{kind=link}

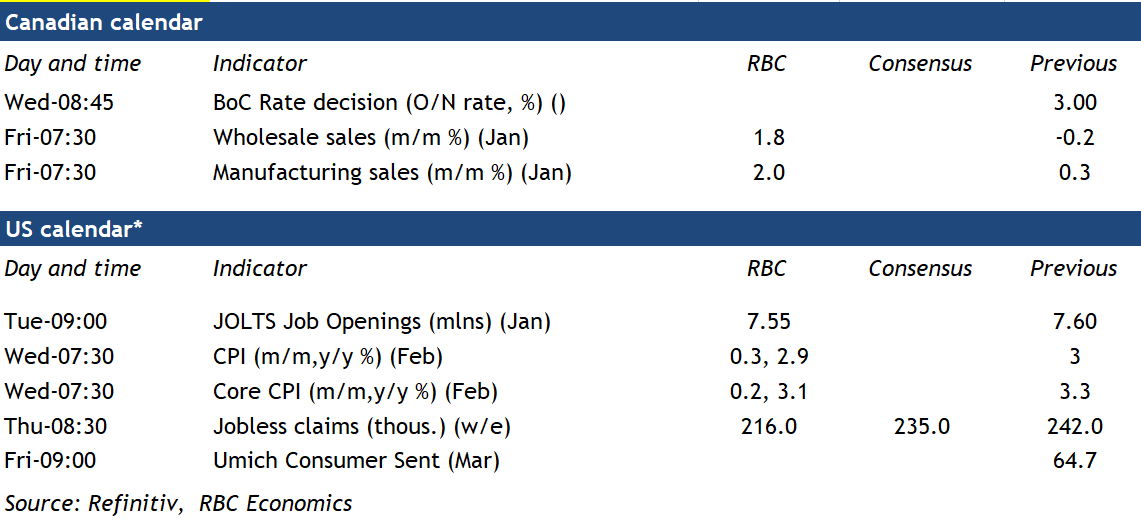

We expect the Bank of Canada interest rate decision on Wednesday will be a very close call as our base case forecast assumes it will forego a rate cut for the first time since April 2024, but U.S. trade risks could still easily tilt odds towards a seventh consecutive cut.

Outside of tariff risks, backward looking domestic demand in Canada is showing enough signs of recovering early in 2025 for the BoC to pause their cutting cycle. Inflation has remained around the central bank’s 2% target, but would be higher without the federal sales tax holiday that lowered prices for items like restaurant dining. Q4 GDP growth surprised substantially on the upside. There was some evidence of softening Canadian employment in trade sensitive sectors in February. But the unemployment rate is still below levels late last year, consistent with the view that the economy-wide production gap (the key driver of future inflation pressures in the BoC’s policy framework) had begun to narrow into 2025.

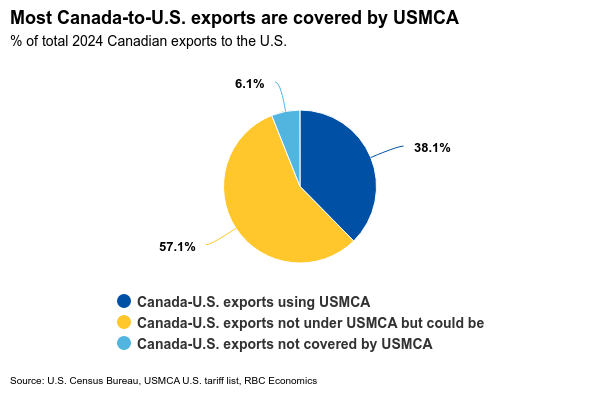

The latest round of 25% blanket tariffs on Canada and Mexico have already begun to be rolled back with reports that USMCA-compliant trade will be exempted. Only 38% of Canadian exports to the U.S. last year used CUSMA/USMCA but we expect the bulk of trade (potentially 90%+ based on our own early calculations) can be brought into compliance relatively quickly.

The reality is trade risks are not going away. Steel and aluminium tariffs are still set to be imposed in the coming week with broader reciprocal tariffs to be announced in April. What U.S. trade policy will look like week-by-week (or even hour-by-hour) is still highly uncertain. And that uncertainty itself is already threatening to choke off a recovery in Canadian business investment.

But as we have noted before , the BoC will also need to consider any potential fiscal policy response – which is better able to provided targeted, timely support than changes in interest rates that impact economic conditions more broadly and only with substantial lags. Interest rates are still relatively high. At 3%, the overnight rate remains near the top of the 2.25% to 3.25% range that the BoC views as having a neutral impact on the economy. But Governor Macklem has also explicitly highlighted the limits of monetary policy as a tool to offset tariff shocks, and the BoC still needs to strike balance between supporting the economy through uncertainty while guarding against adding unnecessarily to future inflation.