and lead to softer monthly prints for both core goods and services. However, we believe growing concerns over tariffs are already affecting pricing decisions and will help to keep the pace of consumer price inflation firm overall.){kind=link}

Summary

Consumer price inflation came out of the gate strong in 2025, but price growth looks to have cooled somewhat in February. We estimate headline CPI rose 0.25% and the core index advanced 0.27%. The moderation in the core index is likely to reflect some giveback in a handful of categories that soared in January (e.g., prescription drugs, used cars, motor vehicle insurance and recreation services) and lead to softer monthly prints for both core goods and services. However, we believe growing concerns over tariffs are already affecting pricing decisions and will help to keep the pace of consumer price inflation firm overall.

Despite Moderation in February, CPI Inflation to Remain Firm

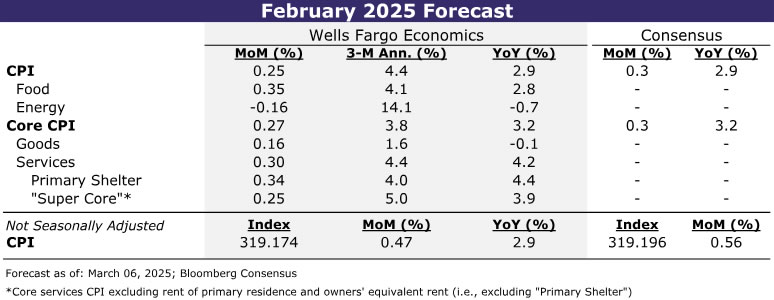

The January CPI report carried echoes of 2024 with the first key inflation read of the year coming in hot. Unlike last year, however, we expect it to be followed up by a more temperate gain in February. Headline CPI likely increased by about 0.25% in February, or roughly half the size of last month’s advance. Gasoline prices rose less than usual last month, signaling a decline in energy goods prices on a seasonally-adjusted basis. That should help keep the overall contribution from energy slightly negative despite a pickup in energy services costs from the recent strength in natural gas prices (Figure 1).

The firmer trend in food inflation that began last fall likely continued in February. We look for a 0.3% rise in food prices, which would push the three-month annualized rate up to 4.1%—the strongest clip in two years. Grocery prices look poised for another solid increase (0.4%) following the jump in producer prices for consumer foods last month and weekly data from the USDA suggesting relief on egg prices has yet to arrive (Figure 2). Slower growth in average hourly earnings for restaurant workers continues to offer some relief to food away from home, but the rebound in food-related commodity costs and the lapping of a low base comparison last February points to the cost of dining out picking up on a year-ago basis.

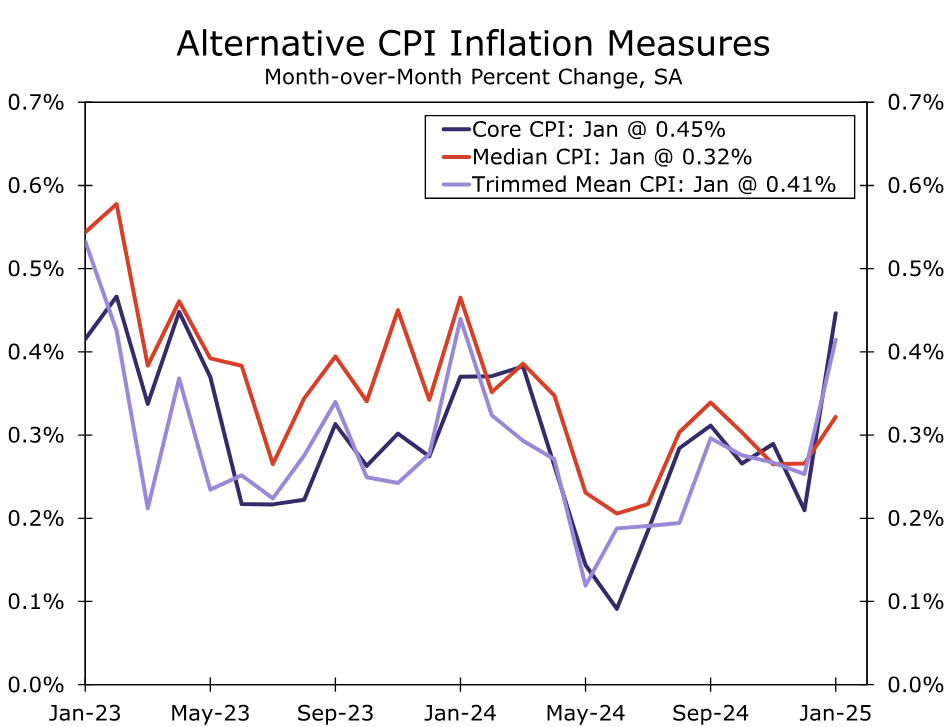

Excluding food and energy, we estimate CPI inflation cooled in February with a 0.3% gain (0.27% unrounded). Whereas January 2024’s upside surprise was broadly based, strength at the start of this year was more narrowly driven and suggests price pressures are not quite as persistent as first meets the eye. Specifically, the core CPI’s rise of 0.45% exceeded the median CPI increase (0.32%) and trimmed mean CPI increase (0.41%)—a reversal from what played out last year when January’s strength was followed in February and March (Figure 3).

When looking across the core, we see a number of categories ripe for reversion toward their recent trend. Among them are prescription drugs after the largest monthly gain on record in January (2.5%). On the services side, we see scope for slowing in motor vehicle insurance, whose 2.0% jump in January looks elevated versus industry rate data, and in recreation services and motor vehicles fees, where prices in each saw their largest monthly increases in at least four years.

The anticipated giveback in these categories should lead to a slowing in non-housing services inflation both on a monthly (0.3%) and annual basis (3.9%). We have penciled in a slight pickup in primary shelter costs in February, however. While any impact of the LA wildfires is likely to be a choppy and drawn out affair, February marks the first month in which rents may be affected (see the Topic of the Week section of our January 24 Weekly for more detail). All told, we expect core services to advance 0.3%, which would nudge the year-over-year rate down to a three-year low of 4.2%.

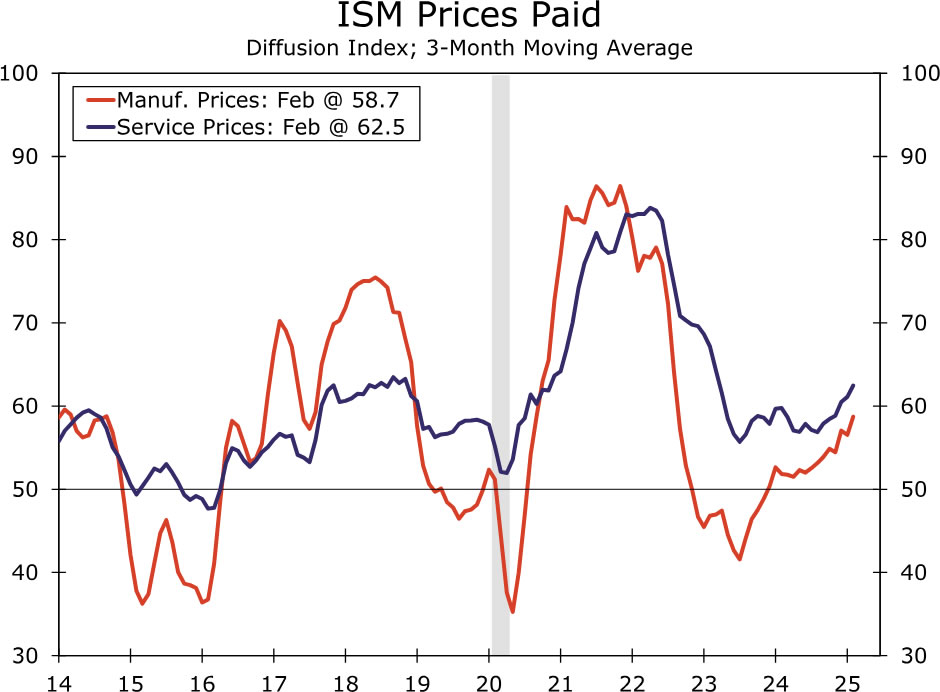

Core goods inflation is likely to have slowed slightly in February with a 0.2% monthly increase. In addition to the anticipated payback for prescription drugs, wholesale auction prices for used cars point to the CPI used vehicle index moving back down in the near term. But elsewhere, we expect the uptrend in goods prices to continue. Goods prices have historically risen the most during the first two months of the year, leaving the potential for residual seasonality in the data to boost February prices on seasonally-adjusted basis. And unlike the tariffs under the first Trump administration, the additional 10% tariffs on Chinese imports implemented at the start of the month included all consumer goods. Furthermore, while even larger tariffs on Canada and Mexico were postponed, the saber-rattling may have been enough to change some firms’ pricing decisions already. Notably, both the ISM manufacturing and services surveys reported a pickup in prices paid last month (Figure 4), while the Atlanta Fed’s measure of businesses’ one-year inflation expectations rose to a seven-month high in February.

While February’s CPI report is likely to deliver an initial taste of tariffs, it is likely to be just the start. The implementation of a further 10% tariffs on Chinese goods and the follow-through on 25% tariffs on goods from Canada and Mexico, even with some carve outs, is poised to stoke inflation in the near term. Although we expect both headline and core inflation to tick down on a year-over-year basis in February, we anticipate it will start moving back up this spring and remain stuck near 3% for the duration of this year despite further easing in shelter inflation and growing signs of consumer fatigue.