.){kind=link}

Canadian Highlights

- Markets were on edge this week as the U.S. followed through on its 25% tariffs on steel and aluminum imports.

- Trade tensions haven’t fully translated into economic data yet. Canadian household wealth rose for the fifth consecutive quarter while debt servicing costs fell to the lowest level since 2022.

- The Bank of Canada cut its policy rate by 25 basis points to 2.75% this week, but Governor Tiff Macklem warned that monetary policy can’t fully offset a trade war.

U.S. Highlights

- All three major indexes briefly entered correction territory this week as the trade fight continued to escalate. The sentiment has partially recovered by Friday boosted by the news that the government shutdown was averted.

- Consumer and business confidence continued to slide amid high trade uncertainty, while inflation expectations continued to spike.

- Continued policy and inflation uncertainty will keep the Federal Reserve on the sideline at its meeting next week until some time this summer.

Canada – Bank of Canada Cuts But Can’t Fight a Trade War

Markets were on edge this week. The S&P/TSX fell about 1.5% for the week and is now down 5% from its January peak. Long-term bond yields initially dipped as recession fears grew amid escalating trade tensions, but rebounded later in the week, closing a few basis points higher. The Canadian dollar remained under pressure, ending the week unchanged at 69 cents U.S.

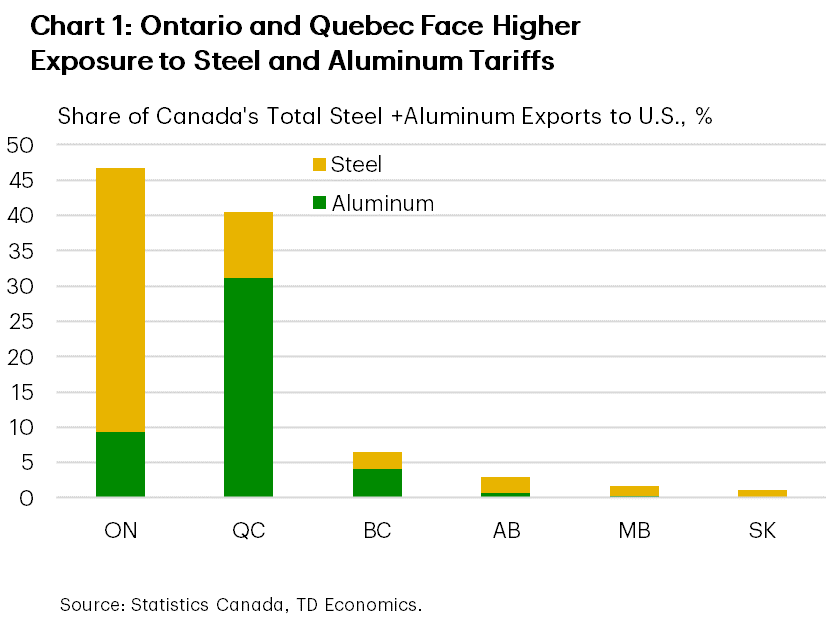

The so-called “golden era” promised by President Trump is giving way to a “period of transition”, marked by heightened market volatility as trade policies shift. On Wednesday, the U.S. administration imposed 25% tariffs on Canadian steel and aluminum imports.

While steel and aluminum exports make up only about 6% of Canada’s total merchandise exports, the regional impact is more significant. Quebec produces most of Canada’s aluminum exports, while Ontario supplies the bulk of its steel exports to the U.S. (Chart 1). In response, Canada implemented new counter-tariffs on Thursday, adding to the $30 billion in U.S. imports already subject to duties as of last week.

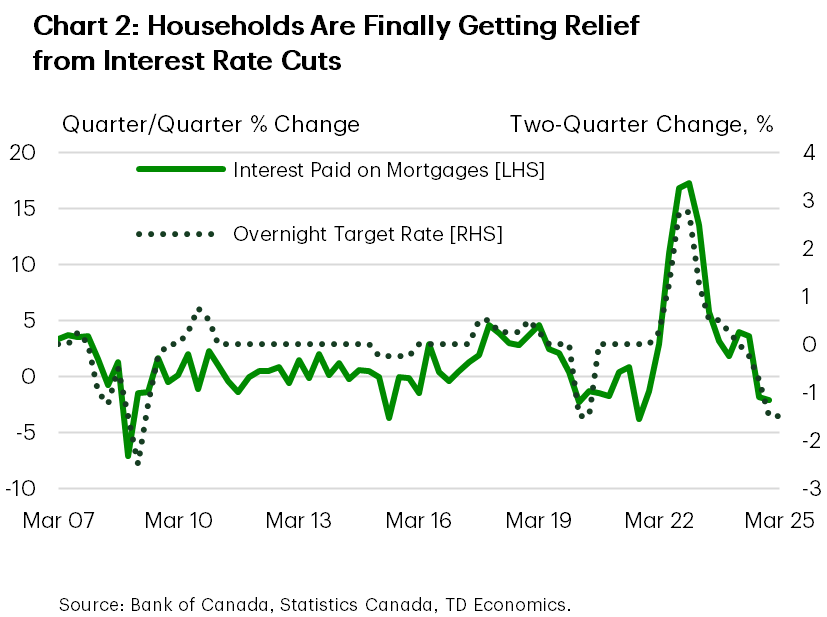

So far, tough trade rhetoric hasn’t fully translated into economic data. This week’s report on Canadian household balance sheet showed that wealth increased for the fifth consecutive quarter, supported by gains in financial and real estate assets. Importantly, households’ debt service ratio fell to its lowest level since 2022, reflecting the cumulative impact Bank of Canada rate cuts, which are now translating into lower aggregate interest payments (Chart 2). In turn, this should provide households with some financial relief, potentially supporting consumer spending.

However, uncertainty is weighing on sentiment. Preliminary results from the Bank of Canada’s business and consumer surveys suggest households are becoming more cautious with spending, while businesses – particularly in the manufacturing sector – are revising down their sales outlooks. Our latest TD debit and credit card spending data, set for release on March 17th, indicate that consumers are shifting toward precautionary savings and are cutting back on discretionary purchases. Still, given a solid hand-off into 2025, we anticipate one more quarter of above-trend growth in Q1 2025.

Beyond that, the outlook becomes murkier. The Bank of Canada cut its policy rate by 25 basis points to 2.75% this week, but Governor Tiff Macklem warned of “a new crisis” where “monetary policy cannot offset the impacts of a trade war”. This is because sustained tariffs risk lifting inflation, threatening the BoC’s hard-won 2% target. This limits how far the BoC can cut rates to support demand. As long as the pressure on tariffs remains in place, the BoC should keep its dovish bias, and we expect two more quarter-point cuts to take the overnight rate to 2.25% by June. Although markets are currently pricing in only a 50% chance of a cut next month.

U.S. – Markets Tumble as Continued Trade Fights Reignite Recession Concerns

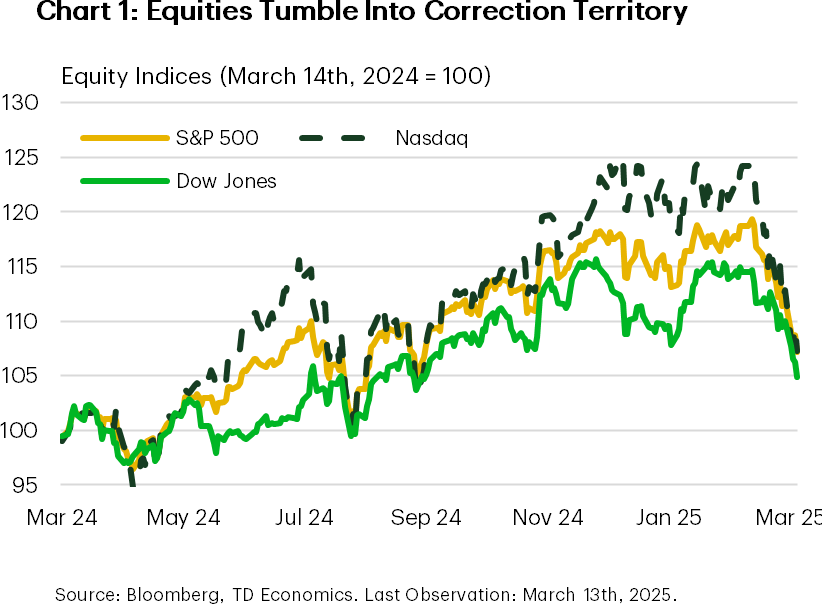

This has been another one of those “everything, everywhere, all at once” weeks. Investors were caught between a rock and a hard place, forced to navigate both a trade dispute and the threat of a potential government shutdown. Trade risks remain a major concern, reigniting fears of a recession and intensifying the selloff in financial markets. All three major indexes briefly entered correction territory, before retracting a bit on Friday as Senate Democrats appear to back the Republican’s stopgap spending bill that will keep the government funded through September 30th (Chart 1).

Tariff threats continued to dominate headlines this week, with the administration’s 25% steel and aluminum tariffs coming into effect on Wednesday, prompting retaliation from Canada, the E.U. and China. The E.U. imposed tariffs on $26 million of U.S. imports, while Canada imposed a 25% tariff on $30 billion worth of U.S. goods. In addition, China announced a 15% tariff on some key American farm products, such as pork, chicken, and soybeans, following the U.S.’s decision to raise the tariff rate on all Chinese imports by an additional 10% on March 4th – bringing the effective tariff rate on China to around 30%.

The recent ratcheting up of trade tensions has fueled concerns that tariffs could weight more meaningfully on growth this year and put further upward pressure on inflation. This week’s CPI report showed that inflationary pressures eased in February, with headline inflation slowing to 2.8% year-over-year down from 3% in January. While welcome, this reprieve may be short-lived as the latest numbers would have only captured the initial 10% tariff on China that came into effect on February 4th.

Business surveys indicate that inflation expectations and pricing intentions have risen, suggesting that price pressures are building in the supply chain. If tariffs remain in place, companies will eventually need to raise prices or absorb higher costs themselves. Some smaller businesses have already started raising prices. This week’s NFIB Small Business Confidence Survey showed a 10-point jump in the share of businesses increasing average selling prices.

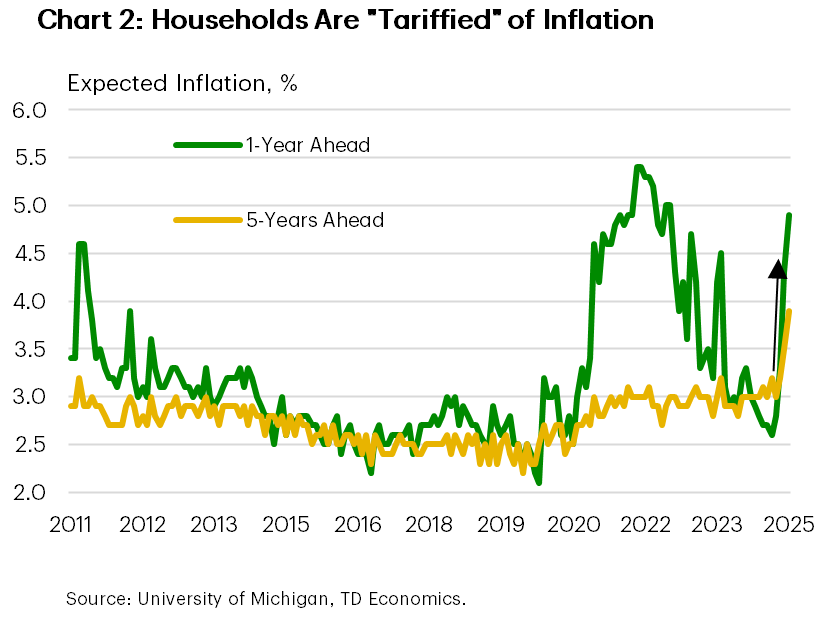

Household confidence has also been weakening rapidly, driven not only by the recent stock market selloff but also by expectations of higher inflation in the months ahead. Indeed, the March reading of University of Michigan’s survey of consumer confidence shows that after declines in the prior two months, consumer confidence continued to nosedive this March – falling to the lowest level since November 2022. Year-ahead inflation expectations surged from 4.3% last month to 4.9% in March, marking the highest reading since November 2022 (Chart 2).

Given the current storm of uncertainty, the Federal Reserve is likely to remain on hold at its next meeting next week. With inflation expectations becoming more unhinged, we expect the Fed to remain on the sidelines until some time this summer, at which point slowing economic growth will likely prompt the need for additional support in the form of lower interest rates.