{kind=link}

- Markets brace for impact ahead of Trump’s inauguration.

- BoJ seen raising rates at first gathering of 2025.

- Euro and Pound traders turn gaze to PMIs.

- Canada and New Zealand CPI data to shape BoC and RBNZ bets.

- World Economic Forum in Davos also in focus.

Trump takes the oath of office

Another interesting week lies ahead of us, with the spotlight falling on the inauguration of US president-elect Donald Trump on Monday, and on the BoJ, which is kickstarting the first round of central bank decisions for 2025 on Friday.

Getting the ball rolling with Trump and the US, the dollar has benefited and Treasury yields have surged lately on increasing expectations that the Fed may need to proceed with extra caution on rate cuts this year. Trump’s tariff pledges and his promises of corporate tax cuts and deregulation have raised concerns about a resurgence of inflation, which has been proving sticky even before such policies are enacted. What’s more, the US economy seems to be firing on all cylinders, with the labor market seeing strong growth in November and December, corroborating the notion that there is no need for the Fed to rush into lowering interest rates further.

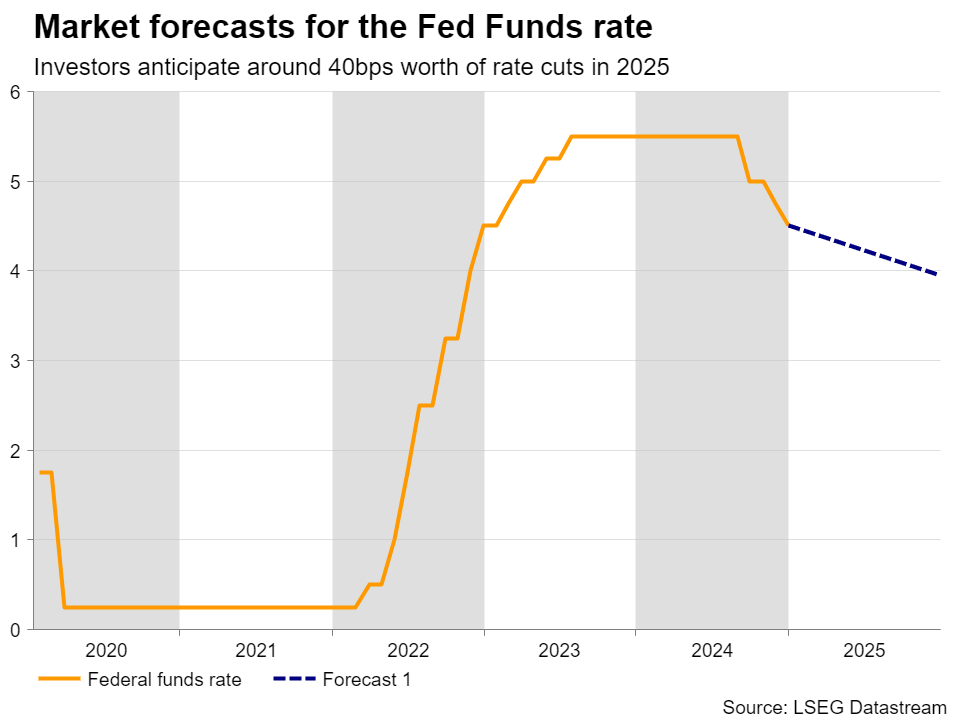

According to Fed funds futures, investors are currently expecting 40bps worth of reductions by December 2025, which is a more hawkish projection than the Fed’s own upwardly revised ‘dot plot’, which pointed to two 25bps reductions. And this is even after news headlines suggested that the new US administration is likely to adopt a gradual approach on tariffs and after the US CPI numbers for December came in somewhat softer-than-expected.

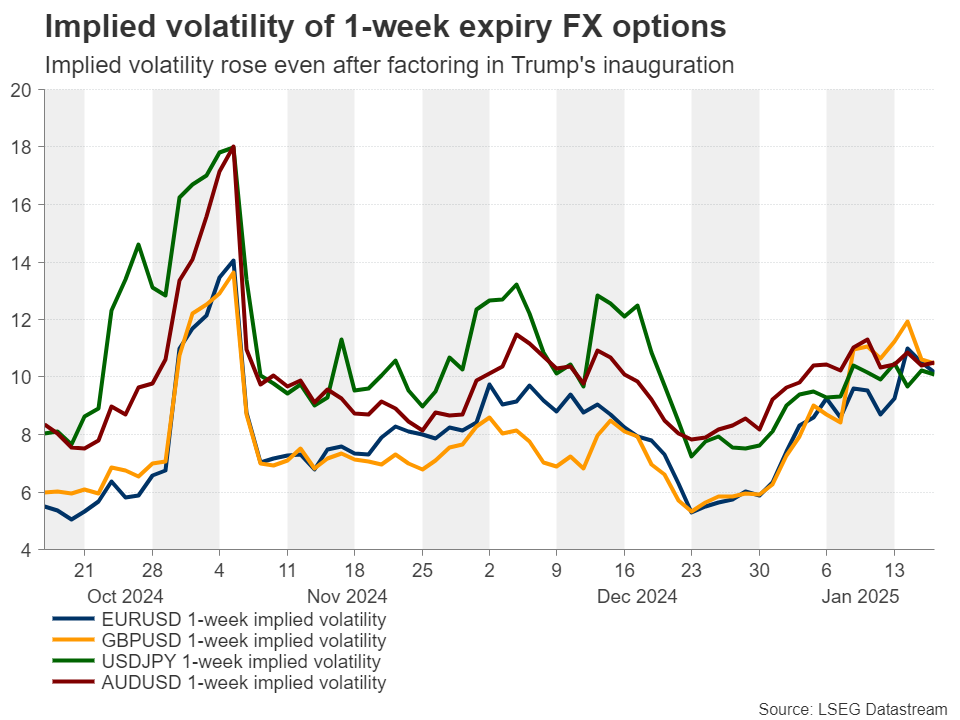

With all that in mind, investors may be eagerly awaiting Trump’s inauguration speech for more clues about how he plans to proceed with his policies, and this is evident by the fact that the implied volatility of 1-week expiry FX options has been trending north and has continued to rise even after factoring in Monday’s inauguration. In other words, market participants see the event as a source of volatility for the FX market.

Should Trump sound more hawkish on tariffs than the latest headlines suggest, the dollar is likely to take another shot in the arm as Treasury yields rebound. A potentially risk-averse mood could also weigh on equities, specifically stock futures, as the New York Stock Exchange will remain closed in celebration of Martin Luther King Day. However, whether any declines will be sustained will also depend on whether Trump will bolster the hype about extending corporate tax cuts, which is a supportive variable.

Stock traders will have more to digest the following day as Netflix will report its earnings results for the last quarter of 2024.

Will the BoJ hike rates right off the bat?

Flying to Japan, the BoJ will kickstart the first round of central bank decisions for 2025 on Friday. At its last meeting for 2024, the BoJ decided to refrain from hiking interest rates, with Governor Ueda saying that they need more information to raise interest rates again, placing emphasis on wages and the uncertainty surrounding US president-elect Trump’s economic policies.

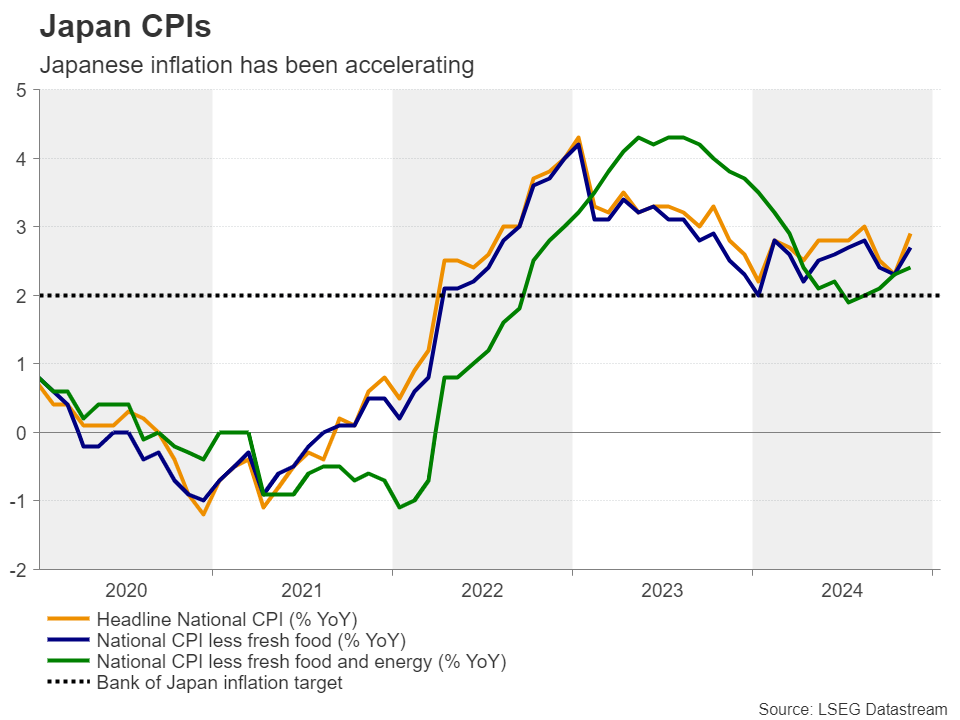

Since then, data revealed that the Nationwide CPI accelerated notably in November, while the closely watched Tokyo prints pointed to even hotter price pressures in December. Wages also sped up in November. What’s more, the Summary of Opinions from the December gathering suggested that a hike may be on the cards sooner than investors were led to believe following Ueda’s press conference.

Combined with hawkish remarks by several policymakers thereafter, including Ueda this week, who said that he heard many encouraging views on potential pay hikes since the turn of the year, the aforementioned developments prompted investors to pencil in around an 80% chance of a quarter-point interest rate increase on Friday.

Having said that though, the BoJ has a strong record of disappointing hawkish bets, and this may be another one of those occasions if president-elect Trump sounds too aggressive about his tariff plans at his inauguration speech on Monday. Therefore, if the Bank refrains from hitting the hike button once again, the yen is likely to tumble.

The opposite could be true should policymakers agree to hike, but the risks may be asymmetrical. The negative impact on the yen if the Bank were to stay on hold may be larger than the positive impact associated with a hike. Nonetheless, a falling yen may not be the easiest trade in town as further declines may encourage a new round of intervention by Japanese authorities.

January PMIs the drivers for Euro and Pound

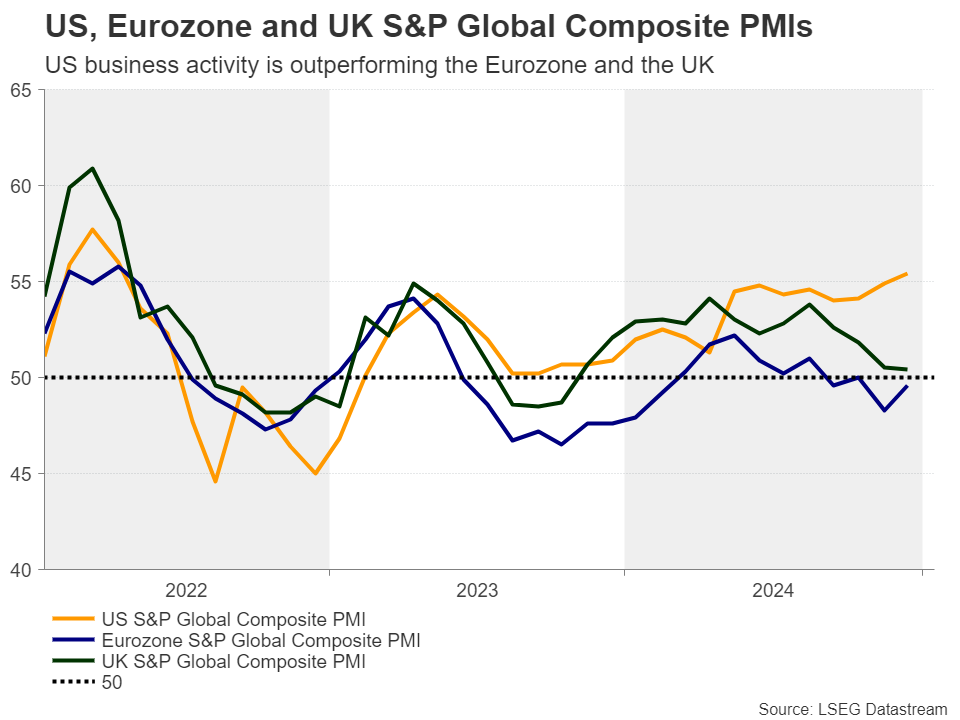

From the Eurozone and the UK, the preliminary S&P Global PMIs for January are coming out on Friday. The euro and the pound have been bleeding recently, with the former falling victim to the widening divergence in monetary policy expectations between the ECB and the Fed and the latter feeling the heat of fears about a Truss 2.0 episode as well as the latest round of weak UK data. Just this week, the softer-than-expected inflation data for December was followed by weak GDP, December retail sales, and industrial production numbers for November.

Both the ECB and the BoE are expected to cut interest rates more aggressively than the Fed this year, with the former seen cutting another 95bps and the latter another 60bps. Thus, PMIs pointing to more troubles for the Eurozone and UK economies could further widen the policy divergence between the ECB and the BoE with the Fed and thereby deepen the wounds of the euro and the pound.

The US S&P Global PMIs will also be released on the same day, but dollar traders will be already digesting Trump’s policy signals and thus, the impact of those numbers may be limited and short-lived.

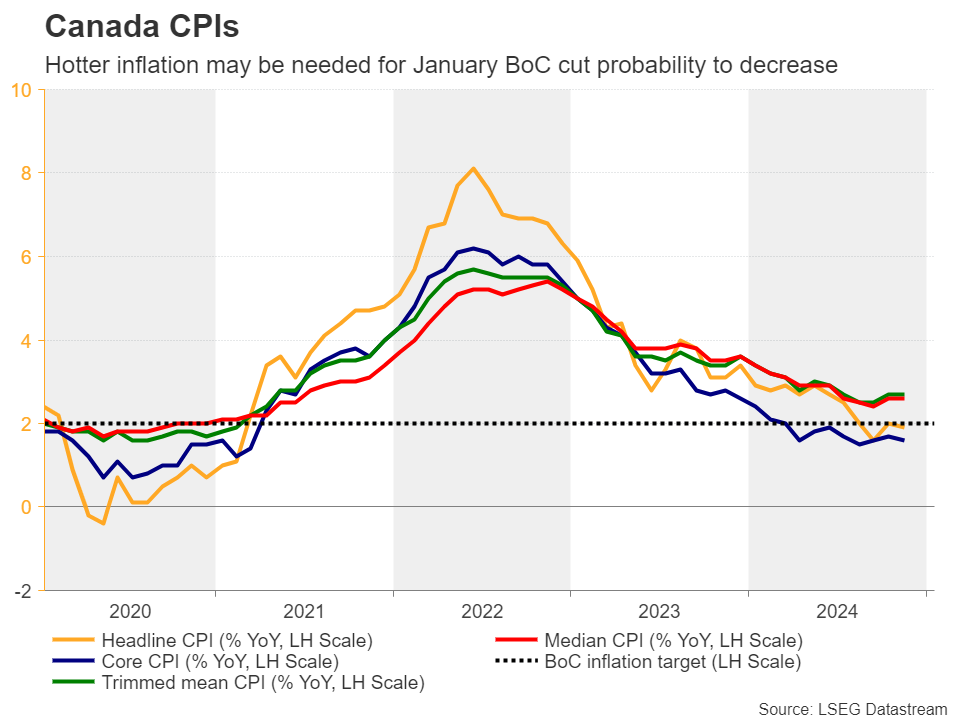

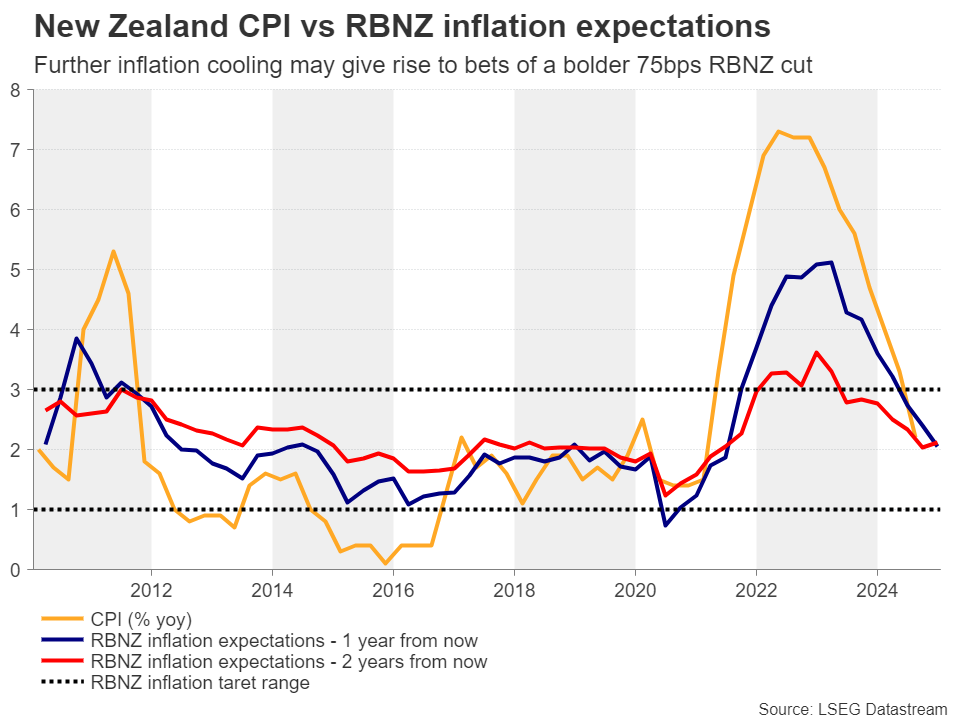

Loonie and Kiwi traders await CPI reports

Following this week’s US CPI figures, Canada and New Zealand are scheduled to release their own inflation prints on Tuesday. The Canadian jobs report for December revealed strong employment gains, with the unemployment rate unexpectedly dropping. Still, investors are assigning a decent 65% for the BoC to cut interest rates by another 25bps on January 29. For that probability to be lowered meaningfully, Canada’s CPI numbers may need to come in hotter-than-expected, which could encourage loonie traders to increase their long positions. A positive business outlook survey by the BoC on Monday may also help.

In New Zealand, a February rate cut seems to be a done deal. The question is whether it will be a quarter- or a half-point cut. At their November gathering, RBNZ policymakers cut the cash rate by 50bps and signaled that if economic conditions continue to evolve as projected, they could lower the OCR further early in 2025.

Since then, GDP data revealed that the economy slipped into technical recession in Q3, allowing investors to assign a strong 65% chance that another bold 50bps reduction may be looming, especially as inflation rested at 2.2% y/y in Q3, very close to the midpoint of the Bank’s 1-3% target range.

Ergo, should next week’s data reveal that inflation returned, or even fell below that 2% midpoint, market participants may start considering a larger 75bps reduction, and the kiwi could resume its prevailing steep downtrend against its US counterpart.

Global leaders gather in Davos

Elsewhere, the World Economic Forum in Davos, Switzerland will take place. The meeting gets underway the same day with Trump’s inauguration and thus, Trump is expected to deliver a speech virtually on Thursday. Other speakers include Ukrainian President Zelenskyy, who will attend in person and speak on Tuesday.

Geopolitical tensions will be one of the main topics at the gathering, and thus, it will be interesting to see what risks global leaders foresee for their economies this year. Their views on Trump’s agenda may be closely monitored as well, while artificial intelligence will also be a key topic of discussion.