for the third consecutive meeting lowered its policy rate by 25 bps to 1.0%. Markets in advance even saw some probability of a 50 bps cut to prevent a further unwarranted rise of the Swiss franc. Inflationary pressures decreased significantly (1.1% in August). Imported goods and services contributed to the decline in inflation which also reflects the recent CHF appreciation. Overall, Swiss inflation is mainly driven by higher prices for domestic services. The new inflation forecast (1.2% for 2024, 0.6% for 2025 and 0.7% for 2026) is significantly lower than in in June and would have been even lower without today’s cut.){kind=link}

Markets

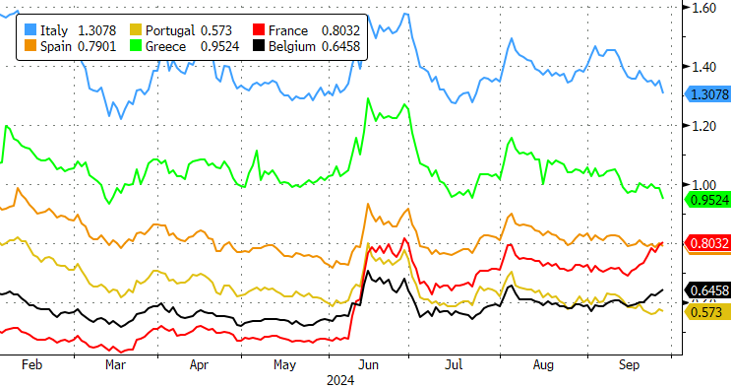

European trading mostly revolved around China’s Politburo promise of more forceful cuts, necessary fiscal spending and vow to stabilize the ailing real estate market in late Asian trading dealings this morning. It fired up stock markets, in particular Chinese. The CSI300 jumped another 4%+ and is headed for its biggest weekly gain in a decade. European markets bathed in the positive spillovers with the likes of the EuroStoxx50 eking out gains of >2% and the Stoxx600 bracing for a record close. The AUD and NZD are the best performers in currency markets. Their respective countries have important trade ties with China. German Bunds outperformed in core bond markets. German yield changes vary between -2.4 (30-yr) and -3.0 bps (2-yr) with the 2-yr testing the recent/March 2023 lows. The French spread vs. Germany’s 10-yr yield is grabbing some headlines. Growing risk premia push it above the Spanish one for the first time since 2007 (80 bps vs 79 bps). Investors increasingly worry about France’s fiscal mess and the inability of a frail coalition government to do something about it. US Treasuries swapped earlier gains for losses after the release of some second tier data. US durable goods orders topped estimates across the board, both on a headline level (0.5% vs -2.6% expected) and in the different core gauges. Shipments – used as a proxy for investment in GDP calculations – came in at the expected 0.1%. Weekly jobless claims eased from 222k to 218k, the lowest since May, defying expectations for an increase to 223k. US yields reversed earlier losses to trade +3 bps (2-yr) higher and flat at the back end ahead of what could have been a potential market mover: Fed chair Powell’s pre-recorded speech at the 10th annual US Treasury Market Conference. “Could have”, since Powell did not touch on monetary policy nor did he comment the economic outlook.

News & Views

The Swiss National Bank (SNB) for the third consecutive meeting lowered its policy rate by 25 bps to 1.0%. Markets in advance even saw some probability of a 50 bps cut to prevent a further unwarranted rise of the Swiss franc. Inflationary pressures decreased significantly (1.1% in August). Imported goods and services contributed to the decline in inflation which also reflects the recent CHF appreciation. Overall, Swiss inflation is mainly driven by higher prices for domestic services. The new inflation forecast (1.2% for 2024, 0.6% for 2025 and 0.7% for 2026) is significantly lower than in in June and would have been even lower without today’s cut. The strong Swiss franc, lower oil price and electricity price cuts announced for next January contributed to the downward revision. With modest Swiss growth this year (1.0%) and next year (1.5%) and slightly higher unemployment, the SNB expects that further rates cuts will be needed to ensure price stability. It repeated that it remains willing to be active in the FX market. In comments to Bloomberg Martin Schlegel, successor to current SNB president Thomas Jordan next week, indicated that current level still gives the SNB some room. He declined to say whether the franc is overvalued, but acknowledged that it is a challenge from some Swiss firms. CHF strengthened slightly (EUR/CHF 0.945).

In their joint economic forecast released today, Germany’s leading economic institutes revised the outlook for growth in the country further down. After a contraction of 0.3% in 2023 growth is again expected to be negative this year at -0.1% (0.2% in previous forecast). Next year’s recovery is expected to be weak (0.8% from 1.4%). Growth in 2026 is seen at 1.3%. In addition to the economic downturn, the German economy is being weighed down by structural change. “Decarbonization, digitalization, and demographic change – alongside stronger competition with companies from China – have triggered structural adjustment processes that are dampening the long-term growth prospects of the German economy.” Economic growth will not return to its pre-coronavirus trend for the foreseeable future. The economic standstill is now also showing clearer signs on the labor market with slightly increased unemployment (seen at 6.0% this and next year after 5.7% in 2023). Inflation is seen holding near 2.0% in the 2024-2026 period.

Graphs

Spreads vs. Germany’s 10-yr of selected countries: France’s tops Spain’s for first time since ’07 as fiscal/political risk premia rises

CSI300 on track for its biggest weekly gain in a decade as authorities promise forceful monetary and necessary fiscal support

EUR/CHF: Swiss franc puts aside SNB’s third consecutive rate cut, sticks near record high levels

AUD/USD: Aussie and kiwi dollar outperform on hopes for Chinese revival. New test of recent highs in the making