{kind=link}

- US dollar set for bullish start to new year as Fed rate cut bets pared

- Yen bears make a comeback, but will they reign in 2025?

- Fed and BoJ policy expectations diverge after Trump’s re-election

‘Trump trade’ reinforces dollar bulls

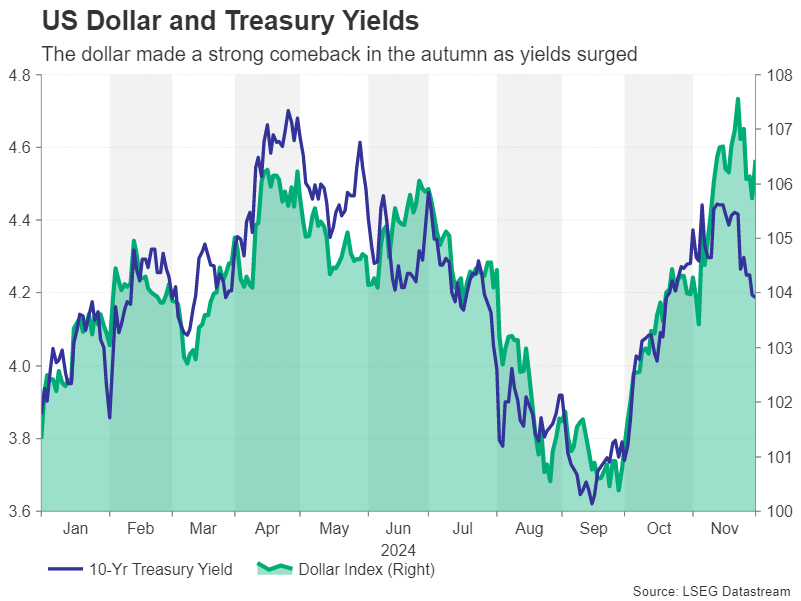

The Federal Reserve finally cut interest rates in September, but far from falling, the US dollar embarked on a fresh rally as policymakers dashed hopes of aggressive policy easing. As we head into 2025, there can be no denying about the dollar’s superiority. The greenback is not only being supported by a resilient US economy and persistent price pressures, but also by expectations that the incoming Trump administration will enact polices that will further boost growth and inflation.

Donald Trump’s historic victory in the 2024 presidential election is shaping up to be the defining narrative for financial markets in 2025. But as the dollar and assets such as US equities and cryptocurrencies cheer the prospect of a Republican-controlled Congress, Trump’s return to the White house isn’t being celebrated by everyone.

Leaving aside the risk to countries that will probably be at the receiving end of Trump’s trade tirade, his election pledges, which are deemed to be inflationary, could cause a major headache for the Fed. Expectations that big tax cuts and tariff hikes will fuel inflation have already pushed Treasury yields to multi-month highs, powering the dollar’s rally.

How inflationary will Trump’s policies be?

The question for the 2025 outlook is how quickly the Republicans will be able to push through their tax agenda and how readily will Trump resort to imposing higher tariffs as he begins trade negotiations with America’s major trading partners like the European Union, Mexico and China?

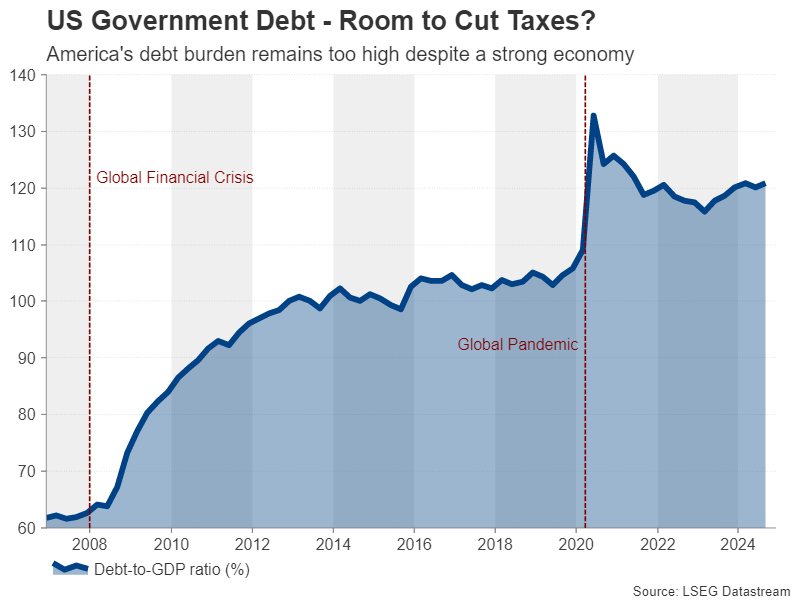

But it’s not just about the timing. With a budget deficit running at more than 6% of GDP and a ballooning national debt, the Republicans could slash spending to pay for their tax giveaways, offsetting some of the boost to the economy from lower taxes.

When it comes to tariffs, it’s yet unclear how far the new Trump administration will go in slapping higher levies on imports, particularly on Chinese goods, which could be in excess of 60%. Trump has a tendency of using scaremongering as a negotiating tactic.

Hence, for the dollar, it’s all about how much has already been priced in and how much that’s yet to be factored in by investors. Any signs that Trump’s election promises will be watered down are likely to be negative for the US dollar during 2025. Similarly, should there be any delays by the newly elected lawmakers in preparing and agreeing to Trump’s legislative agenda, a dollar pullback is a strong possibility.

However, if the Republicans move swiftly with tax cuts and Trump shows his unwillingness to compromise on trade, the dollar will be well positioned to climb towards its 2022 highs when the Fed was hiking rates aggressively.

The Fed’s inflation dilemma

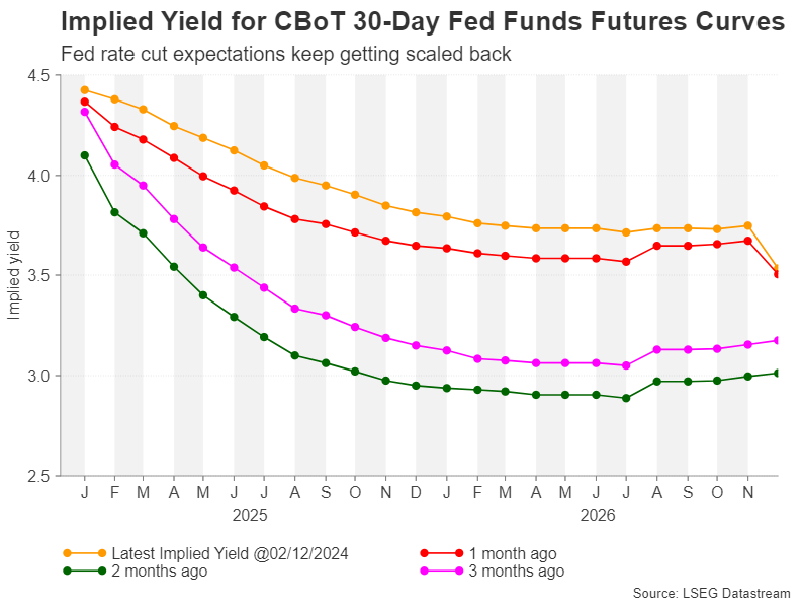

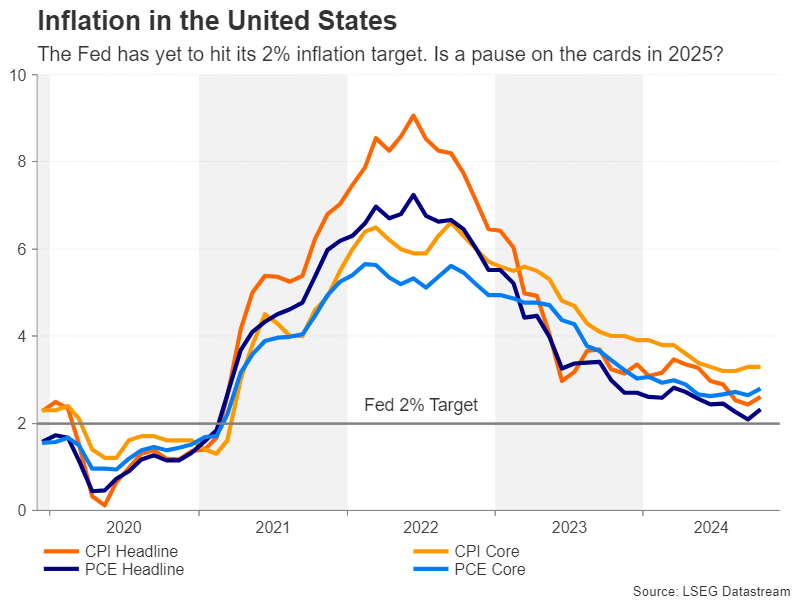

Although the Fed’s tightening days are over and borrowing costs are now falling, the inflation battle is not won and policymakers are wary about lowering rates too quickly. The Fed’s unexpectedly hawkish stance is underscoring the greenback’s bullish outlook. The main concern is that inflation appears to be settling closer to 2.5% instead of the Fed’s 2.0% target.

If this is the case even before Trump has taken office, there’s a real risk that the Fed will not be able to deliver many rate cuts in 2025, while a rate hike cannot be completely ruled out.

Geopolitical risks

Away from domestic politics and Fed policy, the risks to inflation are somewhat tilted to the upside. Assuming there is no nuclear fallout in the meantime, a Trump presidency will probably push for a ceasefire agreement between Ukraine and Russia. However, Trump is likely to take a more hard-line stance against Iran. This risks triggering a wider conflict in the Middle East, especially if it involves tougher sanctions on Iranian oil, or allowing Israel to strike Iran’s oil facilities.

A fresh oil price shock is hardly what the Fed needs when it’s still struggling to tame inflation. As the world’s reserve currency, the dollar also stands to gain directly from risk-off episodes.

Summing up, although there’s not a lot on the horizon that can trigger a massive dollar selloff, its ability to continue marching higher hinges on the actual size of Trump’s tax cuts and tariff increases that will eventually be approved.

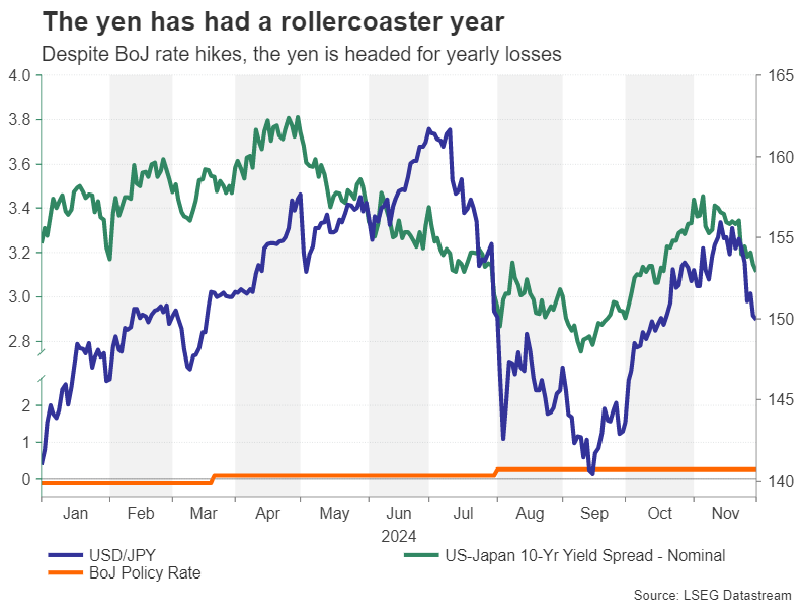

Yen’s rollercoaster ride

So where does all this leave the yen? The Japanese currency staged a dramatic recovery over the summer from levels last seen in 1986. The bullish reversal was driven by a combination of policy pivots by the Bank of Japan and the Fed, as well as direct intervention in the currency markets by Japanese officials.

However, the Bank of Japan’s hawkish surprises soon turned to caution and uncertainty about the pace of subsequent rate hikes has been weighing on the yen. But that’s not to say that the yen can’t restore its bullish posture in 2025.

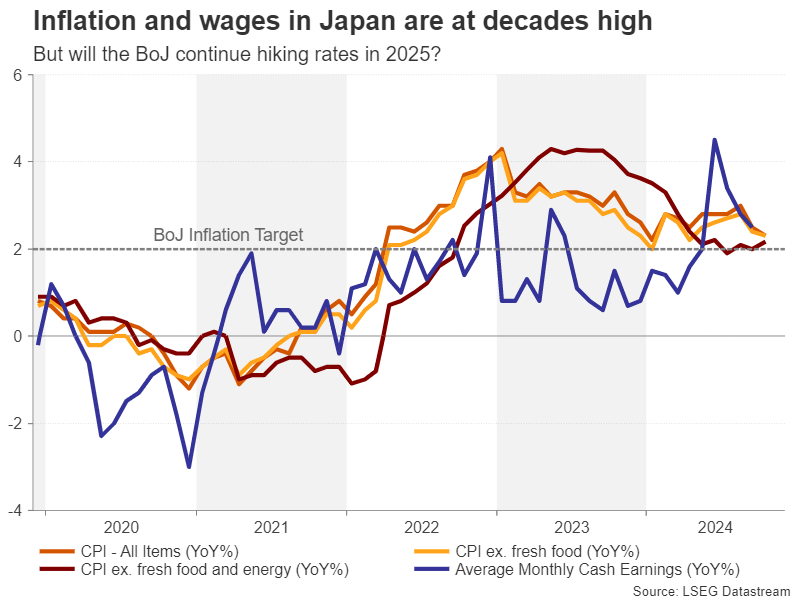

BoJ has one eye on wages

Although inflation in Japan has fallen to around 2.0%, policymakers see upside risks to the outlook from wage pressures as well as higher import costs from the weaker yen and increases in commodity prices. The BoJ is hopeful that next year’s spring wage negotiations will lead to another round of strong pay deals.

The country’s biggest trade union is aiming for wage increases of at least 5.0%. Such an outcome could pave the way for the BoJ to hike rates to 1.0% by the end of 2025.

Yield differentials matter

However, even if borrowing costs do rise to 1.0% or higher, yield differentials with the US might not necessarily narrow much if the Fed finds itself with very limited scope to trim its rates. Hence, whilst the BoJ may catch some investors off guard with its determination to normalize monetary policy, any yen rebound will depend as much on Fed policy as on domestic policy.

Still, with uncertainty hanging over the global economic outlook due to the elevated geopolitical tensions and Trump back at the White House, safe haven flows could also be the yen’s saviour in 2025.