{kind=link}

Summary

- The FOMC voted unanimously today to keep its target range for the federal funds rate unchanged at 4.25%-4.50%. The Committee also decided to dial back the pace of quantitative tightening by allowing only $5 billion worth of Treasury securities to roll off the Fed’s balance sheet every month.

- In a change from the last post-meeting statement, today’s statement noted that “uncertainty around the economic outlook has increased,” an apparent reference to the uncertain outlook for U.S. trade policy and the effects it may have on the economy.

- The median GDP growth forecast for this year in the Summary of Economic Projections was downgraded while the core PCE inflation forecast was pushed higher.

- The median dot in the dot plot continues to look for 50 bps of rate cuts this year. However, there are now more FOMC members who think that less than 50 bps of easing would be appropriate than members looking for more than 50 bps of rate cuts.

- We look for 75 bps of easing by the end of the year, which we acknowledge is not a view that is currently shared by most FOMC members.

- If the economic slowdown that we forecast eventually leads the FOMC to place more weight on the “full employment” objective of its dual mandate than on its “price stability” objective, then we believe the Committee will ultimately conclude that lower rates are warranted and commence an easing cycle this summer.

FOMC Keeps Rates Unchanged While Dialing Back Pace of QT

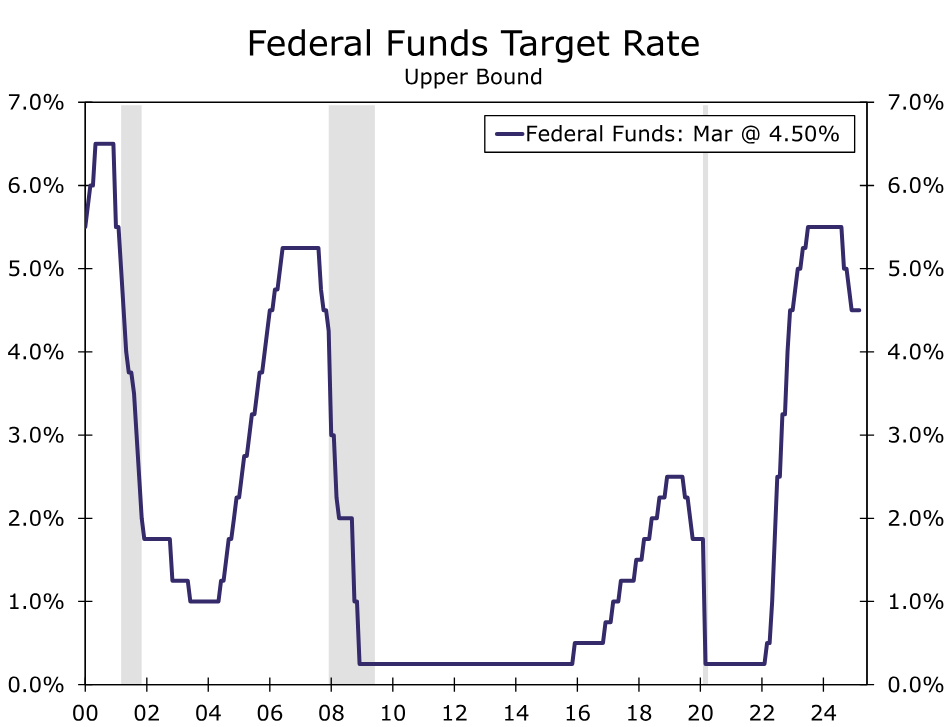

As universally expected, the Federal Open Market Committee (FOMC) held its target range for the federal funds rate unchanged at 4.25%-4.50% at its policy meeting today, a decision that was unanimously supported by all 12 voting members of the Committee. After cutting rates by a cumulative 100 bps at three consecutive policy meetings between September and December, the FOMC has now been on hold for the past two meetings (Figure 1).

The FOMC also decided today to slow the pace of quantitative tightening (QT). Beginning in April, the Federal Reserve will allow only $5 billion of Treasury securities to roll off its balance sheet every month. Previously, the monthly cap was $25 billion per month. (The Fed will continue to allow up to $35 billion worth of mortgage-backed securities to roll off the balance sheet every month). Governor Waller, who wanted to keep the monthly cap for Treasury securities unchanged at $25 billion per month, dissented in the decision related to QT. As we discussed in detail in our most recent “Flashlight” report, technical considerations related to the looming debt ceiling decision may have played a role in the FOMC’s decision to slow the pace of QT. That said, Chair Powell implied in his post-meeting press conference that the FOMC likely will not return to a faster pace of QT once the debt ceiling debate is resolved.

Heightened Uncertainty

In deciding to keep rates on hold today, the Committee continued to note in its post-meeting statement that “economic activity has continued to expand at a solid pace.” The statement also continues to characterize inflation as “somewhat elevated.” Indeed, the year-over-year change in the core PCE deflator, which most Fed officials believe is the best measure of the underlying rate of consumer price inflation, stood at 2.6% in January, above the FOMC’s target of 2%. Notably, the Committee stated that “uncertainty around the economic outlook has (emphasis ours) increased,” which likely is a reference to the uncertainty surrounding tariff policy. This heightened uncertainty appears to have led the FOMC to change its view of the balance of risks. Previously, the Committee judged “that the risks to achieving its employment and inflation goals are roughly in balance.” Today’s statement merely noted that “the Committee is attentive to the risks to both sides of its dual mandate.” In short, it’s difficult to assess where the balance of risks lie if the outlook for economic policy is considerably clouded.

We Look for Policy Easing Later This Year

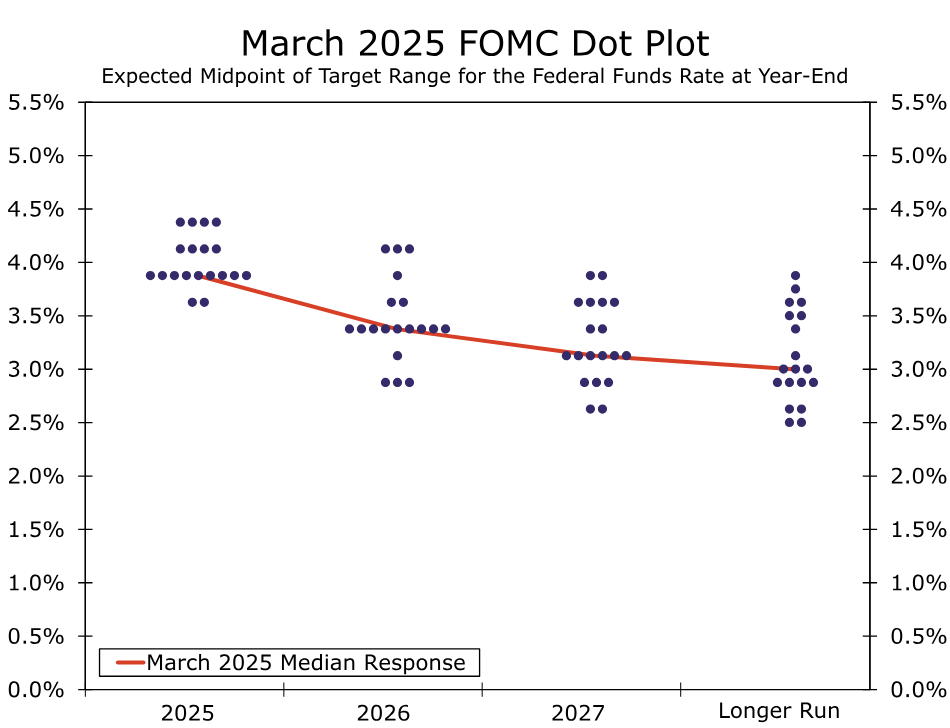

The central bank also released the quarterly Summary of Economic Projections (SEP) that contains the Committee’s macroeconomic forecasts. As we prognosticated in our recent “Flashlight” report, the median GDP growth forecast for 2025 was lowered from 2.1% in the December SEP to 1.7% while the median forecast for core PCE inflation was pushed up from 2.5% to 2.8%. In other words, the current SEP looks for a bit more stagflation in 2025 than the previous SEP, which was released in December. The median forecast in the so-called dot plot continues to look for 50 bps of rate cuts this year, although four FOMC members now think that only 25 bps of rate cuts will be appropriate this year while another four members think it will be appropriate to keep rates on hold all year. (Figure 2). In December, three members looked for 25 bps of rate cuts in 2025 while only one member thought it would be appropriate to refrain from easing this year.

We have a more dovish view of monetary policy in coming months than the collective FOMC. We forecast that the FOMC will reduce its target range for the federal funds rate by 75 bps by the end of the year. (Only 2 of the 19 FOMC members think it appropriate to cut rates by 75 bps by the end of 2025). As we discussed in more detail in our most recent U.S. Economic Outlook, our forecast is predicated on our assumption that the Trump administration will lift tariff rates meaningfully, with most trading partners retaliating, in coming months. Although the levies should cause only one-off increases in prices of tariffed goods, the resulting modest rise in inflation should only be temporary, at least in our view. Meanwhile, the negative hit to GDP growth likely will cause the unemployment rate to rise, which could remain elevated if policy remains restrictive. We do not know what individual FOMC members have assumed about trade policy in coming months. But if the economic slowdown that we forecast eventually leads the FOMC to place more weight on the “full employment” objective of its dual mandate than on its “price stability” objective, then we believe the Committee will ultimately conclude that lower rates are warranted and commence an easing cycle this summer.

That said, we agree with the FOMC’s assessment that uncertainty regarding the economic outlook has increased, and we think it likely that the Committee will keep rates on hold again at its next meeting on May 7. The outlook for Fed policy clearly depends on the evolution of economic policy, especially trade policy, in coming months. In our view, the FOMC’s near-term policy decisions will be dictated by incoming economic data.