opened 1.0% lower. Yields eased a few basis points. However, the intraday momentum again changed in the run-up the US trading session. Yields reversed most of the early decline. US investors apparently still are focused on the potential impact of a ‘no-landing scenario’ for the US economy.){kind=link}

Markets

It look that a rather guarded reaction of Chinese investors this morning to recently announced stimulus would set the stage for some kind of a risk-off correction. European equities (EuoStoxx 50 ) opened 1.0% lower. Yields eased a few basis points. However, the intraday momentum again changed in the run-up the US trading session. Yields reversed most of the early decline. US investors apparently still are focused on the potential impact of a ‘no-landing scenario’ for the US economy. US yields currently show daily changes between -1.0 bps (2-y) and +2.5 bps (30-y). US eco data were few and very close to expectations (NFIB small business confidence and US trade balance). Fed Board member Adriana Kugler indicated a balanced approach on further Fed easing, but even after the strong payrolls repeated that the Fed wants to avoid an undesirable slowdown of the labour market. The focus remains on the maximum employment side of the Fed dual mandate. In this respect she warned against giving too much weight to one single data-print. Comments suggest that the bar for the Fed not continuing with steps of at least 25 bps remains high. Later today, we look out at investor appetite for a $58 bln 3-y Treasury Note auction after the recent rise in yields. German yields show no clear directional trend, changing less than 1.5 bps across the curve in a daily perspective. After yesterday’s correction, US equities again opened in positive territory (S&P 500 +0.37%). European indices reversed part of their early decline (EuroStoxx 50 -0.45%). Brent oil ($79.5 p/b) is trading off the ST peak levels ($81+) reached late yesterday.

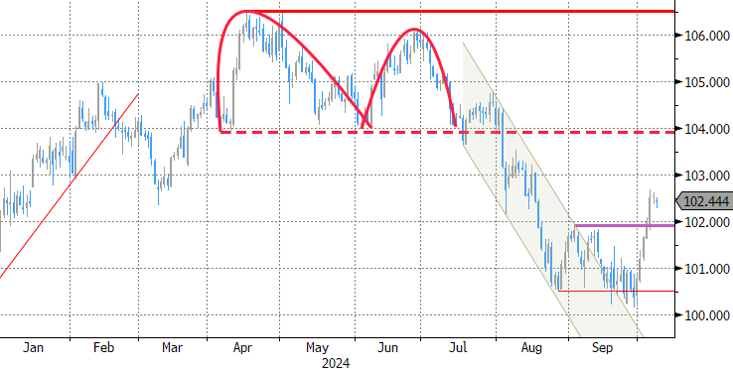

Moves in the major USD cross rates are modest. Intraday, the greenback to a large extent followed the dynamics of US yields. DYX (102.45) keeps the post-payrolls top (102.68) within reach. Similar narrative for EUR/USD (1.0975) and USD/JPY (148.10). Sterling this morning briefly weakened to revisit the EUR/GBP 0.84 barrier despite decent BRC retail sales (+1.7% Y/Y). Sterling captured a better momentum later (currently EUR/GBP 0.8378). Markets and analysts are becoming ever more focused on the first budget of the new Labour government scheduled for October 30 (FT article today). To the extent that especially higher LT UK yields mirror market caution on the ability of the new government to balance its plans to revive growth against the need for fiscal consolidation, this kind of rate support won’t help sterling.

News & Views

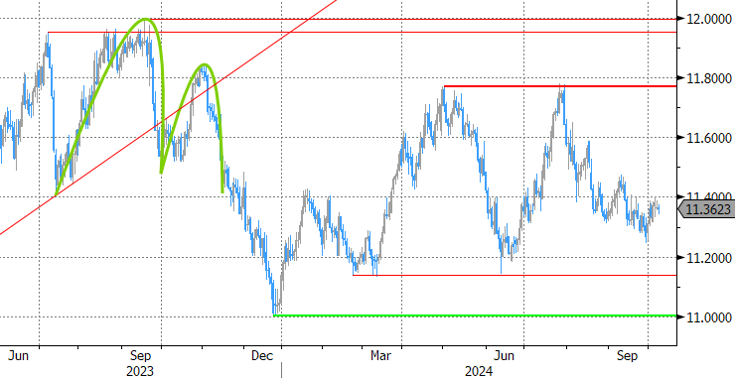

Swedish September inflation figures printed almost fully in line with consensus. Headline CPI rose by 0.2% M/M with the Y/Y-figure slowing from 1.9% to 1.6%. The Swedish Riksbank’s preferred CPIF gauge (using fixed mortgage payments), accelerated to 0.3% M/M. On an annual basis, CPIF inflation also slowed, from 1.2% to 1.1%. Core CPIF (excluding energy) showed the only small upward surprise, rising by 0.4% M/M (2% Y/Y from 2.2%). It’s the first time that Sweden statistics releases preliminary inflation readings. More detailed information and definitive figures will be available on October 15. Headline numbers won’t derail the Swedish Riksbank from cutting the policy rate (currently 3.25%) at this year’s two remaining policy meetings. The central bank in September even suggested that a cut of 50 bps is possible. EUR/SEK isn’t going anywhere today, treading water at 11.35.

National Bank of Poland policymaker Janczyk confirmed recent vibes that the central bank is working towards the March 2025 policy meeting as a potential game changer in its current higher-for-longer approach. If forecasts at that meeting confirm current assumptions of a sustained disinflation trend in the Q2 and Q3 2025, then the path to cutting rates will be open. Janczyk expects Polish inflation to peak at slightly below 7% in March or April. He added that the timing of cuts is now more to be found in the government’s fiscal policy than in monetary policy, echoing similar remarks by NBP governor Glapinski at last week’s press conference. The Polish zloty joins a CEE-wide rebound today with EUR/PLN slipping from 4.3230 towards 4.31.

Graphs

EUR/SEK: CPI data allow Riksbank to maintain its ‘aggressive’ easing bias. Krone hardly reacts.

UK 10-y yield rebounds sharply, at least partially due to market uncertainty on the UK’s fiscal position.

DXY (TW USD index): dollar maintains most of post-payrolls’ gains.

Iron ore future contract (DCE): Iron ore eases as investors aren’t convinced on China’s (fiscal) stimulus.