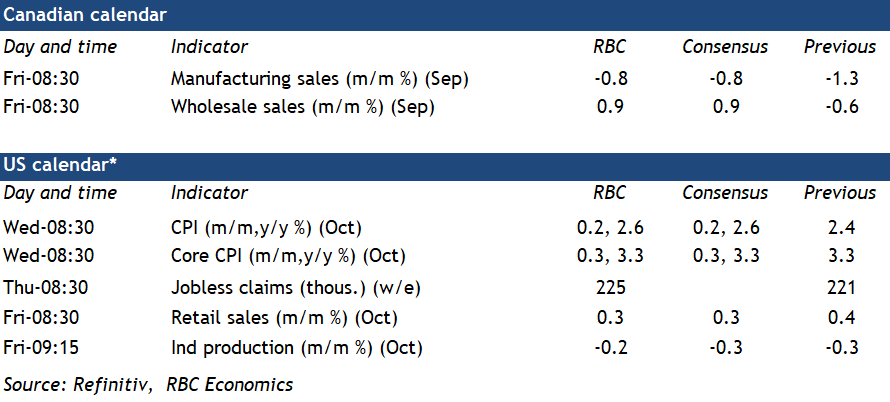

{kind=link}

U.S. inflation numbers will be closely watched by policymakers on Wednesday for any further signs that resilient growth domestic product and consumer spending is putting a floor under price growth.

U.S. GDP growth in Q3 was strong and a jump in auto sales in October means Friday’s retail sales report should show another increase early in Q4. But that strength has also come alongside firmer-than-expected inflation prints in recent months, and has markets questioning how quickly (and how much) the U.S. Federal Reserve will cut interest rates in the year ahead.

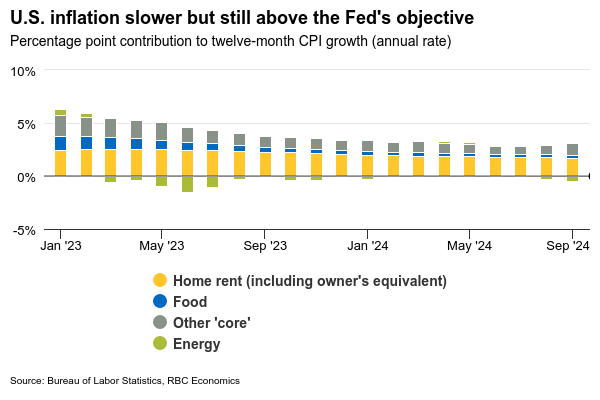

In October, we expect that U.S. headline consumer price index growth ticked up to 2.6% year-over-year from 2.4% in September. Average gasoline prices fell in October and food prices continue to grow at a pace closer to the Fed’s 2% target. But, sticky core inflation—which we expect held steady at 3.3% annually—continues to drive the bulk of price growth. Up until September, home rents were responsible for the lack of downward movement in the core measure. But last month, the share of CPI basket items (excluding shelter) reporting price growth above 3% moved higher from September.

The Fed takes a longer-term view of inflation data, with Chair Powell reiterating after a 25 basis point cut this week that price growth has still slowed substantially from where it was despite recent upside surprises. We continue to expect that gradual softening in labour markets will ease underlying inflation pressures enough to justify another Fed interest rate cut in December. But we also expect that interest rates will need to remain higher in 2025 than policymakers have been expecting to offset the inflationary impact of a large government budget deficit and keep price growth on a (sustainable) path back towards the Fed’s 2% objective.

Week ahead data watch

U.S. retail sales likely edged up again in October, given auto sales were strong. However, (a price-led) sales decline at gas stations would partially offset higher auto sales.

We expect the U.S. industrial production on Friday to inch lower in October, following the 0.3% decline in September. The weakness was mainly driven by lower output in the manufacturing sector as the impact of the Boeing strike and hurricanes dragged into October.