{kind=link}

- A no-confidence vote to remove French PM Barnier pushed out by the far-right National Rally party may topple the French government this week.

- A current political fiasco in France has triggered an increase in the credit risk premium on longer-term French sovereign bonds.

- A further uptick in French sovereign bonds’ credit risk premium may lead to a major bearish breakdown on the more risk-sensitive EUR/CHF cross pair.

Since our last publication, the higher risk-sensitive EUR/CHF cross pair has wobbled as it grappled with the Eurozone’s economic weakness and a looming unfavorable external trade environment due to further global supply chain disruptions due to incoming US President-elect Trump’s 10% to 20% tariffs threat on other countries’ exports to the US, inclusive of the Eurozone.

The EUR/CHF inched lower in the week of 18 November (ex-post US Presidential election outcome on 6 November) and retested a key intermediate support of 0.9255, a key swing low made almost a year ago on 29 December 2023.

An increase in France’s sovereign bond credit risk premium

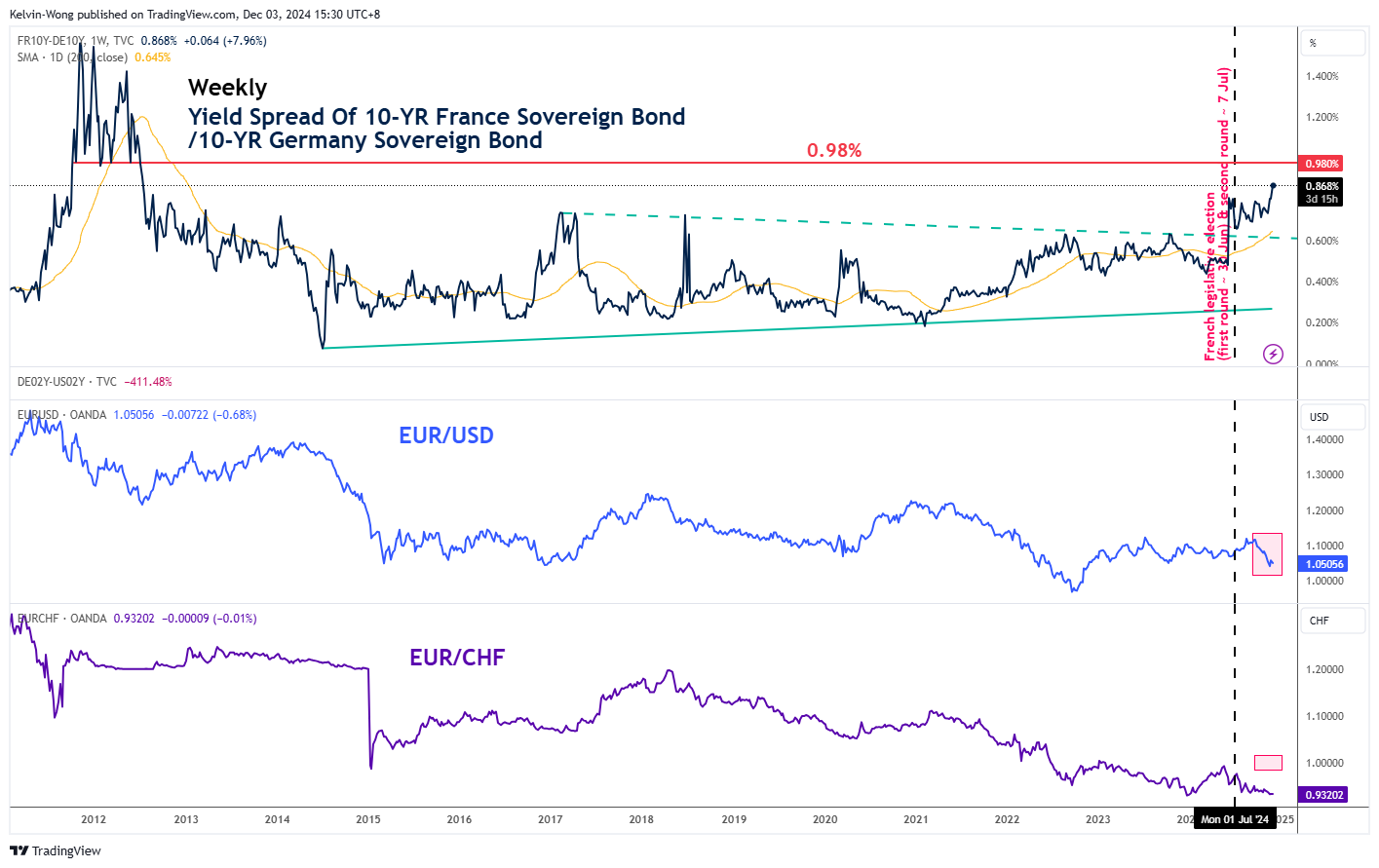

Fig 1: 10-year yield spread of French sovereign bond over German Bund as of 3 Dec 2024 (Source: TradingView, click to enlarge chart)

The credit risk premium of longer-term sovereign debt in France can be defined by the 10-year yield spread between France’s and Germany’s sovereign bonds (Bunds)

When the yield spread between 10-year France’s sovereign bonds over Germany’s Bund increases, it suggests a potential increase in the credit risk premium of holding French sovereign bonds.

Since the outcome of the second round of the recent summer French snap-National Assembly election on 7 July, the 10-year yield spread of France’s sovereign bonds over Germany’s Bund has continued to inch higher after its prior major bullish breakout that occurred earlier in the week of 10 June 2024 as the election results have led to a hung-parliament in France.

At the start of this week, the far-right National Rally leader Le Pen intensified her party stance to support a call for a no-confidence vote in the National Assembly to remove the incumbent French Prime Minister Barnier over his refusal to tweet his 2025 budget to suit the viewpoints of the National Rally party.

A no-confidence vote may happen as soon as this Wednesday, 4 December, and the French government may topple this week if things go in favour of Le Pen’s National Rally party.

A further increase in the 10-year yield spread of France’s sovereign bonds over Germany’s Bund towards the 0.98% medium-term resistance level may trigger further downside pressure in the EUR/USD and EUR/CHF (see Fig 1).

EUR/CHF’s last line of defence stands at 0.9255

Fig 2: EUR/CHF medium-term & major trends as of 3 Dec 2024 (Source: TradingView, click to enlarge chart)

The current price level of the EUR/CHF is being traded at 0.9320 at this time of the writing, just a whisker above the 0.9255 key intermediate support in place since its 29 December 2023 swing low.

The weekly MACD trend indicator has continued to inch downwards below its zero centreline which suggests a persistent major downtrend that increases the odds of a major bearish breakdown on the EUR/CHF (see Fig 2).

Watch the modified 0.9565 key medium-term pivotal resistance (also the 200-day moving average) and a break below 0.9255 with a weekly close below it may see fresh multi-year lows on the EUR/CHF to expose the next supports at 0.9085 and 0.8890 in the first step.

On the other hand, a clearance above 0.9565 negates the bearish tone for a squeeze up to revisit the 1.0040/1.1000 long-term pivotal resistance zone (also the upper boundary of the long-term secular descending channel in place since the April 2018 swing high).