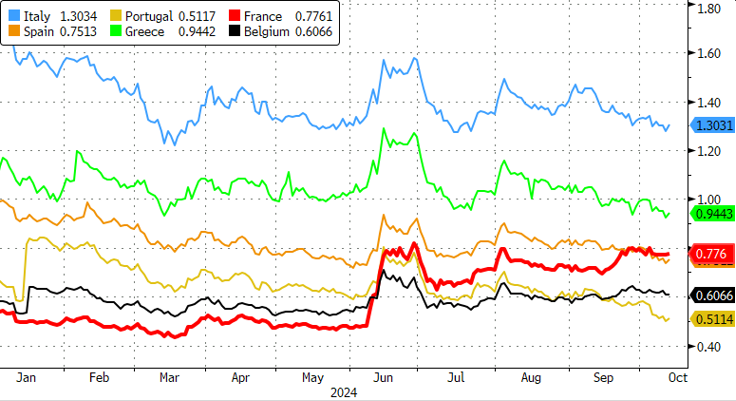

. German changes add 2 to 3 bps across the curve. French OAT’s underperform. The French-swap spread tests the multiyear high in the wake of yesterday evening’s budget release.){kind=link}

Markets

It’s more of the same today in absence of big events. Slightly below-consensus US PPI data only very briefly triggered a bid in US Treasuries which continued their bear steepening run. Daily changes on the US yield curve range between flat and +4.9 bps (30-yr). German changes add 2 to 3 bps across the curve. French OAT’s underperform. The French-swap spread tests the multiyear high in the wake of yesterday evening’s budget release. The government wants to implement €60.6 bn spending cuts and tax increases to avoid the budget deficit (expected at 6.1% of GDP) from increasing further. Via a 5% deficit next year, they aim to gradually get below the 3% Maastricht threshold by 2029, two years later than asked for by Europe. Lack of parliamentary majority complicates matters. EUR/USD holds steady around 1.0930 with risk sentiment showing no clear direction neither.

Next week’s eco calendar looks interesting. Chinese FM Lan Fo’an holds a press conference tomorrow. He’s expected to announce a new batch of fiscal aid to shore up to economy. It’s a second shot after earlier monetary and fiscal stimulus at the end of September. That triggered a 40%-50% rally on Chinese stock markets, half of which is undone after returning from golden week holidays. On Friday, China reports Q3 GDP data and September retail sales & production numbers. US markets are closed on Monday for Columbus Day Holiday, but a speech by Fed heavyweight governor, and possible successor of Fed chair Powell, Waller is worth watching. He speaks on the economic outlook at an event in Stanford. In the first half of the year, he advocated “what’s the rush?” (in favor of higher for longer). We think he’s still on that boat, but in the other direction. What’s the rush in making monetary policy rapidly less restrictive if inflation remains stuck above 2% and the labour market/economy doesn’t collapse? It’s in line with the mainstream view that the Fed will cut its policy rate by “only” 25 bps at the November policy meeting. Eco data include the Empire Manufacturing business survey (Tuesday), retail sales, Philly Fed business outlook & jobless claims (Wednesday) and housing data. It’s unlikely that they’ll spark the same amount of volatility as September payrolls and September CPI (in combination with jobless claims) did. The European focus simply centers on Thursday’s ECB policy meeting. Unaltered September GDP & CPI forecasts and the brief intermeeting period suggested that bar any surprises, the ECB would sit this meeting out before conducting a new policy rate cut in December. Awful EMU PMI business surveys and a confirmation of the disinflationary trend made Frankfurt changed tack. ECB president Lagarde told European parliament lawmakers that she would take the data into stride when deciding on policy in October. A large majority of ECB governors also backed a (25 bps) October rate cut. Barring any major economic surprises, we think a 25 bps rate cut is the most likely scenario for December as well.

News & Views

The German government earlier this week downgraded the 2024 growth forecasts into a 0.2% contraction. Having done so had the side effect of opening up borrowing (and spending) room under a mechanism enshrined in the country’s constitution that allows for additional spending in times of economic weakness. Bloomberg reported that Germany’s finance minister Lindner plans to take full advantage of that, resulting in a net increase in 2025 borrowing by about €5bn (to €56.5bn). The “windfall” helps close the €12bn budget financing hole for 2025 with the government banking on lower-than-expected outflows of other earmarked funds to close the remaining gap.

Canadian job growth topped consensus estimates in September. Net gains amounted to 46.7k, picking up from the 22.1k in August and almost double the 27k expected. Full-time jobs (+112k) more than compensated for a setback in part-time work (-65k). The unemployment rate unexpectedly fell back from 6.6% to 6.5%. This first decline since January was accompanied by a drop in the participation rate though, from 65.1% to 64.9%, the lowest since mid-2021. The employment rate, currently at 60.7% (-0.1 ppt), has trended downwards since the peak of 62.4% in early 2023 as labour force growth outpaced employment growth. Average hourly wages among employees increased 4.6%. The report is testament to a solid-to-strong labour market and questions the need for aggressive rate cuts by the central bank. BoC governor Macklem didn’t not want to rule out bigger (than 25 bps) cuts after lowering the policy rate by 25 bps to 4.25% in September. He made the comments back then when market momentum was building for the Fed to kick off with a super-sized 50 bps cut as well. Canadian money markets today pared bets for such a move at the October 23 meeting from 50% to 30% currently. The Canadian dollar clawed back some of the previous losses today but remains on track to print daily losses, extending its losing streak to 8 days. USD/CAD is trading around 1.375. Canadian government bond yields rise between 3.3 and 4.6 bps across the curve.

Graphs

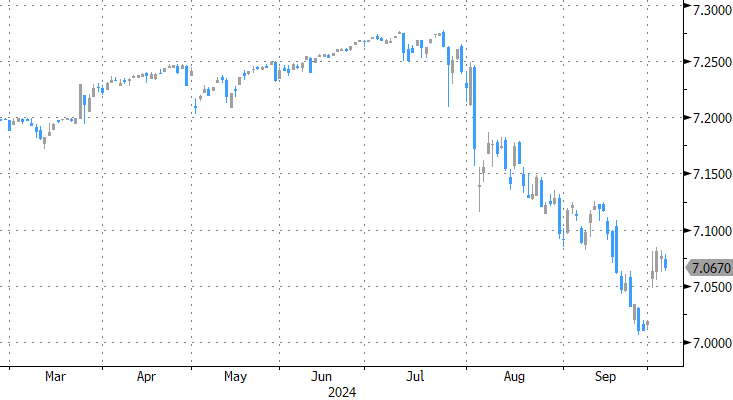

USD/CAD: can Loonie stop the rot following stronger Canadian payrolls?

French OAT’s continue underperforming after 2025 budget proposal

US 10-yr yield: bear flattening trend continues going into long US weekend

USD/CNY: all (Chinese) hopes on tomorrow’s update from minstry of Finance. More fiscal stimulus ahead?!