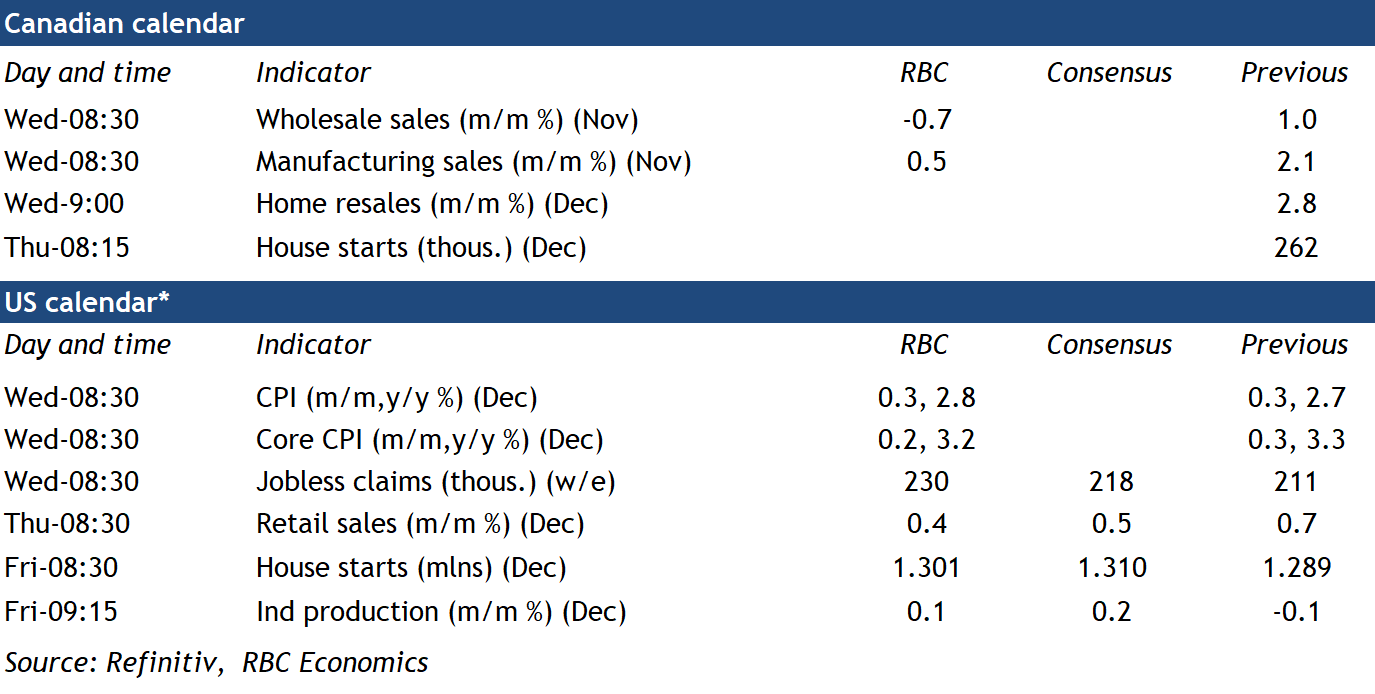

{kind=link}

December’s U.S. consumer price index release on Wednesday will be the last major data print before the first U.S. Federal Reserve meeting of 2025, and we expect it to show further moderation in price pressures after some acceleration in September and October, but not by enough for an interest rate cut this month.

Headline CPI growth is expected to have ticked higher in December to 2.8% from 2.7% in November as a smaller decline in gasoline prices push energy prices back closer in line with year-ago levels following four straight year-over-year declines. We expect food inflation to hold at 2.4%, while the core price growth for everything outside of energy and food edges down to 3.2% from 3.3%.

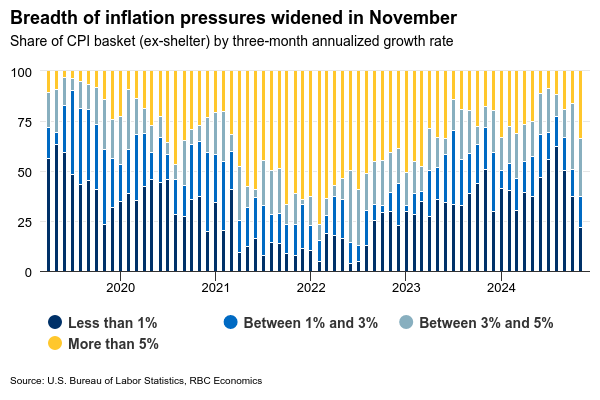

The expected tick lower in core price growth is a result of a lower 0.2% month-over-month increase, driven by slowing rent price growth alongside easing in other core services. The scope of price pressures across the consumer basket has widened in recent months. Our diffusion index showed a third of the basket outside of shelter saw inflation up 5% or more on a three-month annualized basis in November—up from less than a tenth earlier in the summer. We’ll watch this measure closely on Wednesday for any improvements in December.

Lower core price growth in December will not be enough to cancel out recent upside surprises in economic data for the Fed, including the U.S. jobs report on Friday that showed strong hiring gains and solid labour market conditions at the end of 2024. In the December meeting, the Fed had already scaled back their easing bias after a 25 basis point rate cut with Chair Jerome Powell saying the central bank is “at or near a point at which it will be appropriate to slow the pace of further adjustments.”

We now expect the Fed will forego an interest rate cut on Jan. 29th and hold the Fed funds rate unchanged at 4.25%-4.5% throughout 2025.

Week ahead data watch

A 0.5% increase in Statistics Canada’s advance estimate of November manufacturing sales looks to have largely reflected an increase in prices – the increase coupled with reported industrial output prices suggest sale volumes declined after jumping 1.4% in October.

December Canadian home resales likely showed mixed results across regions given early market reports – sales showed strength in Montreal but pulled back in Toronto to reverse earlier fall/winter increases.

Higher auto sales and an increase in gasoline prices are expected to support a 0.4% increase in U.S. retail sales as U.S. consumer spending remains resilient.