged as consumers pulled back on auto purchases.

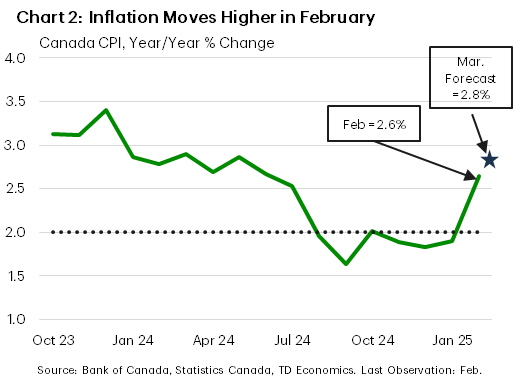

- Inflation reared its ugly head again, as the end of the GST/HST holiday lifted headline CPI above the BoC’s 2% target.

U.S. Highlights

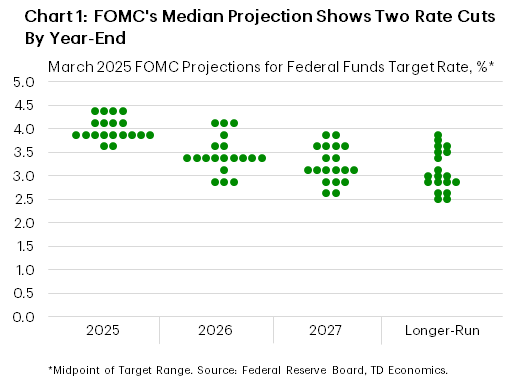

- The FOMC held the policy rate steady at a target range of 4.25%-4.5% for the second consecutive meeting. But, committed to slowing the pace of balance sheet runoff of its U.S. Treasury holdings.

- Revised economic projections showed a small downgrade to the FOMC’s growth outlook, but a near-term upgrade to inflation. The median forecast still expects 50bps of rate cuts by year-end.

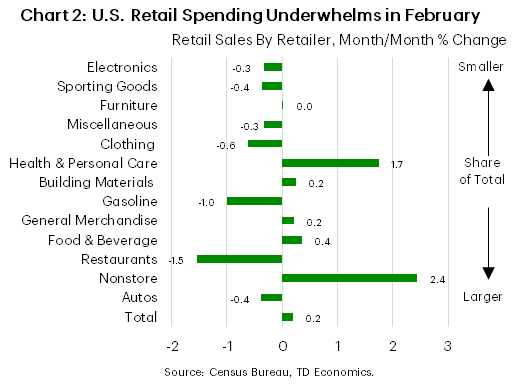

- February data out this week were mixed. Retail sales underwhelmed, while housing data rebounded from January’s weather induced slide.

Canada – Inflation Gets Hot While Real Estate Cools

Canadian economic data are giving a glimpse of what could be instore for the rest of 2025. The housing market has cooled dramatically as buyers moved to the sidelines amidst heightened uncertainty. Weak retail sales numbers have followed suit. At the same time, inflation surged higher, and it’s not just the end of the GST/HST holiday. Financial market volatility remains at the forefront, with equities struggling to bounce off the floor, and bond markets meekly pulling forward the re-start of Fed rate cuts.

This week’s real estate reports were the first hard data points (not sentiment) that reflect the impact of Trump tariffs on consumer behaviour. Existing home sales dropped a whopping 10% month-on-month (m/m) in February (Chart 1). That is the largest decline since the BoC started its rapid rate hiking cycle in the spring of 2022. There were winter storms that may have had an impact, but the decline was clear across the country (not just where storms hit). And this is with the Bank of Canada (BoC) continuing to cut its policy rate and employment/wage growth unabated. From our view, this reflects growing uncertainty amongst buyers, who logically may want to hold off on any big financial commitments. Builders got the signal and they too pulled back on housing starts for condos and single-family homes. Retail sales numbers for January also reflected hesitancy, falling 1.1% m/m in volume terms. It is still early days, but the impact of trade tariffs appears to be quickly permeating through consumer demand.

Trade tariffs will also have an impact on consumer prices. For much of the last few months, inflation was stable, even reaching below the BoC’s 2% target. Part of this was the government’s sales tax holiday, which artificially pulled down inflation. This holiday ended in mid-February and lifted February’s CPI inflation reading to 2.6% year-on-year, from 1.9% y/y in January (Chart 2). We think inflation will continue to rise in March, reflecting a full month of consumers paying taxes when they buy wine at the liquor store and eat at restaurants. Is higher inflation a sign of things to come for Canadians?

There will be a lot of moving parts in the inflation readings through spring. Tariffs are already in place for steel and aluminum, lifting the cost for intermediate goods on the margin over the coming months (beer cans for example). If more tariffs come into effect in early April alongside the increase of Canada’s retaliatory tariffs on $185 billion of U.S. goods, a host of consumer items will see significant price increases (cars/home appliances/etc). In the trade war of 2018, CPI rose by around half a percentage point (ppt) when Canada retaliated against U.S. tariffs on steel and aluminum. A bigger trade war this time around would have over a 1 ppt impact on Canadian CPI. Luckily, the cancellation of the consumer carbon tax will provide an offset. Gasoline prices should drop by about 20 cents on April 1st (not an April fool’s day joke). Other energy product prices will also come down, which would actually keep inflation stable in April even if Trump follows through on tariffs. But that would only be a reprieve should this full-blown trade war take hold. Please take a look at our Quarterly Economic Forecast published this week.

U.S. – Uncertainty Clouding the Outlook

With no new tariff announcements, trade tensions were temporarily moved to the backburner this week, allowing investors to shift the focus to the economic data calendar. February data readings out this week were mixed. Retail sales underwhelmed expectations, but both housing starts, and existing home sales largely recovered from January’s weather induced slide. Meanwhile, the Federal Reserve held the policy rate steady at a target range of 4.25%-4.5% but signaled an intention to slow the pace of balance sheet runoff for U.S. Treasury holdings starting in April. While investors were braced for a more downbeat messaging on the outlook, the Fed’s statement and Chair Powell’s press conference struck a more balanced tone. This helped to temporarily soothe unnerved financial markets, but growth fears reemerged by late-week, fueling a further sell-off. At time of writing, the S&P 500 was down 0.5%, while term yields traded lower by about 10bps, with the 10-year Treasury currently sitting at 4.22%.

The Fed’s statement included updated economic projections from FOMC members. The median GDP forecast was revised lower over the forecast, with a below-trend pace of economic growth expected in 2025 (1.7% from 2.1%), before steadying at 1.8% in 2026 (previously 2.0%) and 2027 (previously 1.9%). The unemployment rate was nudged higher by a tick this year to 4.4% but remained unchanged at 4.3% in 2026 and 2027. Core PCE inflation was also revised higher for 2025 (2.8% from 2.5%), which Chair Powell largely attributed to tariff impacts. Importantly, the revised “dot plot” still showed two 25bps rate cuts for this year. But a closer inspection of the dots shows that committee members see the balance of risks skewed towards fewer cuts, as eight officials now expect one or no cuts this year (up from four in December) (Chart 1).

During the press conference, Chair Powell characterized the economy as “strong”, but emphasized that any point forecasts remain “highly uncertain” in light of recent policy changes under the new administration. When asked about the recent pullback in business and consumer sentiment measures, Powell reiterated that the “hard data” are still showing an economy that is “solid”. He also downplayed the recent jump in inflation expectations shown in the University of Michigan survey, characterizing it as an outlier relative to most other measures.

But this week’s retail sales data suggests otherwise. Retail sales rose by just 0.2% m/m in February, after declining 1.2% in January. Only 5 of the 13 major categories (Chart 2) saw gains last month while revisions to January showed an even weaker pace of retail spending than previously reported. Moreover, spending at bars & restaurants – the only services-based metric included in the retail report – plunged by 1.5% or the largest monthly pullback in two-years. This bears close watching, as discretionary services spending has been a key driver underpinning the strength of the consumer in past years.

For now, the Fed appears comfortable to sit tight and wait for more clarity on both the policy and data front. This will not come from any one policy announcement or data reading, suggesting policymakers will remain on the sidelines for at least another few months before making their next move.