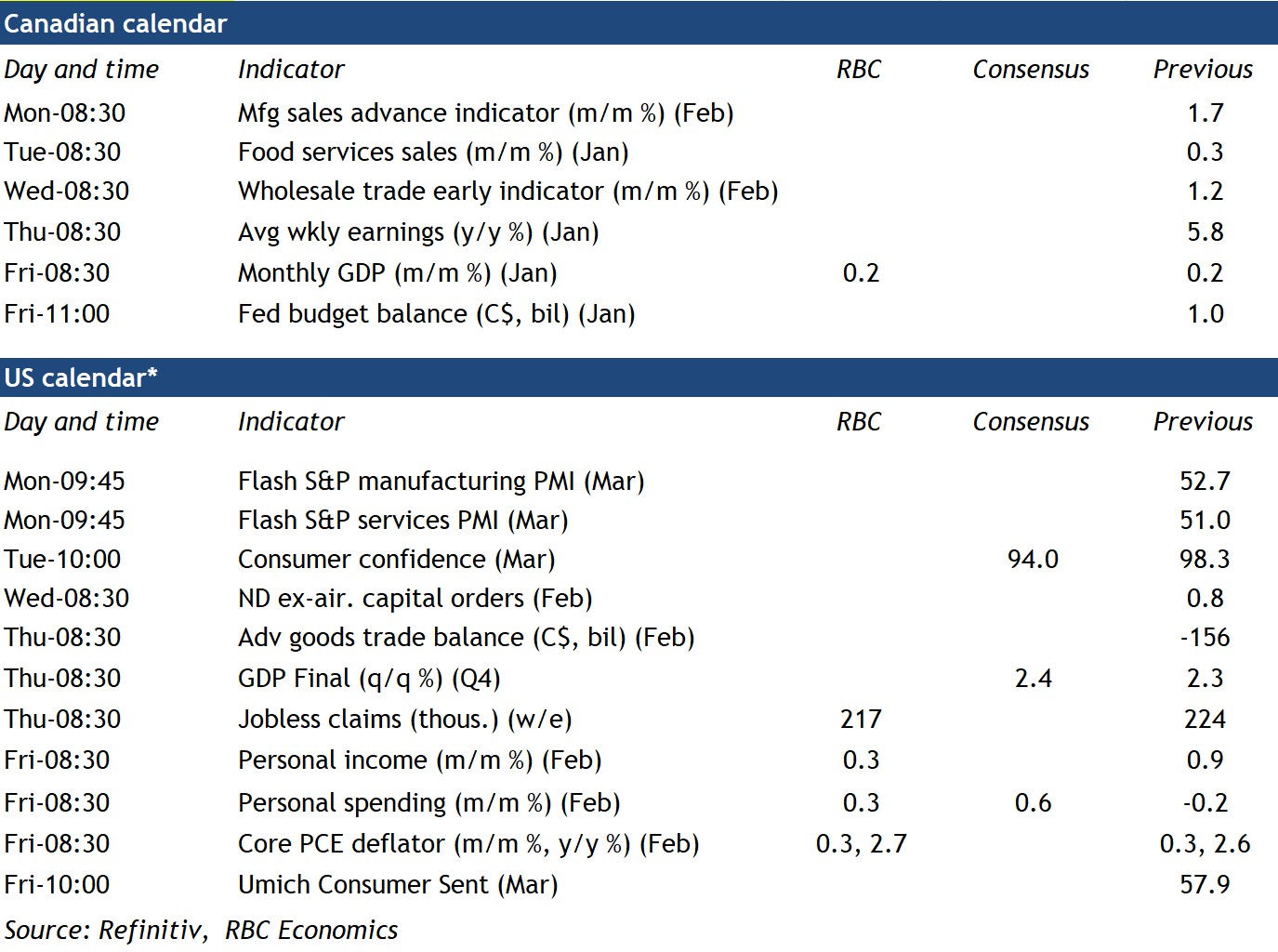

{kind=link}

U.S. tariff risks continue to cloud the outlook for Canada, but January’s gross domestic product report should show further signs of life in an economy that broadly underperformed global peers in the previous two years.

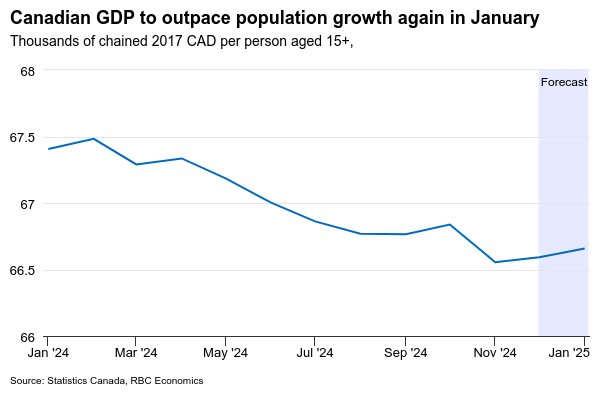

We expect GDP increased 0.2% from December—adding to the 0.2% increase in December and slightly lower than Statistics Canada’s preliminary estimate a month ago.

Output in the transportation sector likely bounced back after the end of the labour disruptions in postal service and ports that weighed on output in earlier months. Non-conventional oil production in Alberta posted another solid 4% gain in January (by our count), following a 2% increase last month, and drilling activity picked up after declining in November and December. Wholesale sale volumes also posted an 0.8% increase.

Outside of these sectors, we expect the report will be more mixed. Retail sale volumes declined by 1.1% in January and home resales declined by 3.3%, building on a 5% drop in the prior month. We also expect manufacturing output will be little changed following declines in the previous two months. Still, the increase in overall GDP we expect would outpace population growth for a second consecutive month, and comes alongside employment growth and a lower unemployment rate in 2025.

Moving forward, these more positive but, ultimately, backward-looking data releases will continue to be overshadowed by intensifying international trade risks. By our count, the effective U.S. tariff rate on imports from Canada has increased by about 2-2 ½ percentage points (provided Canadian exporters are largely able to comply with CUSMA/USMCA rules.) But details of another round of planned U.S. tariffs in April still vague. We continue to expect the implementation of tariffs and the threat of more to come will weigh on consumer and business confidence and spending in the months ahead.

Week ahead data watch

- Job openings from the Survey of Employment, Payrolls and Hours have been declining, and we will continue to watch those closely next Thursday.

- We expect U.S. personal spending edged higher in February, consistent with an earlier reported increase in retail sales. We expect the core PCE deflator (the U.S. Federal Reserve’s preferred inflation gauge) edged up 0.3% from January and 2.7% from a year ago.