{kind=link}

- The ECB meeting next week is expected to end with yet another 25bp rate cut, bringing the policy rate to 2.5%, 150bp lower than the peak last year. While the cut decision is relatively straightforward, divergences in the ECB GC members’ assessment of the policy stance is starting to show, thus a key question will be whether the ECB will start now to soften its assessment on monetary policy restrictiveness.

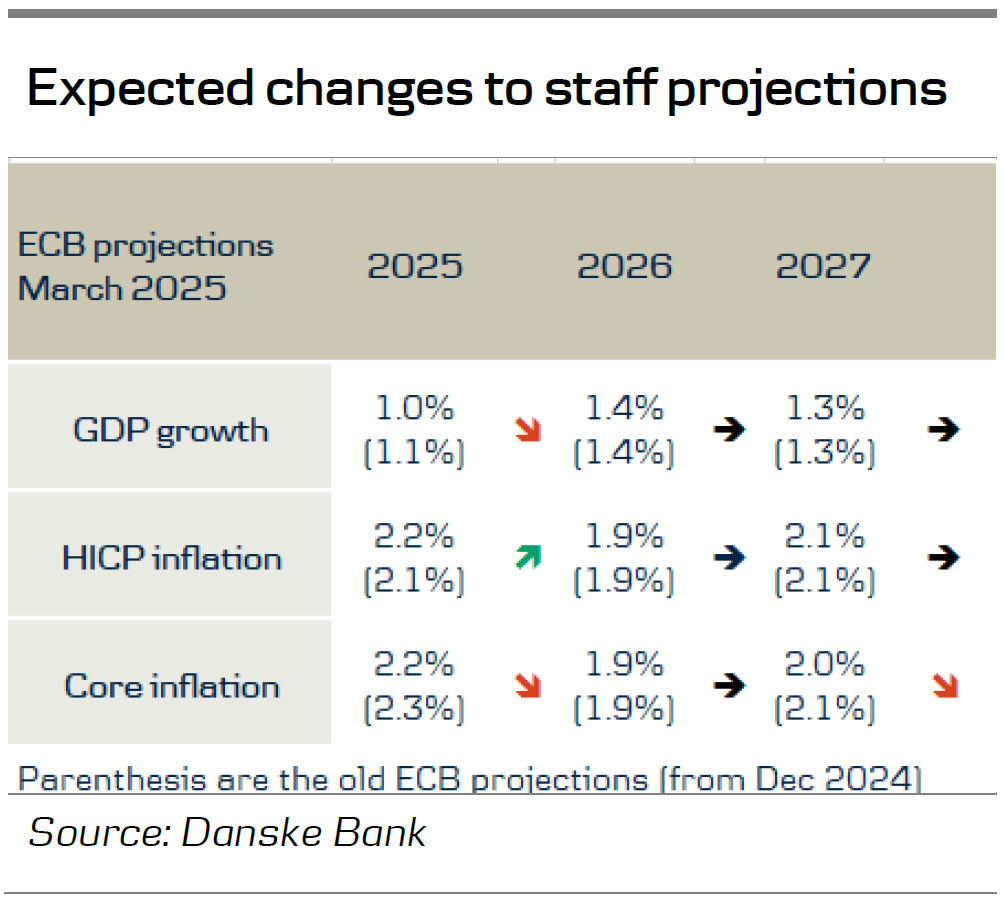

- We continue to expect the three-tiered reaction function to prevail (inflation outlook, underlying inflation and strength of monetary policy transmission) and the data dependency to be reiterated. We expect the new staff projections to show higher inflation this year (2.3% y/y, December projection: 2.1% y/y) due to higher energy prices, while core inflation, more importantly, is likely to be revised down to 2.2% y/y for 2025 from its 2.3% level in December. We expect no changes to the growth forecast except a small downward revision to 1.0% y/y for 2025 due to a lower growth overhang from 2024.

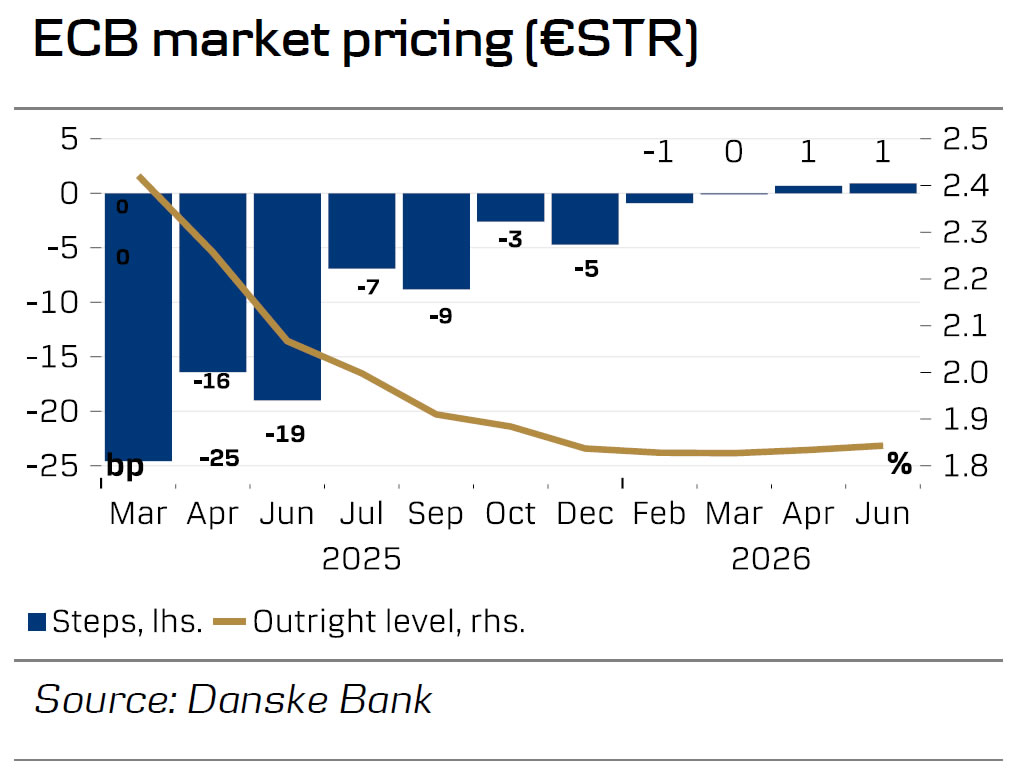

- Markets are pricing another 59bp worth of rate cuts this year, following next week’s 25bp rate cut. We expect ECB to cut more than this to end with a terminal rate of 1.5% in H2 this year, albeit risks are slightly skewed to the upside.

Diverging views

The ECB GC members have started to position themselves more vocally ahead of the upcoming ECB meetings, and at least two camps have emerged. These differences do not seem significant enough to affect the policy decision of a rate cut that we and markets expect in March, but there appears to be a significant difference of opinion on the risks emerging as the easing cycle is maturing. The views may converge once more data comes in, but with the difference in views, we can expect front-end volatility to be higher than it would be otherwise.

We identify the hawkish camp, with comments from Schnabel and Wunsch, against the dovish camp, with comments from Panetta and Stournaras. The difference of views emerges from the degree of restrictiveness that we currently have. Last week, Schnabel said that she is ‘no longer sure whether it is still restrictive’, while the dovish camp was of the view from the ECB assessed in January that ‘financing conditions continue to be tight, also because monetary policy remains restrictive’. To nuance this discussion, one first has to agree on what levels of interest rate are actually restrictive, neutral and accommodative, and here we also expect to see a diverging set of views, which we discussed in our previous ECB preview ahead of the January meeting. In the end, we expect the ECB to guide that the past policy rate cuts are starting to transmit to the economy and it is warranted to assess the required level of monetary policy restrictiveness on an ongoing basis, thus using a more vague language on the exact restrictiveness level. We believe this is a compromise that both the doves and the hawks can subscribe to.

To guide for a halt or pause?

The ECB’s influential GC member Schnabel last week suggested that it may be time to discuss when to pause or halt the rate cuts that commenced in summer last year. We find this discussion too early to give a conclusion on whether there should be a pause or a halt now, but it is naturally something that eventually will come. At the current juncture, no one gains from committing to either outcome for the April meeting, and that means more volatility in front end pricing can be expected.

Staff projections to show higher headline inflation but lower core and growth

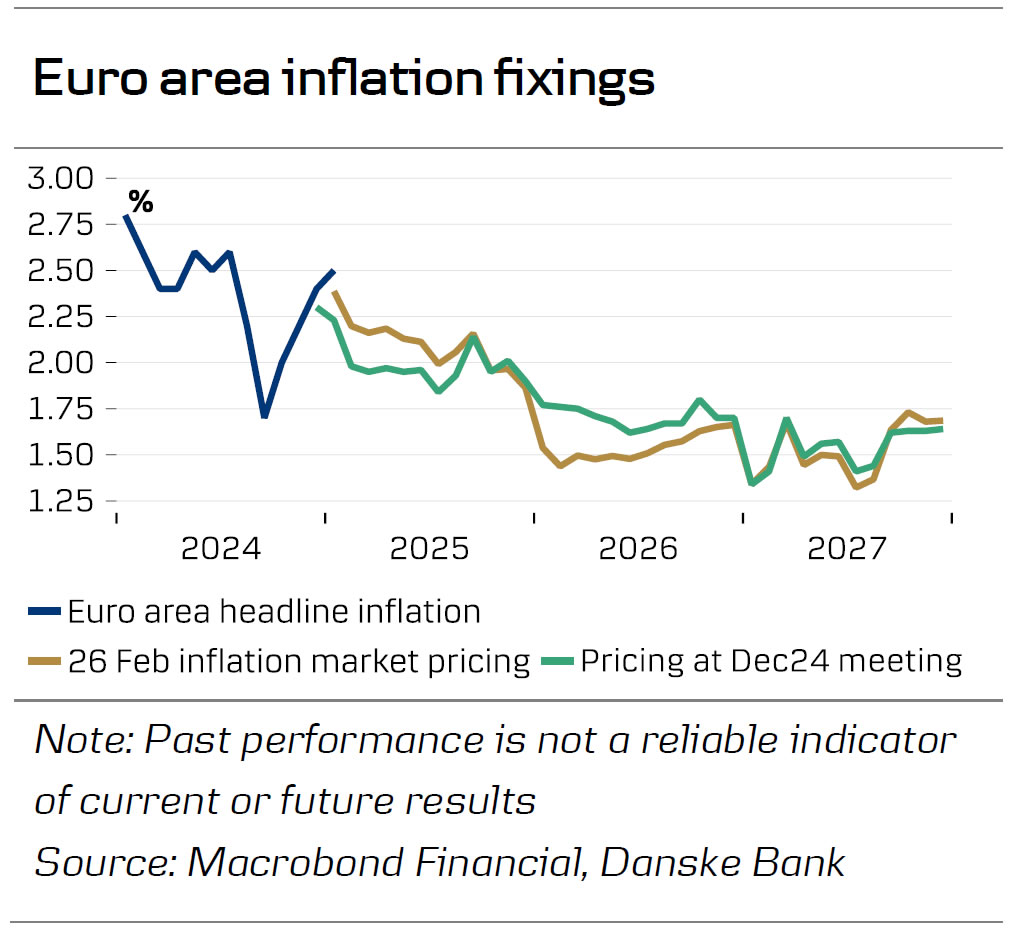

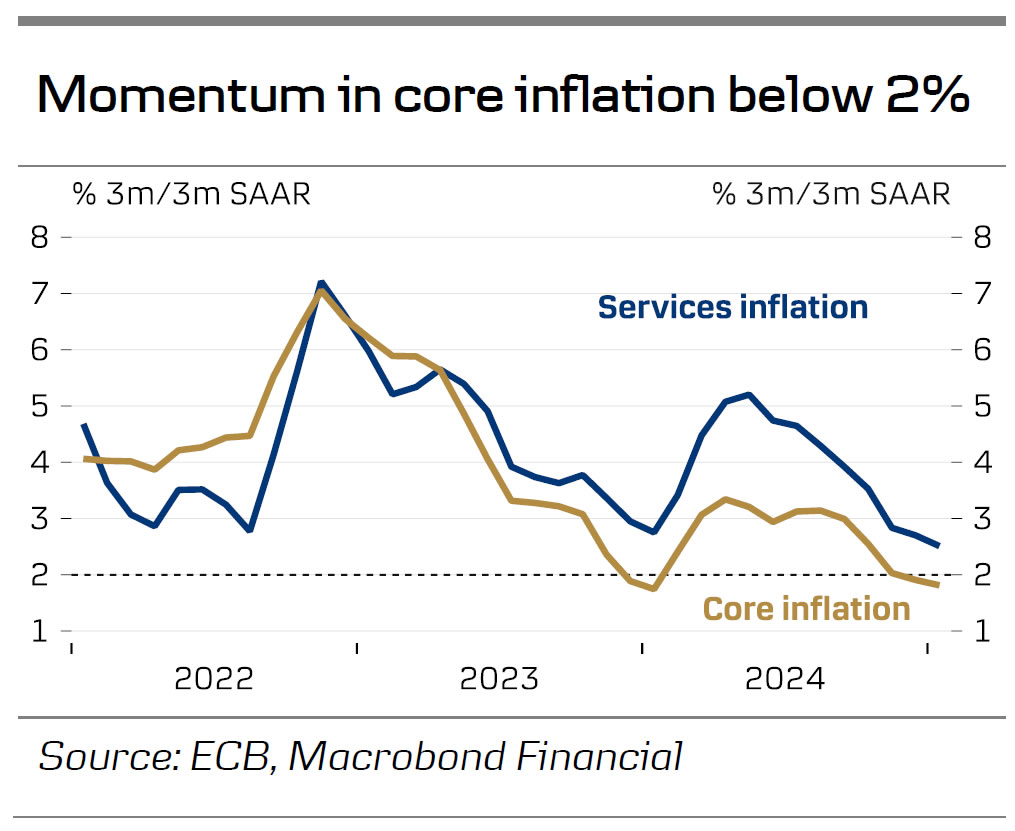

Inflation rose to 2.5% y/y in January mainly due to energy inflation. While energy prices have generally come down following talks of a potential end to the war in Ukraine, there is considerable uncertainty on the headline inflation estimate for this year due to the cut-off date for the technical assumptions which is likely to be on 12 February. At that point in time the gas price and futures were 19% higher compared to the December cut-off date, while it was about 5% higher for oil. We thus expect the staff projections to revise up the headline inflation forecast to 2.2% y/y for this year from 2.1% y/y. More importantly, we expect a small lowering of the core inflation forecast to 2.2% y/y (from 2.3%) due to lower wage growth and weaker than expected core inflation in January. The December staff projections estimated Q1 25 core inflation at 2.7% y/y, which seems unlikely as an average given the 2.7% print in January and as base effects in services inflation are set to pull it significantly lower in February and March (the February number is expected to be released on Monday 3 March).

So, while the headline inflation forecast is expected to be revised up, we do not expect that to change the ECB’s view on inflation, as the cooling momentum in core inflation continues. Lagarde will likely receive questions in the case of a revision, which she can use as an opportunity to highlight the risks to the inflation profile from energy prices, but at the same time stress the falling momentum in core, anchored inflation expectations, and that inflation is expected close to target in 2026 and 2027.

Growth in the final quarter of 2024 turned out to be weaker than projected by the ECB. The December staff projections saw GDP rising by 0.2% q/q while the actual number was just 0.05% q/q due to a contraction in Germany while Spain grew 0.8% q/q. Momentum has since increased a bit as indicated by the PMIs that recorded 50.2 in both January and February, following an average of 49.3 in Q4, due to a rise in the manufacturing PMIs. The labour market has also remained resilient with employment rising 0.1% q/q in the final quarter of 2025 and the unemployment rate recording 6.3% in December. Hence, the new projections will likely continue to show 0.3% q/q growth in all of 2025, but the yearly growth figure is expected to be revised down to 1.0% y/y from 1.1% y/y due to a smaller overhang from Q4 24. For 2026 and 2027 we do not expect any changes to the projections

Another well-telegraphed meeting should have limited market impact

Despite several non-traditional drivers influencing EUR/USD – including the German election, developments around a potential Ukraine ceasefire, and ongoing US economic policy uncertainty – the pair has stabilised around 1.05 in recent weeks. In this context, the March ECB meeting provides clarity for markets, as another rate cut is fully priced in. A data-dependent, meeting-by-meeting approach with no pre-commitment to a specific rate path is likely to be maintained, limiting market impact. With the next cut not fully priced until June, the forward rate path will be the key focus.

A central question is whether the ECB will drop its ‘restrictive’ policy label, a move that would signal a hawkish stance and pose upside risk for EUR/USD. While some policymakers, including Schnabel, have called for a discussion on this, the statement is unlikely to make such a shift just yet, as the ECB seeks to avoid unintended hawkish signals. However, post-meeting commentary may provide insights into when such an adjustment could occur.

For EUR/USD, the February US jobs report, released the day after the ECB meeting, is likely to be more pivotal. The recent USD depreciation has narrowed the rate differential gap, and our short-term model suggests EUR/USD is now trading closer to fundamentals, as the tariff risk premium has eased. In the near term, we expect the pair to remain range-bound around 1.05. However, if softer US data momentum persists, risks are skewed toward some tactical upside. On a strategic basis, our outlook for stronger relative structural growth in the US keeps us bearish on EUR/USD, with a move toward parity expected over the next 12 months.