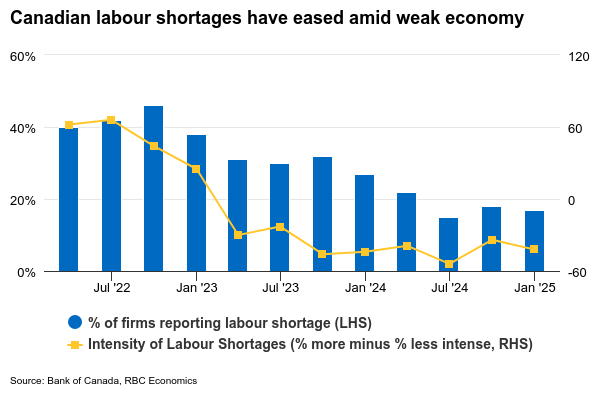

{kind=link}

The Bank of Canada is expected to cut interest rates at a more gradual 25 basis-point pace on Wednesday following 50 bps cuts in each of the two prior meetings—widening a gap with U.S. policy rates as the Federal Reserve is widely expected to forego a January rate cut.

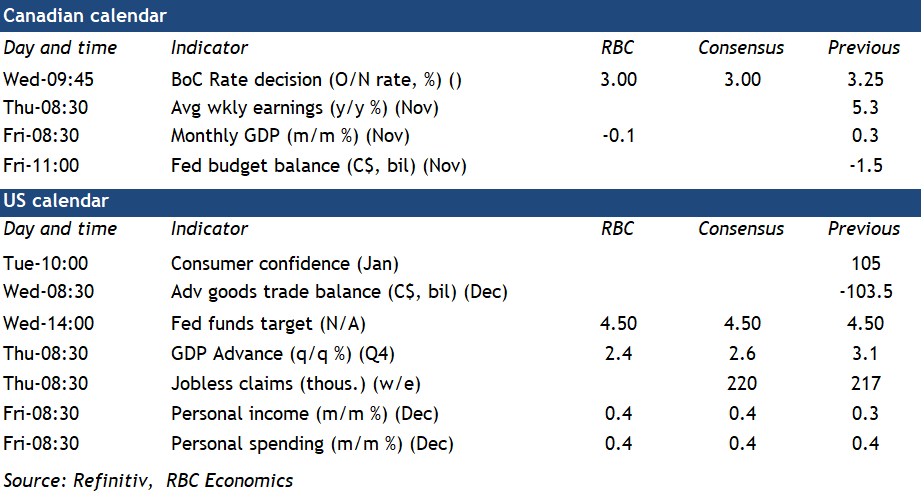

A weak Canadian economy has prompted earlier and more aggressive interest rate cuts from the BoC compared to other advanced economy central banks. But the 3.25% current overnight rate is still at the top end of the BoC’s 2.25% to 3.25% estimated range for “neutral,” which would not put upward or downward pressure on growth or inflation over time. It is also well above the 1.75% peak rate in the decade before the global pandemic.

The BoC clearly communicated in its December policy decision that with the interest rate no longer at obviously “restrictive” levels, the pace of future rate cuts would likely be more gradual, and contingent on economic data. Recent Canadian gross domestic product growth and inflation data have been mixed. Q4 GDP growth is tracking close to the BoC’s 2% October forecast and inflation, excluding indirect taxes, ticked higher in December. The BoC’s Q4 business outlook survey flagged some improvement in business sentiment. But, labour markets are still soft enough to argue that more interest rate cuts are needed for the economy to rebound enough to prevent inflation from undershooting the 2% target. We continue to expect the BoC will ultimately need to cut the overnight rate to a slightly stimulative 2% this year.

In December, Governor Tiff Macklem also flagged downside risks to the growth outlook from potential protectionist U.S. trade policy as a “major new uncertainty.” Those concerns have likely only become more pronounced with the new Trump administration threatening to impose aggressive tariffs on imports from Canada as early as next month. We expect policymakers would be more likely to cut interest rates faster and further should those downside risks materialize with the ultimately disinflationary growth and labour market implications from tariff hikes more a concern than a one-time increase in prices. See more on potential tariff impacts here.

The backdrop in the U.S. economy is very different. GDP growth remained firm in Q4 (we expect an 2.4% annualized increase to be reported in the week ahead) and progress on further reducing inflation has been slow. We continue to think an overly stimulative government spending backdrop is helping keep a floor under growth and inflation. Interest rates will need to stay higher for longer to keep growth in consumer prices on a downward trajectory back to the Fed’s 2% objective. The Fed is widely expected to stand pat on interest rates in January. Our base case assumption is the Fed will remain on the sidelines and not cut interest rates this year.

Week ahead data watch

Friday’s Canadian November GDP report should show a 0.1% contraction from October. Manufacturing, retail, and wholesale sale volumes all posted declines in November and oil production in Alberta appears to have largely reversed a sizable October gain. But, early data for December looks firmer with household spending bouncing back in part tied to delayed holiday shopping ahead of Cyber Monday and the start of the GST/HST holiday in mid-December.

We will be watching job openings in Canada’s November payroll report for signs on if a persistent rise in the unemployment rate is getting closer to its end. Job openings in October were still running 23% below year ago levels, but more recent data from indeed.com has shown some improvement late last year and into January.

We expect U.S. personal spending edged up 0.4% in December, mainly driven by higher auto sales and price-related sales increases at gas stations. U.S. personal income likely rose 0.4% in December, in line with the 0.3% increases in average hourly earnings during that month.