{kind=link}

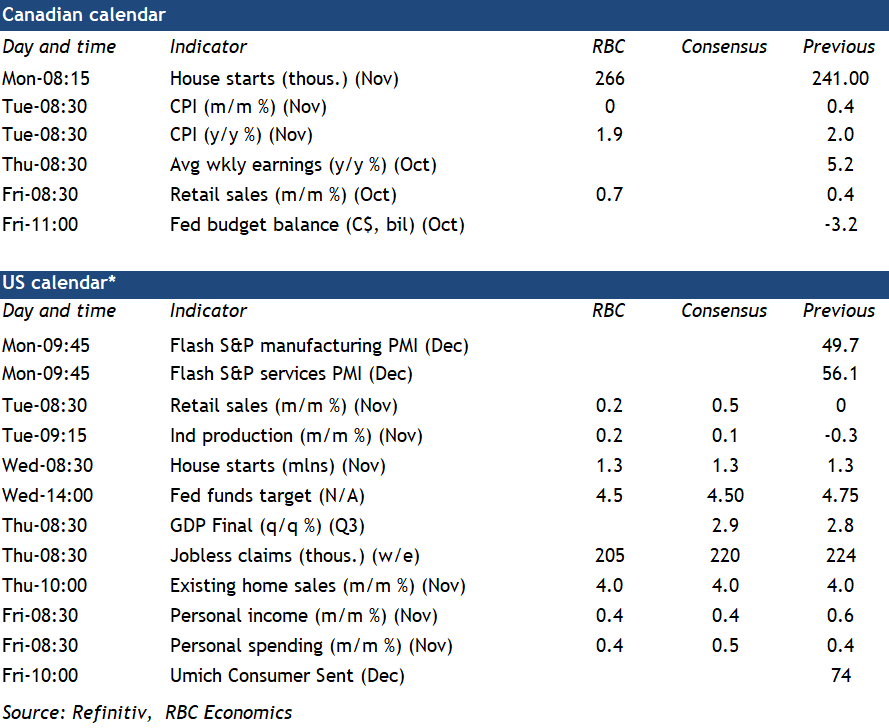

Canadian consumer price index growth is expected to have eased slightly in November after picking up in October, which is consistent with a persistently softening economy that’s left broader inflation pressures tracking at or below the Bank of Canada’s 2% target.

We expect headline inflation to have eased to 1.9% in November. Price growth in both food and energy inflation are expected to have held largely steady year-over-year at around 3% and -2.7%, respectively. But, we look for growth excluding those components to drop to 2.1% from 2.3% in October.

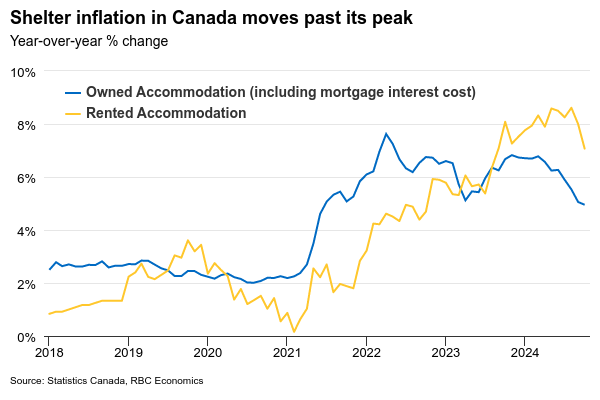

Shelter inflation still accounts for a disproportionate share of overall inflation, but should show further signs of slowing in November. Mortgage interest costs were still up almost 15% from a year ago in October, and accounted for over a quarter of annual consumer price growth. But, that is down from a 30% growth peak in 2023 and will continue to slow following interest rate cuts. Rent inflation also likely eased as a drop in current market asking rents flow through to lease renewals.

Annual growth in the BoC’s preferred “core” measures, such as CPI trim and median, are both expected to tick lower following a rise in October, averaging 2.5%. The breadth of inflation pressures remained relatively narrow in October even with readings picking up. That likely persisted in November.

Unlike Canada where inflation pressures have eased, a resilient U.S. economy has meant inflation has been stickier than previously expected. Headline U.S. inflation picked up slightly to 2.7% in November, while the U.S. Federal Reserve’s “supercore” measure held at an elevated 4.3% on a three-month annualized basis.

Those trends will be closely watched by the Fed, but shouldn’t prevent another interest rate cut on Wednesday. Chair Jerome Powell hinted in recent communications that the central bank doesn’t need to rush rate cuts, but labour markets have also been gradually softening and inflation is still lower than it was at the start of this year. The level of the Fed funds rate is still likely higher than it needs to be for inflation to continue to edge broadly toward the Fed’s 2% objective.

We continue to think the Fed will cut by 25 basis points in December and January before hitting a pause with the fed funds rate at a restrictive 4%-4.25% range. As we have highlighted before, a solid domestic demand backdrop, in no small part tied to a large government budget deficit, would need to be offset by tighter monetary policy.

Week ahead data watch

- We expect Canadian housing starts to grow by 10% in November, reaching 266K.

- October SEPH data will be watched closely for further signs of softening in the labour market. Given slower hiring demand, we expect job openings to weaken further and wage growth to slow.

- Canadian retail sales likely increased by 0.7% in October, in line with StatsCan’s preliminary estimate. Auto sales were up 1.7%, down from the 4.7% in September. Sales at gas station rebounded in October as prices rose.

- We expect U.S. retail sales to tick up again (+0.2%) in November, slowing from the 0.4% growth in October. Auto and gas station sales were both higher during that month.

- U.S. personal spending likely grew by 0.4% in November, matching the pace in October. We expect personal income to edge up by the same amount (+0.4%) as wage growth remained robust in the U.S.

- U.S. industrial production likely ticked higher in November, by 0.2%, supported growth in auto manufacturing.