, but Hong Kong shares tumble (Hang Seng -7.0%). Markets apparently are not convinced that the recent monetary and fiscal measures will be able to profoundly change fortunes for the Chinese economy.){kind=link}

Markets

Investors yesterday continued to adapt positions in the wake of Friday’s impressive payrolls beat. The Fed recently indicated that inflation has cooled enough to the turn the focus to supporting growth and protecting a strong labour market. However, Friday’s payrolls and other US data of late are raising the question whether/how much support the US economy currently needs. Probably less than the Fed (and the market) assessed when the Fed started cutting rates with a 50 bps step back in September. After Friday’s sharp rise, US yields again added between 7.3 bps (2-y) and 5.5 bps (30-y). For the end of the year, 50 bps Fed cuts is still discounted, but markets see a limited chance of the Fed already being forced to take a pause in November (only 85% discounted). Fed officials, including New York Fed president Williams (FT this morning) indicate that the US economy is well positioned to keep strength in the economy and in the labour market and that it might result in a soft landing scenario. With respect to the pace of further easing, Williams indicates that last dots plot is a very good base case. The 50 bps start was a good decision at that time, but is no rule of how the Fed will act in the future. Returning to yesterday, German/EMU yields markets felt some spillover effects from the rise in the US, rising between 4.4 bps (2-y and 30-y) and 5.2 bps (5-y). (US) Equities this time didn’t build on the ‘no-landing’ gains that propelled indices on Friday and fell prey to profit taking. (S&P 500 -0.96%). After breaking several technical levels on Friday, the dollar rally ran into resistance (DXY 102.54, EUR/USD 1.0978).

Asian markets mostly show a mixed, hesitant picture this morning. Mainland China shares are gaining as markets reopen after the holiday period (CSI 300 +4.2%), but Hong Kong shares tumble (Hang Seng -7.0%). Markets apparently are not convinced that the recent monetary and fiscal measures will be able to profoundly change fortunes for the Chinese economy. There are few important eco data in the US and in Europe scheduled for release today. The focus remains on the US CPI data scheduled for release on Thursday. This evening we look out for a $58 bln sale of 3-y US notes. The US 2-y and 10-y yield are nearing the psychological barrier of 4.0% and markets have scaled back expectations on the pace of Fed easing to 25 bps (or even slightly less) for at least the four upcoming Fed meetings. For now, even after the strong payrolls, we think that enough easing is priced out. Both markets and the Fed now are in a genuine data-depended modus where guidance/and the market assessment might change with every batch of important data. Today, a mild risk-off also might cap a further rise in yields. In theory, this still should favor the dollar, but the greenback of late often resigned to its safe haven status.

News & Views

Total UK retail sales rose by 2% Y/Y in September according to data from the British Retail Consortium and KPMG. It’s the fastest pace since March and above that 12-month average of 1.1% growth. BRC chief executive Dickinson said that shoppers sought to update their wardrobes with coats, boots and knitwear as autumn rolled out across the UK. The start of the month also saw a last-minute rush for computers and clothing for the new academic year. Non-food sales fell by 0.3% Y/Y which is the slowest pace of decline YTD. Food sales increased by 3.1% Y/Y, the biggest increase since May. All eyes are now on the Budget and the impact that it will have on discretionary spending in the final, “Golden”, quarter of the year.

The head of the Bank of Italy’s economics and statistics department, Altimari, warned in parliament that the economy will expand less than previously expected this year. An accounting revision by Istat means a mechanical downward correction by 0.2 percentage points (0.4% from 0.6%) to the current year’s growth estimate. The current government growth forecast of 1% is becoming very unrealistic. The Italian central bank also called for a prudent approach to public finances, saying the government should concentrate on lowering the country’s mammoth debt, which is currently above 130% of gross domestic product.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) still is a source of concern, but very weak PMI’s and soft comments of Lagarde (and other MPC members) suggest the ECB is likely to step up the pace of easing with an October cut. Spill-overs from strong US data prevented a test of the 2.0% barrier. 2.00-2.35% might serve as a ST consolidation range.

US 10-y yield

The Fed kicked off its easing cycle with a 50 bps move. The Fed shifting focus from inflation to a potential slowdown in growth/employment made markets consider more 50 bps steps. Strong US September payrolls suggest the economy doesn’t need aggressive Fed support for now, but the debate might resurface as the economic cycle develops. For the US 10-y, 3.60% serves as strong support. The steepening trend is taking a breather.

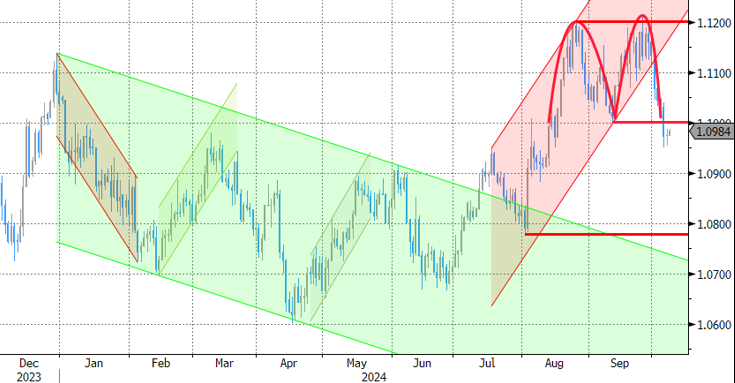

EUR/USD

EUR/USD moved above the 1.09 resistance area and twice tested the 1.12 big figure as the dollar lost interest rate support at stealth pace. Bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) partially offset some of the general USD weakness. After solid early October US data, the dollar regained traction, with EUR/USD breaking the 1.1002 neckline. Targets of this pattern are near 1.08.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness was indicated to be further unwound gradually. The economic picture between the UK and Europe also was increasingly diverging to the benefit of sterling, pulling EUR/GBP below 0.84 support. Dovish comments by BoE Bailey ended by default GBP-strength.