{kind=link}

- Dollar elevated even as Fed leaning towards December cut

- Investors still see strong chance for a January pause

- Strong jobs numbers could add fuel to dollar’s engines

- The data comes out on Friday at 13:30 GMT

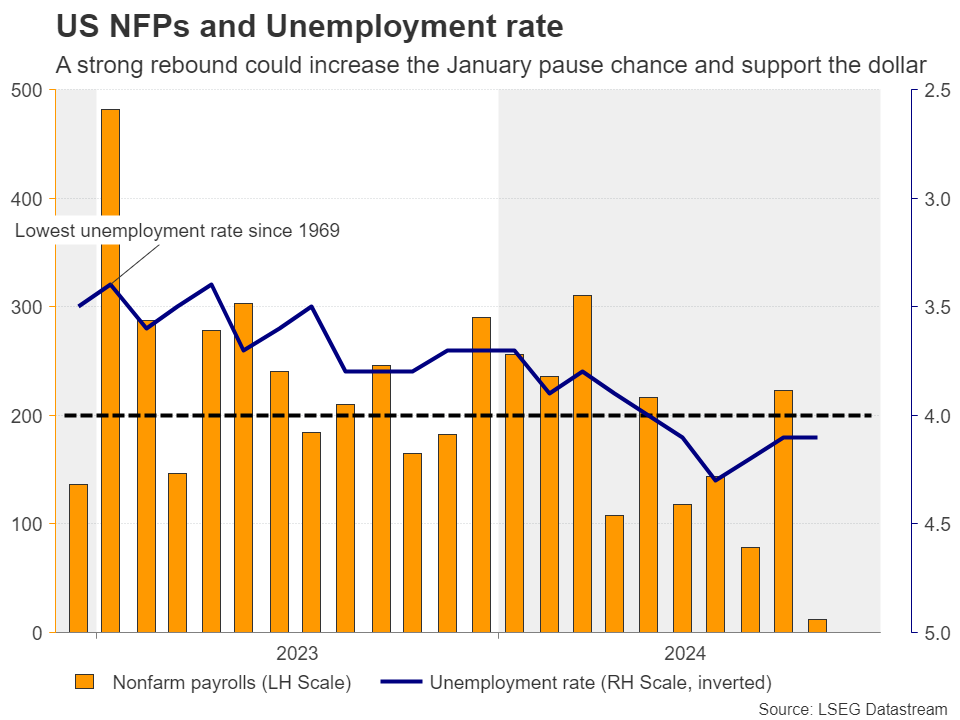

Investors are still expecting a Fed pause in January

The US dollar recharged this week, confirming the notion that last week’s pullback may have been the result of traders realizing some profits on their long positions ahead of the Thanksgiving break.

Although some Fed officials appeared to be favoring another rate cut in December, market participants continued to believe that the Fed may need to take the sidelines at the turn of the year, assigning a stronger chance of that happening in January. According to Fed funds futures, there is a 60% chance for a pause at the first FOMC gathering of 2025.

After threatening Canada, Mexico and China with hefty tariffs, US President-elect Donald Trump warned that he will impose 100% tariffs on BRICS nations if they were to move away from the dollar and create their own currency. Trump’s tariff pledges and his promises for massive corporate tax cuts are seen as inflationary policies, which alongside the better-than-expected data out of the US have allowed investors to continue speculating on a slow rate-cut process by the Fed. And that is the case even though several policymakers, including the usual hawk Neel Kashkari, are inclined to push the cut button in December.

Jobs growth seen rebounding strongly

This week, Friday’s employment data may attract special attention, especially following the very weak 12k jobs gain in October. Although the low print was attributed to labor strikes and hurricanes, a strong rebound may be needed for investors to remain confident on the dollar uptrend.

The forecasts suggest that the economy has gained 202k jobs in November, but the unemployment rate is expected to have increased to 4.2% from 4.1%. Nonetheless, that’s not necessarily a bad thing if it is accompanied by a rising participation rate, as it could be a sign of more unemployed people entering the labor force and being encouraged to actively start looking for a job. Average hourly earnings are expected to have slowed but only fractionally, to 3.9% y/y from 4.0%, which means that inflation could remain somewhat sticky in the months to come.

Such numbers are likely to encourage investors to add to their bets about a potential pause at the turn of the year, and even increase the probability of the Fed remaining sidelined at both the December and January gatherings. That probability currently rests at a respectful 23%.

Euro/dollar may be poised to drift further south

With the euro feeling the heat of the uncertainty surrounding French politics, euro/dollar may be vulnerable to drift further south if the US data add more fuel to the dollar’s engines.

The bears may feel confident to take the action down to the low of November 22 at 1.0330, or towards the 1.0290 barrier, marked by the low of November 21, 2022. If they are not willing to stop there, a break lower could carry larger bearish implications, paving the way towards the inside swing high of November 11, 2022, at around 1.0100.

For the outlook to start looking brighter, a rebound above the key pivot area of 1.0665 may be needed. Such a move could encourage advances towards the 1.0765 zone, marked by the inside swing lows of October 23 and 29, the break of which could trigger extensions towards the high of November 7 at 1.0825.