. That said, the focus is on next week, when the second update of fourth quarter GDP and January’s Personal Income and Outlays report will give a fresh look at economic momentum and the first look at the Fed’s preferred inflation metric for 2025. Fed speakers provided some insights this week on why the data-dependent approach is key when looking to understand how inflation will evolve in a still-healthy economy.){kind=link}

Canadian Highlights

- Headline inflation for the month of January rose to 1.9% year-on-year, while price pressures built in core inflation measures.

- Canadian retail sales surged in December, registering its largest monthly gain in nearly three years. Spending fatigue likely set-in in January.

- Tariff-related uncertainties may be trickling into housing markets as existing home sales took a step back in January.

U.S. Highlights

- Fed Speakers this week emphasized the need for a data-dependent approach to policy decisions.

- As a result, next week’s inflation data in the Personal Income and Outlays Report for January will be closely watched.

- From our lens, the Fed is likely to remain on pause until the second quarter of this year, delivering two cuts by year end, as healthy economic activity supports the labor market and price growth.

Canada – Inflation and (Hockey) Elation

Canada, the spotlight is yours. Team Canada trumped the Americans in a hard-fought hockey game worthy of an applause for both teams. Hockey scores weren’t the only thing on the ticker as Canadian economic data was headlined by a warm inflation print and complimented by a very upbeat consumer spending report. Elsewhere, momentum in home sales halted in January, a relative weak spot amid the broader strength in other data. Taken together, markets have pared back the probability of a 25 basis point (bp) cut at the next Bank of Canada (BoC) rate announcement on March 12th to around 25%. That said, much will happen between now and then, including the outcome of President Trump’s plan to move forward with his threatened 25% tariffs (10% on energy) on Canadian imports.

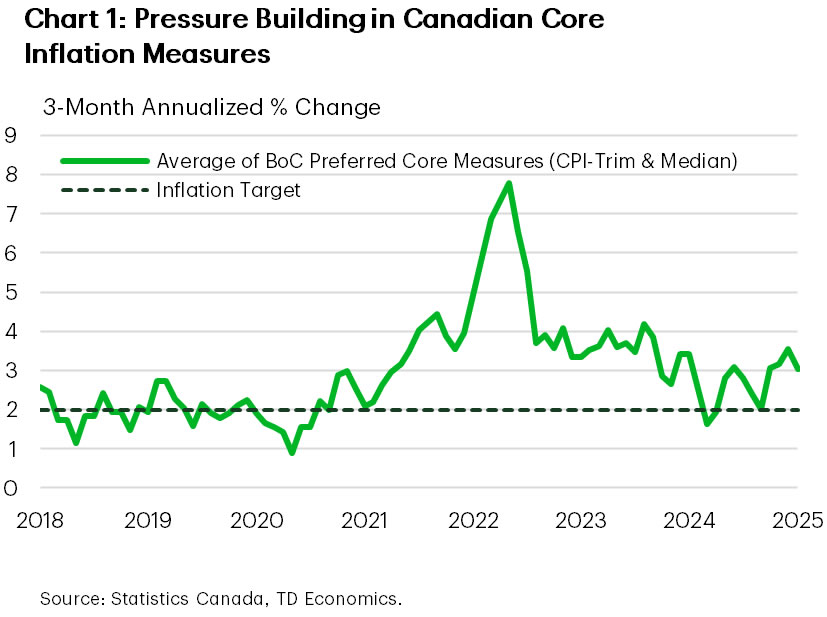

Inflation for the month of January edged up to 1.9% year-on-year (y/y), with rising energy prices making the biggest contribution to headline growth. Price growth was partially offset by the GST/HST holiday, while food price inflation found some respite, falling for the first time in nearly eight years. Headline inflation has stabilized around the Bank’s 2% target, though near-term risks are tilted to the upside as the end to the tax break will lead to higher inflation in coming months. The Bank’s preferred core inflation measure ticked up to 2.7% y/y and has hovered above 3% on a 3-month annualized basis for the past several months (Chart 1), something coming into greater focus as the BoC deliberates its next move.

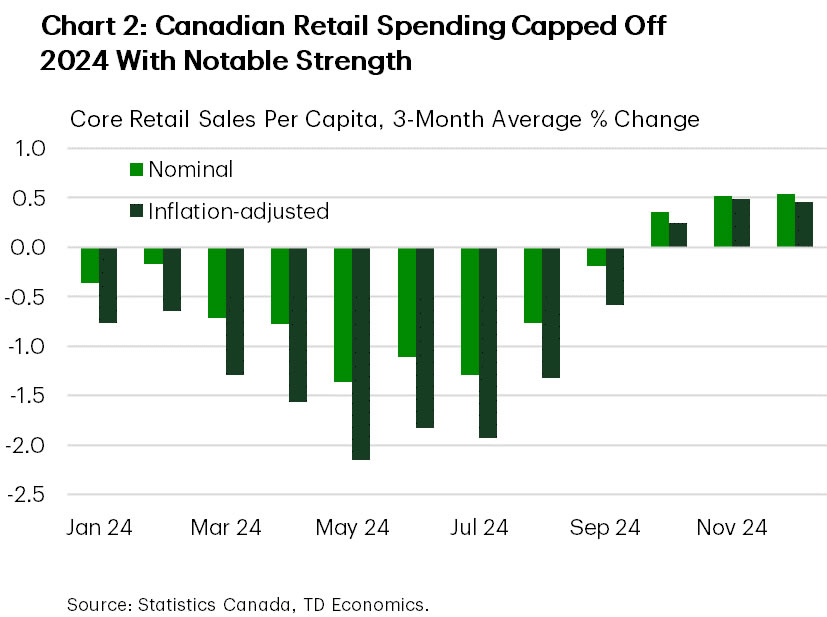

The cumulative 200 bps in interest rate easing since mid-2024, combined with the GST/HST tax break supported a 2.5% m/m surge in December retail spending, the largest increase in almost three years. Inflation-adjusted spending has strengthened over the past few months (Chart 2), supporting our call for an above-trend reading for Q4-2024 GDP growth. Even as spending momentum slows in the first quarter, the consumer is expected to be a pillar of strength for overall growth in 2025. That said, tariff uncertainty could stymie consumption progress to the extent that U.S. policy negatively affects Canada’s job market and wages.

Housing was the only dull point this week, as existing home sales slipped by 3% m/m in January. This was coupled with a surge in new listings that popped by the largest seasonally adjusted amount on record, pulling markets to the lower end of balanced market conditions. Tariff uncertainty may have weighed on buyer sentiment towards the end of January, but easing price pressures and further interest rate cuts should maintain a solid foundation for the housing market in coming quarters.

So where to from here? Our recently released Q&A discusses how the BoC may react to trade war scenarios. To take out insurance against escalating trade tensions, we think the BoC will prioritize the downside risk to growth and front-load interest rate cuts over the first half of the year, bringing the policy rate to 2.25%, the lower end of the Bank’s neutral range estimates.

U.S. – Data Dependent Decisions

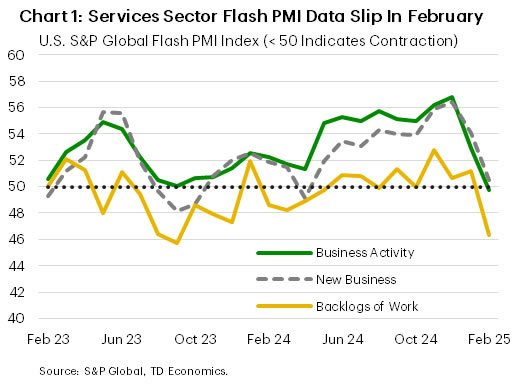

In the absence of major economic data, equities and Treasury yields were a smidge below where they started the week after reacting to a flash PMI release on Friday that suggested shrinking activity in the services sector in February (Chart 1). That said, the focus is on next week, when the second update of fourth quarter GDP and January’s Personal Income and Outlays report will give a fresh look at economic momentum and the first look at the Fed’s preferred inflation metric for 2025. Fed speakers provided some insights this week on why the data-dependent approach is key when looking to understand how inflation will evolve in a still-healthy economy.

At the start of the week Board member Christopher Waller gave a speech in Sydney with a title that left very little ambiguity, “Disinflation Progress Uneven but Still on Track. Rate Cuts on Track as Well.” The speech clearly outlined his views, including that monetary policy is restrictive and “putting downward pressure on inflation”, while economic momentum is holding up. Vice Chair Jefferson spoke later in the week, reaffirming the view that the economy and labor market are on solid footing, and the need to maintain a data dependent approach. Dr. Jefferson focused on the strength of household balance sheets and how they are supporting consumer spending. The key was that while they are generally in good position, households with lower- and middle-incomes “have less of a buffer of liquid assets than they did before the pandemic” and keeping an eye on balance sheet developments will help “inform forecasts of overall economic activity”.

One interesting concept to monitor was Dr. Waller’s acknowledgement that progress on cooling inflation in the early part of the year has been notably slow in past years. This could be attributable to “residual seasonality”– the idea that the price adjustments that usually come in the early part of the year are now bigger than they were typically and are showing up in the seasonally adjusted data that should have accounted for them. This is an interesting wrinkle, and Dr. Waller cited research that price pressures have tended to be greater in the first half of the year relative to the second in 16 of the past 22 years. The expectation then would be that even with stronger-than-expected inflation in the early part of the year, this effect should fade into the latter part of 2025, as it did in 2024.

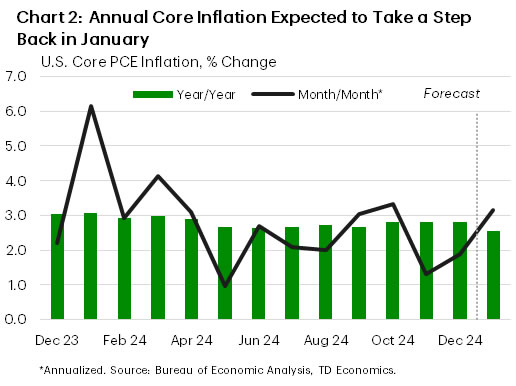

With speakers emphasizing the data-dependent approach, the focus will then be on the Personal Income and Outlays report on next Friday. The spending figures could be noisy, as cold weather and large fires in Los Angeles likely disrupted economic activity, so the focus will be on what happens with inflation. Current expectations are for the core PCE price index (the Fed’s preferred inflation gauge) to clock in at around 0.2%-0.3% month-on-month in January (2.6% year-on-year, Chart 2), but as Dr. Waller suggested even an upside surprise could be due to some residual seasonality. From our lens, the Fed is likely to remain on pause until the second quarter of this year, delivering two cuts by year-end, as healthy economic activity supports the labor market and price growth.