{kind=link}

- It was a strong week for US stocks and gold, with the S&P rising about 3% by the end of the week.

- Markets are bracing for potential volatility and policy surprises as Donald Trump is inaugurated as US President.

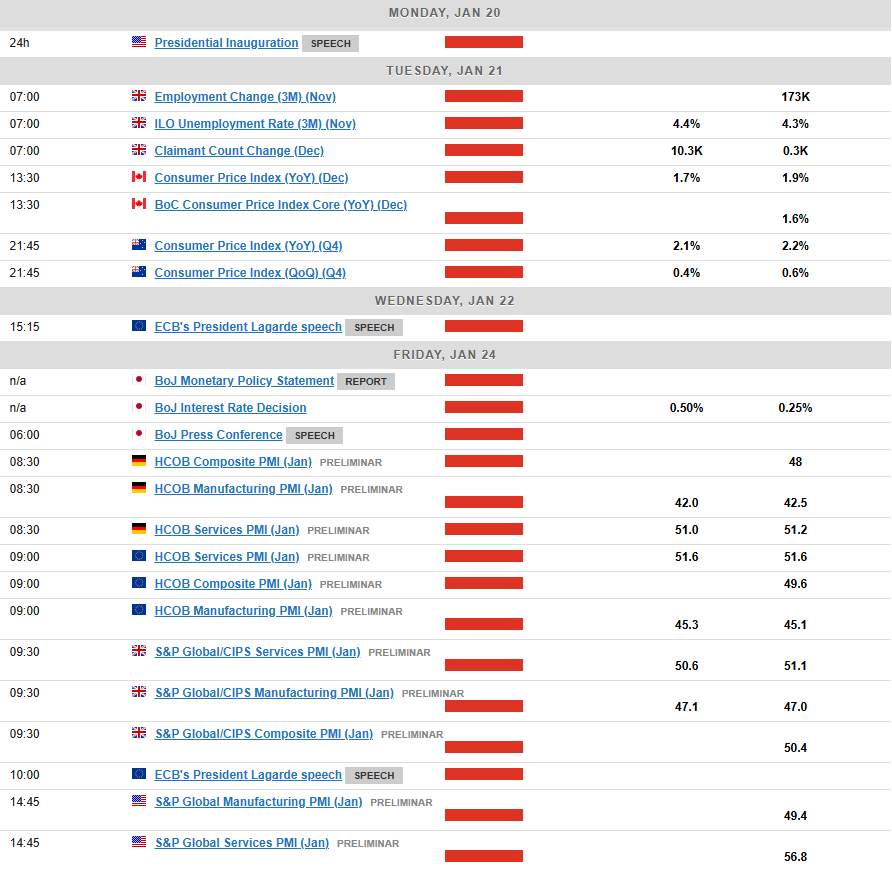

- The Bank of Japan (BoJ) meeting on January 24th is a key event, with potential for an interest rate hike.

- The S&P 500 is showing positive signs, potentially entering a bullish phase if it closes above a key resistance level.

Week in Review: Moderating US Inflation and Strong Earnings Keep Sentiment Positive

Markets bid farewell to the last trading week before Trump 2.0 as incoming US President Donald Trump will be inaugurated on Monday. Markets have been bracing for volatility and potential surprises in policy as Trump returns to the White House.

US inflation data showed positive signs this week and was backed up by some dovish commentary from Federal Reserve policymakers. However, by the end of next week we could all be singing from a different hymn sheet and thus caution remains.

US Equities enjoyed a positive week as strong corporate earnings from the country’s biggest banks helped propel US indices higher. TSMC also provided a positive outlook for 2025 from a demand perspective that boosted hopes around AI spending and growth prospects. At the time of writing the S&P 500 was up 3% for the week.

The S&P 500 banking index (.SPXBK) and regional banks (.KRX) outpaced the main indexes this week, gaining approximately 6.1% and 7.6%, respectively.

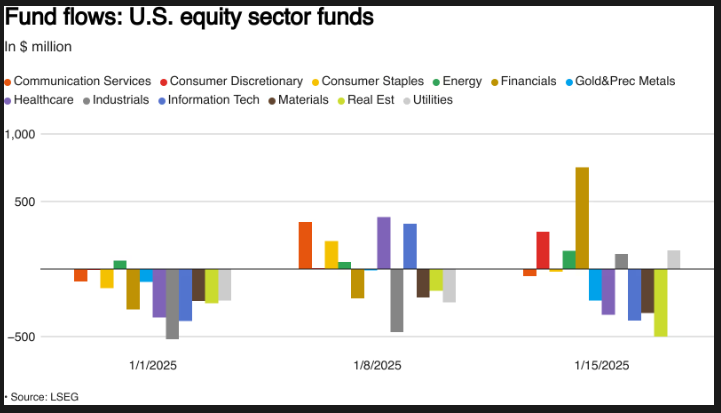

Source: LSEG (click to enlarge)

Gold rose this week and reclaimed the $2700/oz level as the precious metal continues to find demand thanks to global uncertainties. This week the precious metal was also boosted by increased optimism around US rate cuts for 2025.

Oil prices continue to hold the high ground thanks to new Russian sanctions as well potential sanctions on Iran when President Trump assumes office. Oil prices have added 1.87% this week following the successive week of gains. If President Trump reverses the no drilling mandate passed by President Biden recently that could lead to a drop in prices.

On the FX front, the US Dollar has struggled this week but it hasn’t been a smooth move lower. Markets still see a stronger USD in 2025 and that could in part explain the grind lower and why it didn’t gather any real steam.

The crypto market is back on the up this week with Bitcoin eyeing a move above the 105k handle at the time of writing. XRP has continued its rise as markets also bet on a pro crypto policy under President Trump’s administration.

All asset classes and Global markets await the inauguration of Donald Trump as they wait with bated breath for his long promised policy proposals, The proposals are likely to shape market dynamics in the months ahead and remain crucial.

The Week Ahead: Trump Inauguration and BoJ Hold the Keys

Asia Pacific Markets

The main focus this week in the Asia Pacific region is the Bank of Japan’s meeting on January 24. Recent inflation and wage figures look promising and back its plan to increase interest rates at next week’s meeting.

Earlier today we heard rumors from Nikkei that the majority of BoJ board members are set to approve a rate hike next week.

After Friday’s release of data, which saw Chinese GDP come in better than expected. The economy grew by 5.4% in the fourth quarter compared to a year ago, up from 4.6% in the third quarter and higher than the 5.0% estimate. This was the fastest growth since the second quarter of 2023.

Following a data heavy week China’s schedule for new updates slows down. On Monday, the loan prime rates will be announced, but no changes are expected since the People’s Bank of China left key rates the same. Attention will turn to Trump’s inauguration and whether he will announce any immediate tariffs on China.

In the Asia Pacific region New Zealand inflation will be the highest impact data release and could provide the NZD with some impetus moving forward.

Europe + UK + US

In developed markets, the US inauguration will no doubt be at the forefront as well as any immediate moves by the incoming administration. This has the potential to overshadow any data releases.

The US will also be releasing S&P Manufacturing and Services PMI data on Friday.

In Europe and the UK, we also have a S&P manufacturing data which would give further insights into the Euro Area economy. There are also two speeches from ECB President Christine Lagarde on Wednesday and Friday.

Chart of the Week

This week’s focus is on the S&P 500 as it looks to record a daily candle close above a key level that would put bulls firmly in control.

The S&P 500 is currently trading above the previous swing high at 5980 with a daily candle close above leading to change in structure.

This would be key as the optimism for stocks under the incoming President remains high. The S&P found support at the back end of the week after breaking above the 20-day SMA after strong bank earnings helped the index move higher.

There is more earnings due next week with further strong performances from the likes of Netflix likely to propel the S&P 500 toward its all time highs .

Immediate resistance rests at 6025 before the all time highs of 6094 comes into focus.

On the downside, support rests at the 20-day SMA which lines up with support at 5910 before 5840 and 5757 become areas to focus on.

S&P 500 Daily Chart – January 17, 2025

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 5910

- 5840

- 5757

Resistance

- 6025

- 6094

- 6170