. Meanwhile, the Canadian 10-year yield was lower by around 20 bps to 3%.){kind=link}

Canadian Highlights

- President Trump signalled that broad-based tariffs on Canadian exports will come into effect on March 4th. The wait is on to see if they are indeed implemented.

- If enacted, these tariffs would hit just when the economy is on the mend. Canada’s economy advanced at a healthy 2.6% annualized rate in Q4, bolstered by consumer spending.

- Although markets currently judge it as a near 50/50 proposition, we think the Bank of Canada will cut their policy rate on March 12th.

U.S. Highlights

- The Fed’s preferred inflation metric, core PCE, rose 2.6% year-on-year in January, in-line with expectations and continuing to converge with the Fed’s 2% target.

- The Conference Board’s Consumer Confidence Index showed a material decline in February, as tariffs weighed on sentiment and boosted inflation expectations.

- The President announced an additional 10% tariff on China set to take effect on March 4th, in concert with the previously announced 25% tariffs against Canada and Mexico.

Canada – Deadline 2.0

Markets were in a dour mood this week, directly related to President Trump’s repeated threat of broad-based tariffs to begin next Tuesday, March 4th. There was a bit of “will he, won’t he”, with respect to these threats. The signal from the Oval Office on Monday appeared to indicate that they’ll proceed. This message got muddied on Wednesday during a U.S. cabinet meeting, where it seemed as though they could be punted for another month. Unfortunately, Canadians got concerning clarification from President Trump on Thursday that they are indeed set to be enacted next week. The Canadian dollar was down over one cent USD in the week (as of writing). Meanwhile, the Canadian 10-year yield was lower by around 20 bps to 3%.

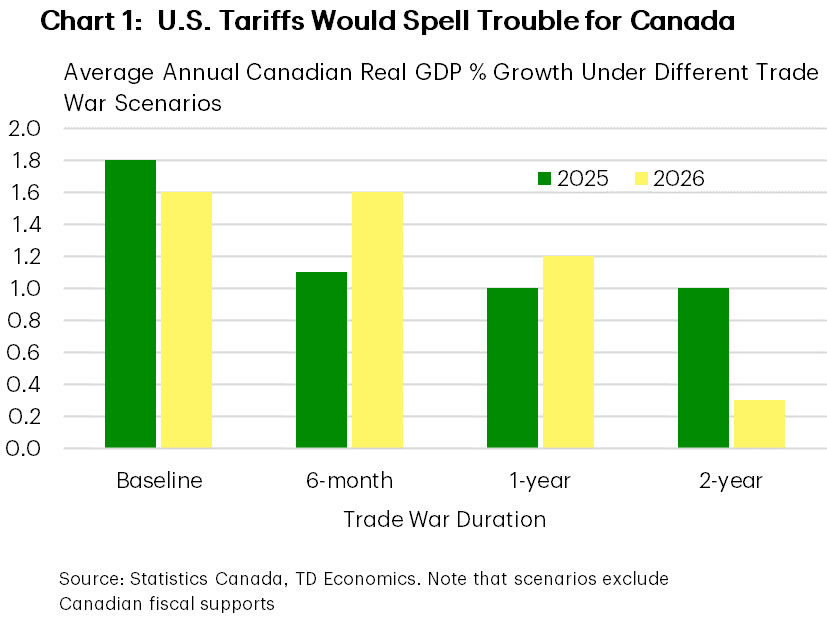

Of course, we’ve done this dance before. Just a few weeks ago, U.S. tariffs were paused at the 11th hour after negotiations between President Trump and Prime Minister Trudeau. So, it remains to be seen if March 4th will mark the beginning of a harmful trade war, or if cooler heads will prevail again. When forecasting the potential damage to the Canadian economy, the one unknown is how long punitive 25% tariffs would be in effect. Our latest Q&A presents economic growth outcomes that could unfold depending on how long U.S. tariffs (and reciprocal ones from Canada), are in place. A two-year trade war would hamper growth well into 2026, whereas as a six-month duration could see growth rebounding smartly next year, although both scenarios would see deteriorating conditions in 2025 (Chart 1).

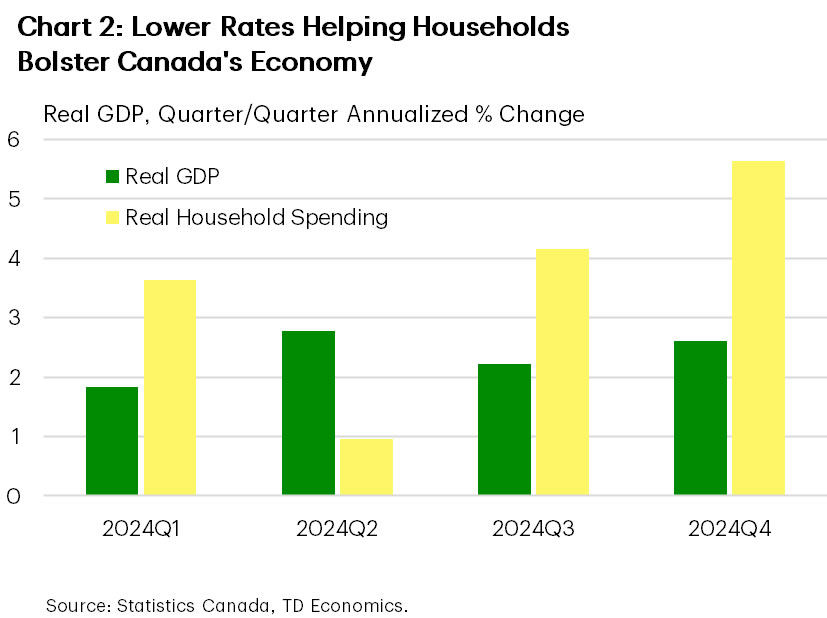

Although there’s never an ideal time for a trade war, high tariffs would thump the Canadian economy just as it’s on the mend. Indeed, job growth has been robust for three straight months in the Labour Force Survey (LFS), and even this week’s payroll jobs report (which had been lagging it’s LFS counterpart) showed an increase in employment in December. What’s more, investment intentions in the capital and repair expenditures survey pointed to an above-trend 6% gain in non-residential spending by Canadian companies and governments in 2025 (see commentary). However, this result comes with the huge caveat that it only partially captured tariff threats, which really ramped up after the survey’s cut-off date. And, in the marquee release of the week, Canadian real GDP jumped 2.6% annualized in the fourth quarter. Details of the report were favourable as well, with lower interest rates, government stimulus measures, and decent income growth propelling a huge gain in consumer spending (Chart 2).

In the wake of the robust GDP data, markets pared back their expectations of a rate cut by the Bank of Canada on March 12th. However, markets are still placing about a 50% chance that a cut will take place. We think the Bank will cut their policy rate next month, even with what is a solidly improving current economic backdrop. In our view, it’s prudent from a risk-management perspective to insulate against downside growth risks by cutting the policy rate again. Of course, if a Canada-U.S. trade war does start next week, this would virtually lock in another cut next month. And now, we wait.

U.S. – Angst Builds with Tariff Threats

The final week of February included an update on the health of the American consumer, and the Federal Reserve’s preferred inflation metric. Meanwhile, financial markets remained cautious as the prospect for broad-based tariffs to go into effect next week against the nation’s three largest trading partners kept sentiment subdued. As of the time of writing, the S&P 500 was down 2.3% on the week, while the 10-year Treasury yield fell nearly 20 basis-points to 4.24%.

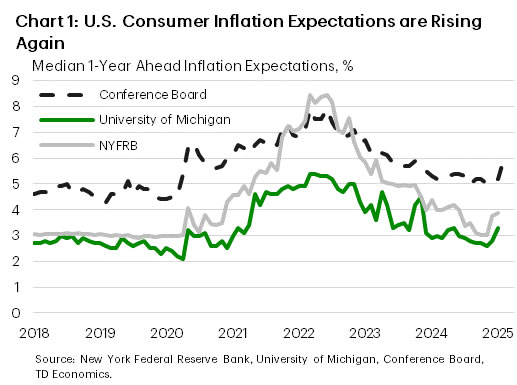

The impact of tariff threats on consumer confidence has partially contributed to the negative sentiment in financial markets over the past week. Last Friday, the University of Michigan consumer sentiment index fell to its lowest level in 15 months, and this was followed by the Conference Board Consumer Confidence Index dropping sharply this week to an eight-month low. The Conference Board’s survey also noted that mentions of trade and tariffs had risen to a level last seen in 2019. While we saw real personal consumption expenditures fall 0.5% month-on-month in January in data released this week, severe weather undoubtedly played a role.

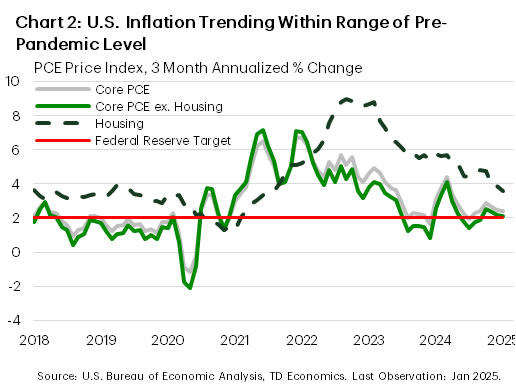

At the same time, consumer surveys have also begun to show signs of rising inflation expectations (Chart 1), which could present a risk for the Federal Reserve’s mission to return inflation to their 2% target. Core PCE inflation, the Fed’s preferred metric, rose 2.6% year-on-year in January. Looking at the three-month annualized percentage change, momentum has continued to trend favorably (Chart 2) with both the housing and excluding housing subcategories within range of pre-pandemic levels. However, these metrics remain slightly elevated on aggregate, which supports the Federal Reserve’s holding pattern. This, combined with rising inflation expectations, is also likely why several of the Federal Reserve officials we heard from this week favored a patient approach to future monetary policy adjustments, particularly amid elevated uncertainty. Market pricing has the Fed returning to rate cuts in June, with one additional rate cut before year end – in line with the median FOMC official projection from December.

Looking ahead to next week, there will be plenty to keep markets on their toes. First up will be the potential for the 25% tariffs on Canada and Mexico, plus the new additional 10% tariff on China announced this week, to be implemented next Tuesday. If an eleventh-hour resolution cannot be achieved again, then significant trade disruptions would likely follow. President Trump will also be delivering his State of the Union address on Tuesday, which may include new policy considerations. Lastly, we’ll round out the week with the employment report for February on Friday, which will be the last employment report released prior to the Fed’s next meeting in mid-March. Consensus expectations currently call for 158k new jobs to have been created this month, which would likely be viewed positively by the Federal Reserve. All-in-all, there will be plenty of information released next week to guide expectations in the months ahead.