{kind=link}

Tuesday November 21: Five things the markets are talking about

Both U.S and German politics dominate capital market moves.

Despite the holiday-shortened trading week, the progress of the U.S tax reform legislation through congress continues to be closely watched. While in Germany, it remains unclear whether Chancellor Merkel will attempt to govern with a minority administration or that another early election in the spring will prove necessary.

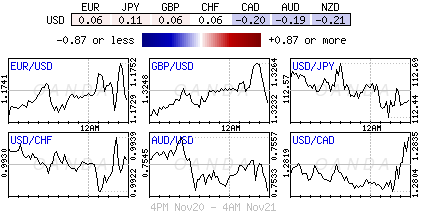

In the U.K, ‘dovish’ comments from BoE rate setter Dave Ramsden, who voted against the recent interest rate hike, seems to have had little impact on the pound (£1.3235). Investors seem to be more focused on Brexit negotiations.

Stateside, existing home sales (10:00 am EDT) are expected to rise for a second consecutive month, while Fed Chair Yellen, who yesterday confirmed that she will leave the Fed when her term ends, is scheduled to speak in New York (06:00 pm EDT). Markets will be looking for clues as to whether the Fed will hike rates next month.

Be prepared, Ms. Yellen may be asked her views on future Fed policy without her at the helm.

1. Stocks pare gains as German political impasse hits Europe

In Japan, stocks rallied overnight after large cap stocks such as automakers and manufacturers of factory automation equipment rallied, while North Korean tensions supported defence-related shares. The benchmark Nikkei ended +0.7% higher, while the broader Topix added +0.7%.

Down-under, the MSCI Asia Pacific Index jumped +0.9% to the highest in more than a week.

In Hong Kong, stocks had their best day in seven-weeks on Tuesday. The Hang Seng index was up +1.91%, while the Hang Seng China Enterprises index rose +2.91%.

In China, the blue-chip index ended at a fresh 28-month high overnight, bolstered by robust gains in brokerage firms. At the close, the Shanghai Composite index was up +0.6%, while the blue-chip CSI300 index was up +1.8%.

In Europe, regional indices trade slightly higher across the board recovering from earlier weakness, in relatively quiet trade.

U.S stocks are set to open in the ‘black (+0.1%).

Indices: Stoxx600 +0.1% at 386.7, FTSE flat at 7392, DAX +0.2% at 13080, CAC-40 +0.20% at 5351, IBEX-35 +0.2% at 10040, FTSE MIB +0.3% at 22251, SMI +0.2% at 9318, S&P 500 Futures +0.1%

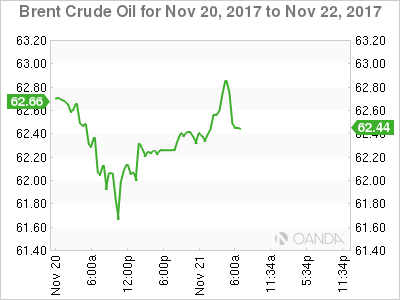

2. Oil rises ahead of OPEC meeting, gold prices steady

Oil prices remain better bid as traders look to next weeks OPEC meeting (Nov. 30) at which major crude exporters are expected to extend production cuts, though rising U.S. output continues to cap some of these gains.

Brent crude oil is up +47c at +$62.69 a barrel, while U.S light crude (WTI) is at +$56.74, up +32c.

OPEC, together with a number of non-OPEC producers led by Russia, has been restraining output this year in an effort to end a global supply overhang and support prices.

OPEC is expected to extend cuts, as storage levels remain high despite recent drawdowns, although there are doubts about the willingness of some participants to keep restricting production.

However, the biggest headache for OPEC has been a rise in U.S drilling, led by shale oil producers, which in turn is capping price gains.

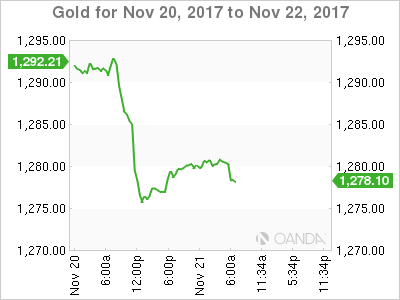

Gold prices have inched higher ahead of the U.S open; with investors waiting for tomorrow’s Fed minutes for clues on the outlook for potential rate rises. Spot gold is up +0.3% per ounce. The metal fell about -1.4% yesterday in its biggest one-day percentage drop since Sept. 11.

3. U.S yield curve flattest in a decade

The U.S Treasury yield curve has flattened to +59 bps for the first time in over a decade and is on track for its biggest monthly flattening since February 2016.

The gap between 2/10-years has narrowed -20 bps so far this month, and is at its tightest level since October 2007. The yield on 10-year Treasuries declined -1 bps to +2.35%.

In Germany, the 10-year Bund yield has fallen -2 bps to +0.35%, the lowest in almost two weeks on political uneasiness.

In the U.K, the 10-year Gilt yield has decreased -4 bps to +1.252%, the lowest in almost two-weeks, while in Japan, the 10-year JGB yield has dipped -1 bps to +0.033%, the lowest in more than a week.

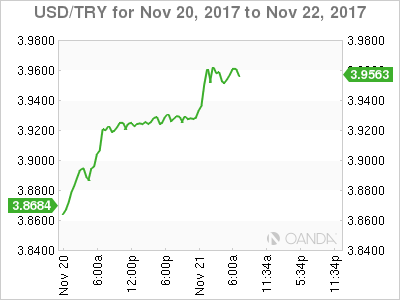

Elsewhere, Turkey’s 10-year government bond yields have jumped to a multi-year high of +12.35%, the highest in five-years. The 2-year bond also has rallied to +13.53%, a higher level than the 10-year bond, creating an “inverted” yield curve, which points to the perception of elevated near-term risks.

>

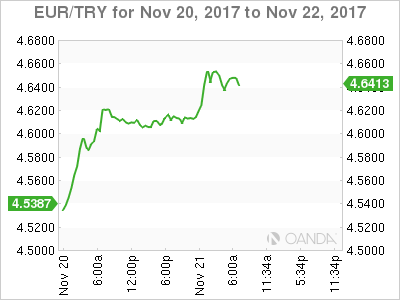

4. Turkey’s central bank lends lira support

In emerging markets, the Turkish lira (TRY) has hit an all-time low of $3.9780 outright, as recent pressure on the central bank (CBRT) from its own government and ongoing tensions with the U.S continues to pressure the currency.

Note: TRY is down some -17% against the dollar since Sept.

The central bank said it would end its interbank money-market facility for overnight transactions from tomorrow and instead fund banks via its late liquidity overnight lending rate. The move will raise average funding costs by 0.25 bps to +12.25%.

The EUR is +0.2% up against the U.S dollar at €1.1753 as improving eurozone growth takes precedent before political issues in Germany. Chancellor Merkel said she would rather have another election than form a minority government.

In the U.K, GBP/USD rises to its highest in nearly three weeks at £1.3268 – up +0.25% on the day – on reports that PM Theresa May is preparing to double her offer for a Brexit “divorce” settlement. Although this offer would still be below what the EU has demanded, it raises some optimism among investors that Brexit talks may be able to progress toward discussing a trade deal.

5. Reserve Bank of Australia (RBA) monetary policy minutes

The minutes of the last Reserve Bank of Australia (RBA) policy meeting pointed to hopes that economic growth was strengthening, but also “considerable uncertainty” over how quickly wage growth might pick up.

RBA Gov. Lowe hardly sounded ‘hawkish’ in signalling there’s little reason for now to think about higher interest rates, the Aussie dollar nonetheless took the opportunity to rebound after weeks of declines. The currency has moved back to A$0.7560 an intraday high.

Officials continue to fret anew about the country’s lack of notable wage growth – Gov. Lowe speech did not sound that hopeful of a near-term uptick in inflation.