{kind=link}

Donald Trump was sworn in as the 47th President of the United States yesterday, unveiling an aggressive “America First” agenda that has significant implications for both domestic and global economies. Among his key priorities are large-scale deportation operations and reducing environmental regulations, signaling potential shifts in labor markets and energy industries. Trump also aims to impose higher tariffs on imports early in his presidency, a move likely to increase costs for U.S. consumers while provoking retaliatory measures from trading partners. While his policies have sparked widespread concern over trade disruptions, Trump has pledged to streamline government operations—a potential boon for economic efficiency. Furthermore, his vow to end the Russia-Ukraine conflict, though uncertain, could stabilize geopolitical tensions and benefit global markets.

Last week on the economic front, U.S. Consumer Price Index (CPI) data for December came in below expectations, suggesting inflationary pressures may be easing. Federal Reserve Governor Christopher Waller indicated that this trend could prompt multiple interest rate cuts this year if it continues, a development that may stimulate borrowing and investment. However, U.S. retail sales slightly missed expectations, hinting at weaker consumer demand.

Currencies

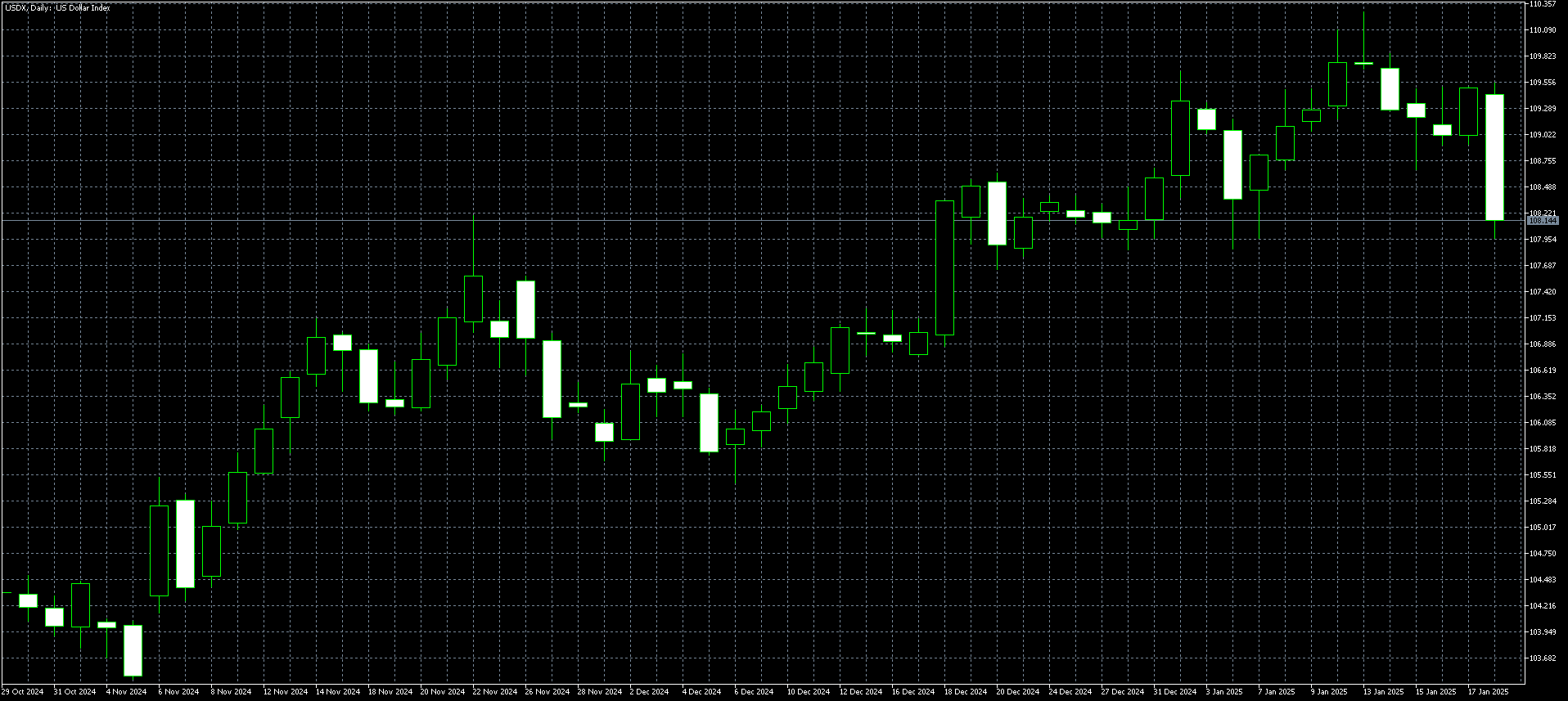

The strong rise in the USD since October has paused after last week’s weaker-than-expected U.S. inflation data. Earlier, the dollar had surged as U.S. long-term bond yields rose, with markets expecting higher inflation under Trump’s presidency. However, if Trump’s policies are seen as less inflationary than expected, the USD could weaken further.

Some analysts believe the BOJ may raise official interest rates at this week’s meeting, which could trigger a sell-off in USD/JPY and add more pressure on the dollar. At the same time, AUD/USD and GBP/USD, which have fallen sharply in recent weeks, may attract buyers, offering potential opportunities for traders.

USD Index Daily Chart

Stock Markets

U.S. stock markets have regained strength following last week’s weaker-than-expected inflation data and the official start of Trump’s presidency. The Dow and S&P 500, which had retraced much of their initial post-election rally in the past two months due to higher-than-expected U.S. interest rates, are now showing signs of recovery.

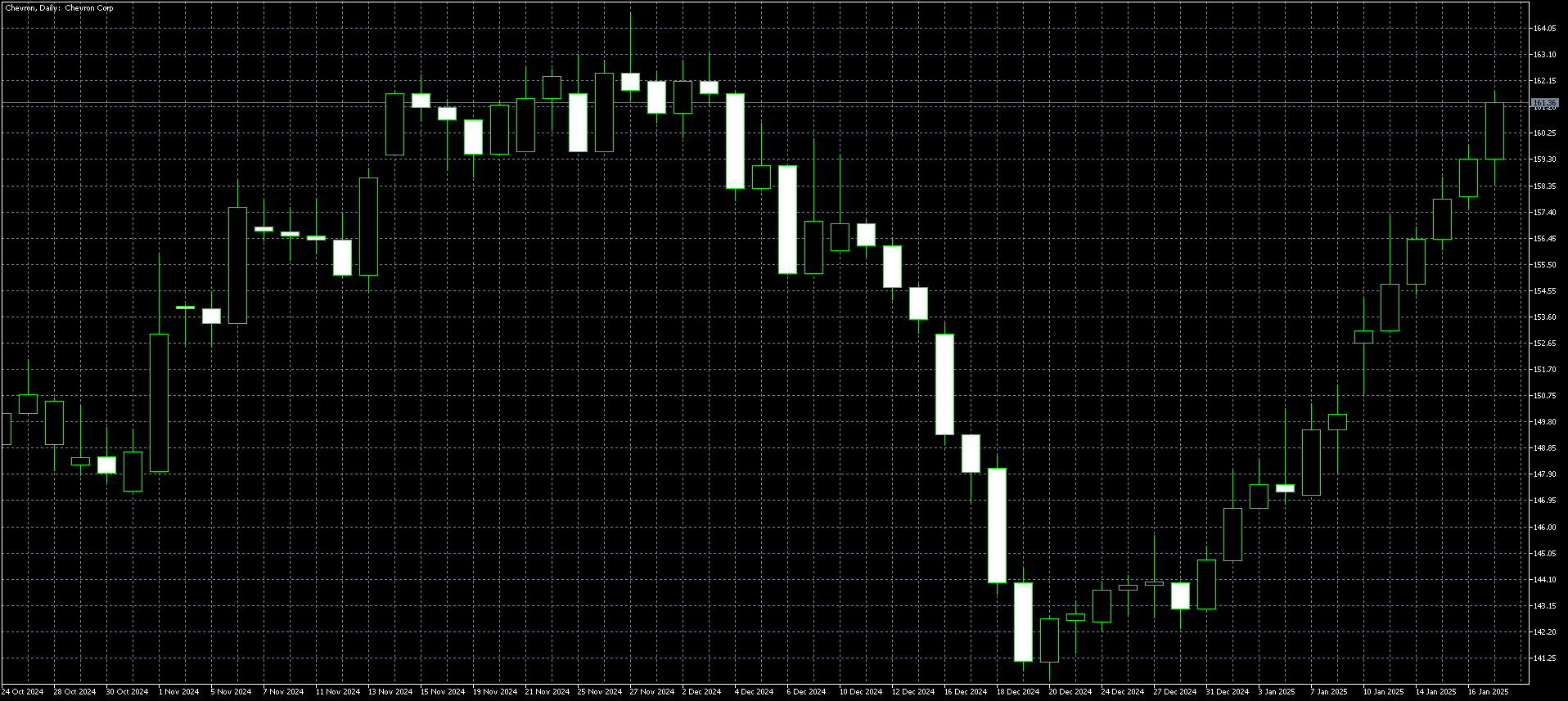

Among the sectors expected to benefit most from Trump’s policies is the oil industry, as the new administration aims to reduce regulations limiting oil extraction. Chevron, for instance, has seen significant gains this year, as highlighted in the chart below, reflecting optimism about the sector’s growth prospects.

Chevron Daily Chart

In the electric vehicle space, Tesla’s boom has slowed, but its upward trend remains intact, due to the close relationship between Elon Musk and Donald Trump. However, this alliance could end at any time, making it essential for bullish traders to stay cautious, prepare for potential losses, and consider shifting bearish if necessary.

Meanwhile, the Nikkei 225 has repeatedly failed to break through the 40,000 resistance level since Trump’s election, despite continued yen weakness. Rising living costs in Japan, outpacing wage growth, remain a key challenge for the Japanese economy, contributing to the index’s struggles.

Bond Market

The closely watched U.S. 10-year Treasury yield has climbed 1% since September, reaching 4.65%, and is approaching the key resistance level of 5% as markets scale back expectations for interest rate cuts. However, last week’s weaker-than-expected U.S. inflation data caused yields to decline, providing a boost to U.S. stock markets while pushing the USD lower. The market will also be closely watching policy announcements from Trump in the coming weeks to see if they are as inflationary as expected.

In Japan, bond yields are also trending higher as the Bank of Japan signals a possible increase in official interest rates. The 10-year Japanese bond yield has doubled over the past year to 1.19%, reflecting a notable shift in Japan’s traditionally low-rate environment.

Commodities

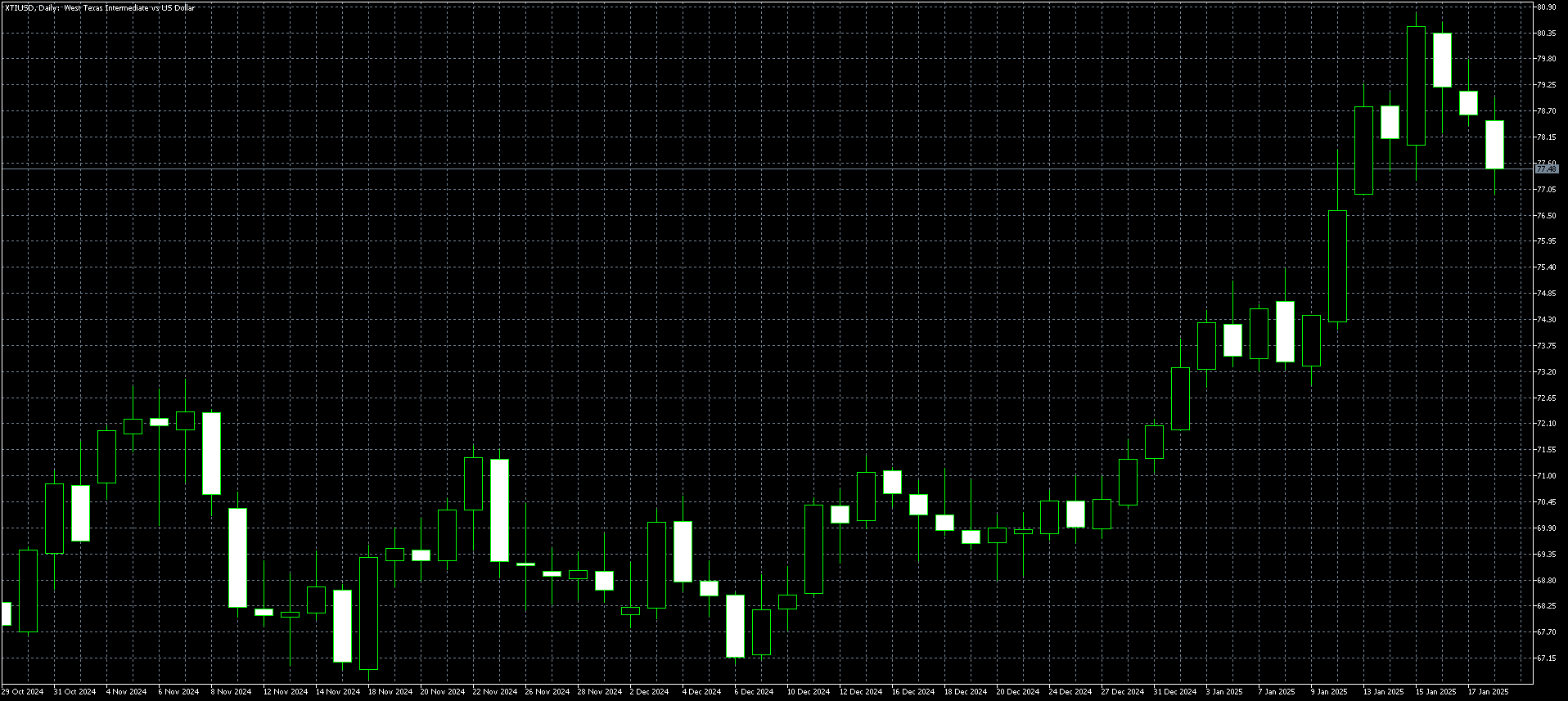

Crude oil prices have risen this year, driven by U.S. sanctions on Russia’s oil industry, which have significantly reduced global supply. Trump’s presidency is expected to further impact the oil market, as he supports expanded oil exploration in the U.S. While this could boost domestic production, Trump has also indicated he will seek ways to push oil prices significantly lower during his term. Additionally, his stated desire to end the Russia-Ukraine war, if successful, could further push oil prices down by reducing geopolitical risk premiums.

Crude Oil Daily Chart

Gold has also moved higher in 2025, despite the strong USD and higher interest rates. Investors view gold as a safe-haven asset to hedge against potential instability in the global economy should Trump’s policies create disruptions. If the USD continues to weaken, gold prices may see further upside, potentially returning to the highs set in October 2024.

Bitcoin

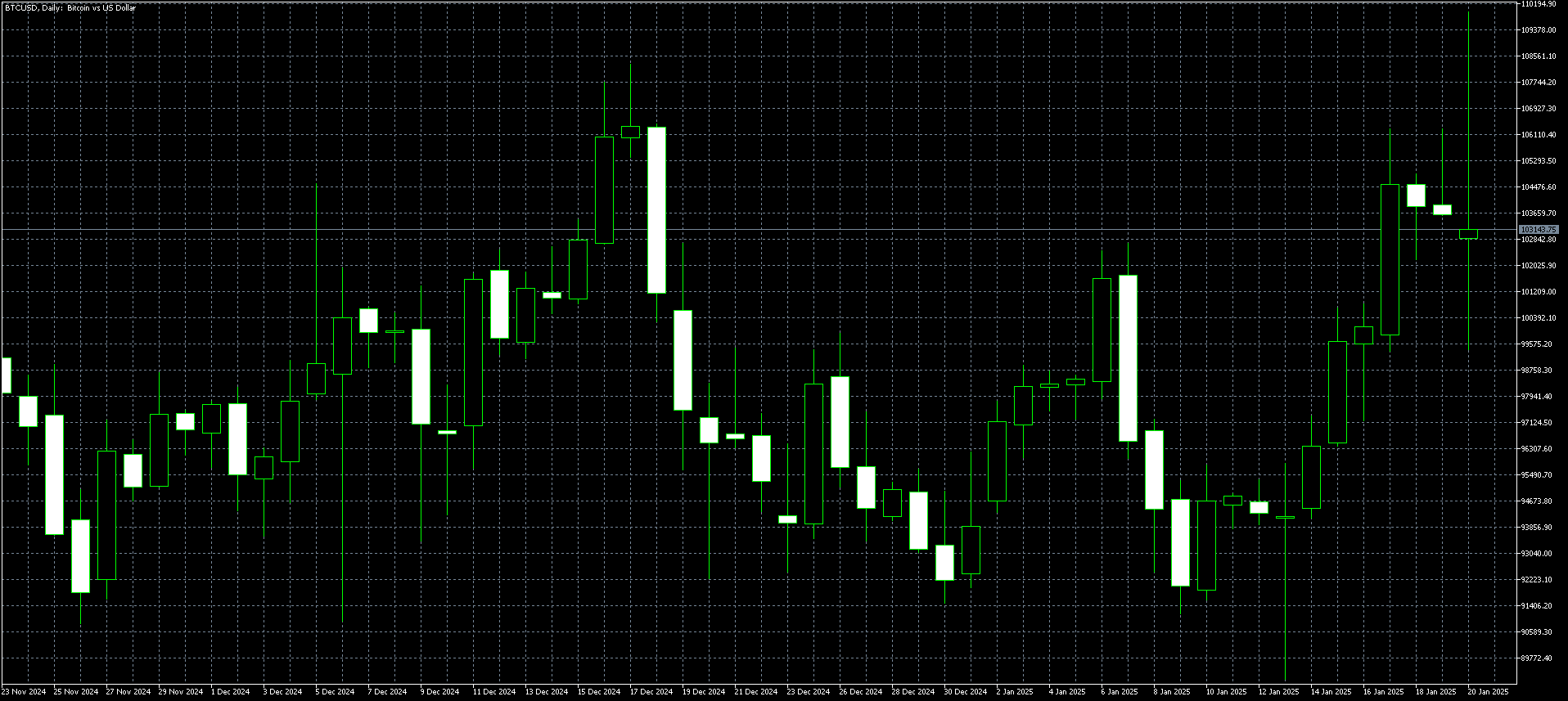

Bitcoin has been trading sideways around the $100,000 mark over the past two months, as the market awaited the start of Trump’s presidency. With Trump now sworn in as president, Bitcoin has begun pushing higher once again. Traders are increasingly optimistic, aiming to drive prices to new highs as Trump has recently reiterated his support for cryptocurrencies.

Upcoming Events to Watch This Week

This week is relatively quiet on the economic front, with the key data releases scheduled for Friday, including U.S. PMI and existing home sales. These reports may provide insight into the health of the U.S. economy but are unlikely to cause significant market volatility. Meanwhile, the Bank of Japan is expected to raise official interest rates from 0.25% to 0.50%, a move that is likely to create substantial volatility in the yen and Nikkei as markets react to this shift in monetary policy.

The market’s primary focus will be on Trump’s initial actions as president. While his expected crackdown on immigration may have limited market impact, any remarks he makes about tariffs could significantly influence sentiment. If his comments hint at a potential trade war, this could raise concerns about global trade and negatively affect market stability. Traders will be closely monitoring his statements for signs of direction on these critical issues.

This Week’s Trump Trades

Here are trade ideas based on this week’s market trends:

USD/JPY: Focus on selling opportunities as the pair appears vulnerable to further downside. Target a break of the key support level at 155.00, which could open the door to additional declines. Monitor Bank of Japan developments closely, as any rate changes could increase volatility.

Bitcoin: The uptrend is gaining momentum, with bullish sentiment returning after Trump’s inauguration. Look for a potential test of $110,000 and higher as traders push for new highs. Buying near key support levels could provide favorable entry points for those with a bullish outlook.

Crude Oil: The recent ceasefire between Israel and Gaza, coupled with Trump’s presidency, is reducing tensions in the Middle East. This geopolitical easing, along with expectations of increased U.S. production, could push crude oil prices lower. Traders should consider selling rallies, targeting lower levels in the short term.

S&P 500: The S&P 500 could push higher this week, buoyed by the start of Trump’s presidency as he enacts his “America First” agenda. Look to buy dips on the S&P 500, as optimism around Trump’s policies may provide continued support for the index.