{kind=link}

- Commodity currencies came under pressure towards the end of 2024

- Bets of a Fed pause at the turn of the year turbo-charge the dollar

- Tariff fears and frustration about China’s policies also main drivers

- Monetary policy could prove decisive in the battle among them

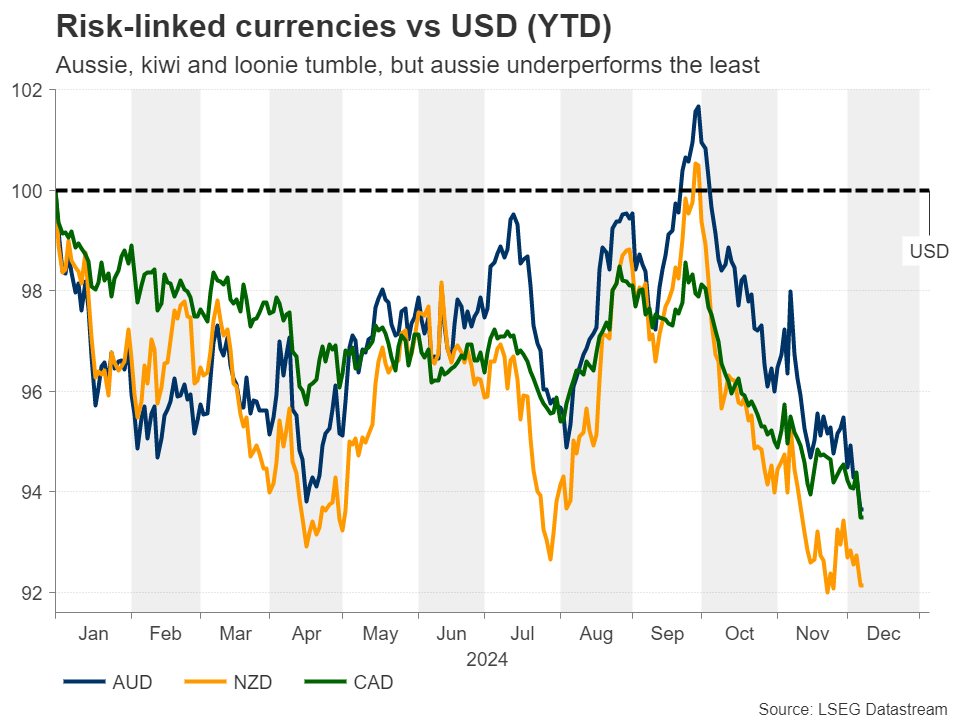

Aussie, kiwi, loonie surrender to stronger US dollar

As 2024 approaches the finish line, the risk-linked currencies – the Australian dollar, the New Zealand dollar, and the Canadian dollar – also known as the commodity currencies, have been seen weakening notably, despite Wall Street conquering fresh record highs.

Although the Australian and New Zealand dollars outperformed their US counterpart in terms of year-to-date performance at some point in late September, October proved to be a dark month due to upbeat US data lessening the need for aggressive easing by the Fed, and due to investors remaining unsatisfied by the massive liquidity injections of the People’s Bank of China to shore up economic activity.

Fed and tariffs the biggest drivers

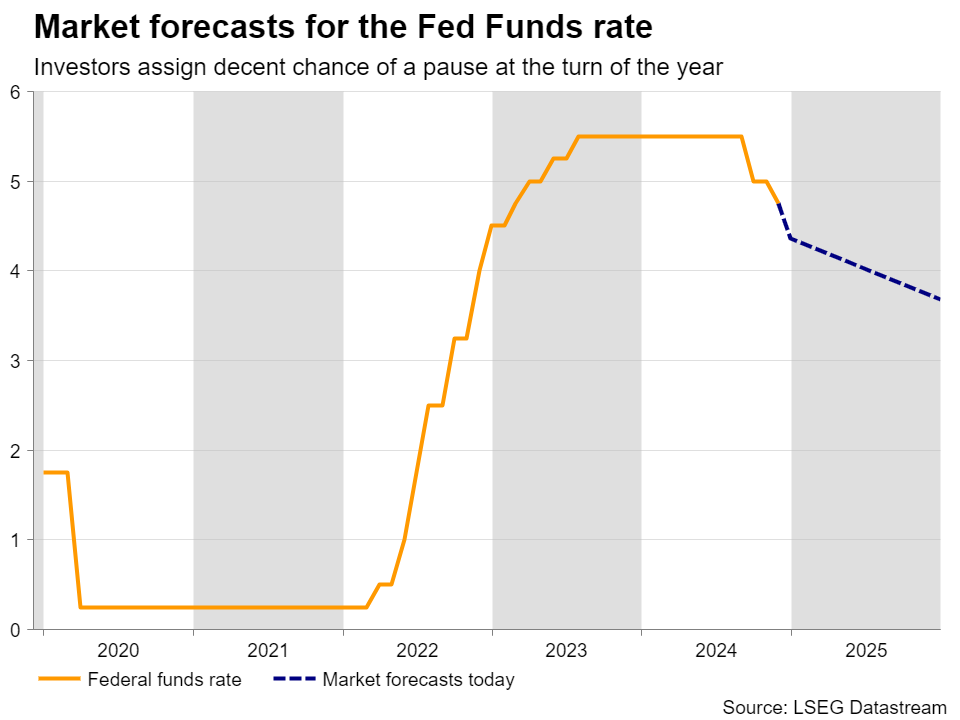

Alongside the already wounded loonie, all three currencies accelerated their slides after Republican candidate Donald Trump won the US election. Trump’s policies are seen as fueling inflation and thereby forcing the Fed to proceed even slower with easing, and even skip some rate cuts at its upcoming meetings. With several Fed officials, including Fed Chair Powell, noting recently that they are in no rush to further lower borrowing costs, investors are now assigning a strong chance for the Committee to take the sidelines as soon as at the first meeting of 2025, in January.

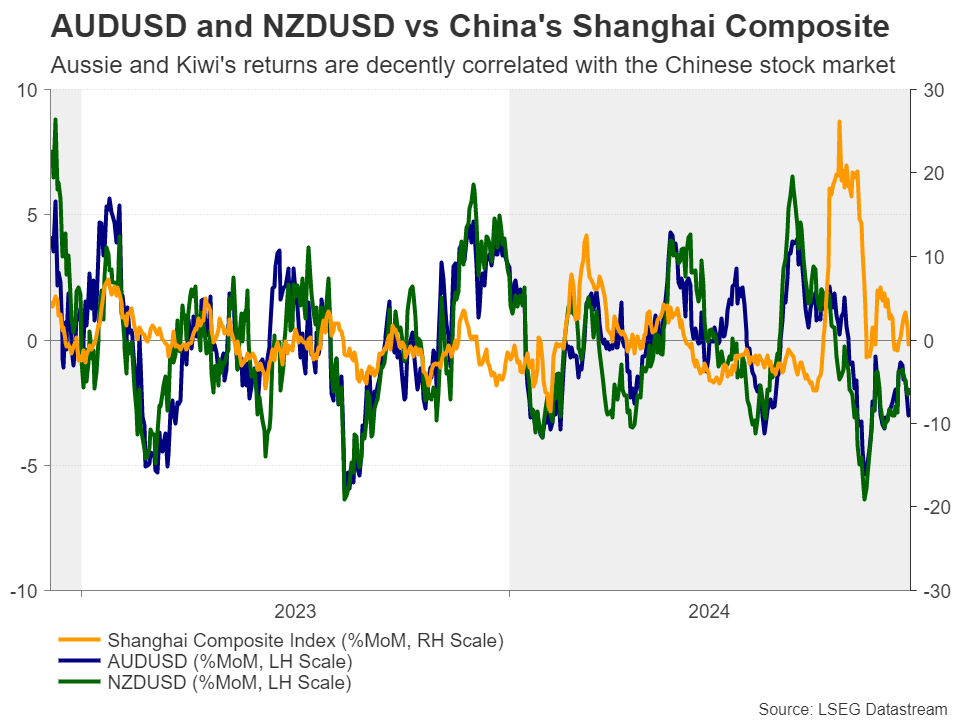

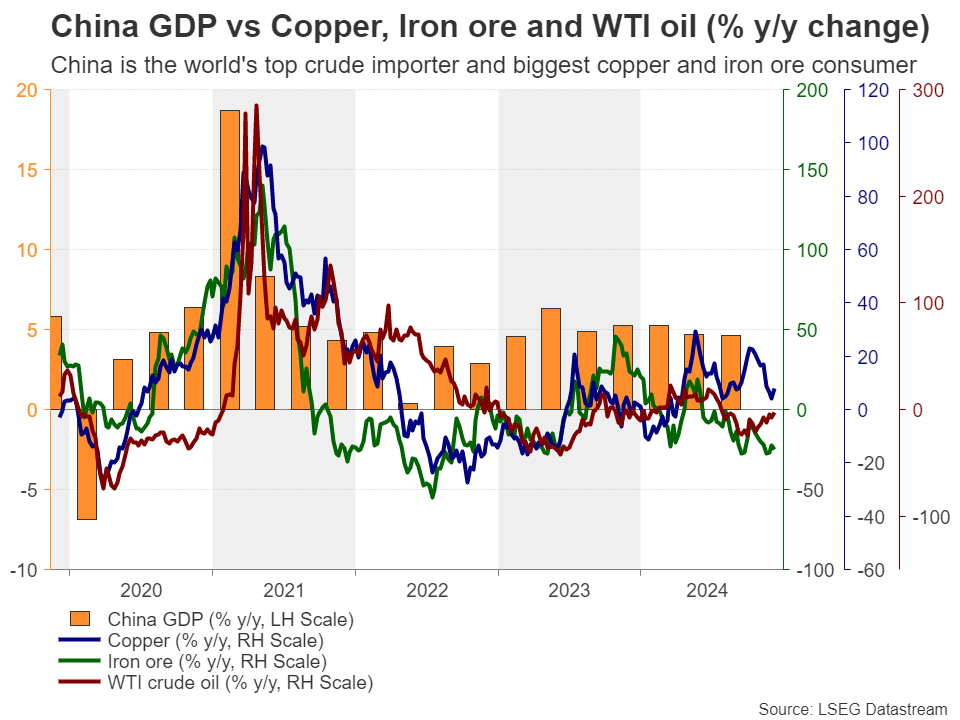

Having said that, Trump’s victory is not hurting the commodity-linked currencies only through the Fed-policy channel. His promises about massive tariffs on Chinese goods are translating into fears about a second trade war and deeper economic wounds for the biggest trading partner of Australia and New Zealand. Those fears could also result in lower commodity prices, as the world’s second largest economy is also the world’s top crude oil importer and the biggest copper and iron ore consumer. Trump has also threatened Canada and Mexico, as well as the BRICS countries, while there is nervousness about how he will proceed with Europe.

Thus, the outlook for the commodity currencies remains blurry, at least for the first half of the year, especially if US data continue to support the idea that the Fed may need to proceed with more rate-cut breaks down the road.

What about monetary policy?

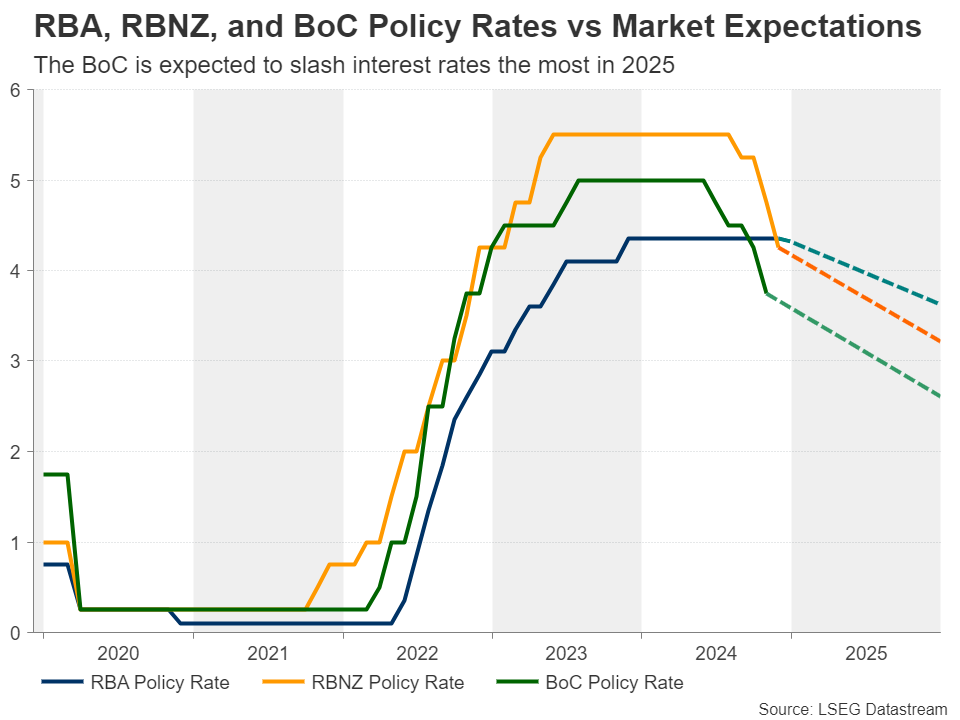

But what happens if we remove the US dollar from the equation? Which of these three risk-linked currencies will perform best and which worst? The answer may lie down to the divergence in monetary policy strategies and expectations of the RBA, the RBNZ and the BoC.

Among the three central banks, the only one that hasn’t hit the rate cut button yet is the RBA, with market participants projecting its first 25bps reduction in April and almost another two by the end of 2025. This is largely due to underlying inflation remaining elevated. The Bank itself has pointed out that as measured by the trimmed mean, core inflation remains some way from the 2.5% midpoint of their inflation target range.

Both the BoC and the RBNZ reduced interest rates by equal amounts until now, but the one expected to continue cutting slightly more aggressively moving forward is the BoC.

The battle between the three

Thus, entering 2025, the aussie may continue to be the best performer among the three, while the loonie could be the laggard. But this could change once the RBA begins its own rate-cut cycle, as very dovish rate paths by the BoC and the RBNZ are already discounted and data coming out of Canada and New Zealand may not be bad enough to warrant so many basis points worth of reductions in 2025. Therefore, the aussie could run out of fuel at some point and take the last place.

As for the best performer during the second half of the year, it may be the Canadian dollar. Yes, the loonie suffered more on Trump’s first remarks about tariffs, but let’s not forget that he has pledged to proceed with a more aggressive policy against China, something that could weigh more on the aussie and kiwi.