step up the pace of rate cuts with an ‘interim’ move in October rather than holding its quarterly pace with a next step in December.){kind=link}

Markets

After last week’s Fed decision, investors were happy to use soft/disappointing data to push money market pricing for ever more aggressive font-loading on Fed and ECB interest rate cuts. Fed members and even more ECB policy makers for now kept a balanced communication mostly favoring a gradual approach. Still markets now see a > 50% chance that the ECB will (have to) step up the pace of rate cuts with an ‘interim’ move in October rather than holding its quarterly pace with a next step in December. For the Fed, a cumulative 75+ bps further easing is discounted despite Fed dots suggesting a main scenario of two 25 bps steps. The US 2y yield is testing 3.55% support (low reached in the wake of the SVB crisis). The EMU 2y swap even trades at the lowest level since September 2022. Today, there was no eco news to further build on this front-loading exercise. It would be an exaggeration to call it a real rebound/correction, but US yields ‘rise’ around 3 bps, awaiting more directional impetus. German yields ‘add’ about 2-3 bps. Further out this week, US durable orders and jobless claims (tomorrow) and Friday’s (expected soft) US PC deflators, might keep yields near recent lows. The next real reference for markets and policy makers will come next week with the US ISM’s and next Friday’s payrolls. EMU flash September inflation will be published on Tuesday next week. The positive fall-out from Chinese multiple easing measures on (mostly) European equity markets already stalled (EuroStoxx 50 -0.2%). That also was the case for the impact on some cyclical commodities including Brent oil ($74/b).

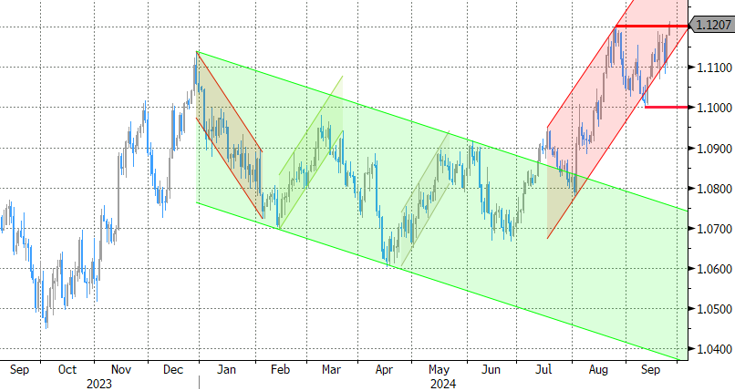

In line with global yields’ trends (easing of global financial conditions), the dollar is holding close to recent lows against most other majors (DXY 100.35). The yen underperforms as markets take somewhat of a more wait-and-see approach on the pace and timing of additional BoJ tightening (USD/JPY rises from 143.23 to 144.05). Maybe a bit strange given recent awful EMU data, EUR/USD remains well bid, slightly outperforming and challenging the YTD top at 1.1202. Sterling this morning briefly tested the GBP/USD 1.343 area (highest since end Feb 2022), but sterling outperformance gradually evaporated despite BoE Green advocating a cautious approach to BoE easing and the OECD upwardly revising UK growth this and next year. After testing the 0.8320 area yesterday, EUR/GBP today rebounds to trade in the 0.8365 area. Cyclically sensitive currency (AUD, NZD, CAD, NOK) and smaller currencies (CZK, HUF, PLN) also are ceding marginal ground.

News & Views

The Swedish Riksbank cut its policy rate for a third time this year and for a second consecutive meeting by 25 bps, from 3.50% to 3.25%. If the outlook for inflation and activity remains unchanged, the policy rate may be cut at the two remaining meetings this year. A 50 bps rate cut is possible at one of these meetings. During H1 2025, the Riksbank also plots one or two further rate cuts (towards 2.25%). That’s a faster path than previously indicated which will contribute to stronger growth and inflation close to target. Updated core inflation forecasts show an average of 1.7% and 1.6% in 2024-2025, down from 1.8%-1.9% in June. The GDP pace is downwardly revised for this year (0.8% from 1.1%) with the recovery set to accelerate next year (1.9% from 1.7%) and in 2026 (2.5% from 2.4%). Risks to the scenario are linked to the recovery in the Swedish economy, the geopolitical unease, and the krona exchange rate that can lead to a different outcome for inflation and the stance of monetary policy. The krona isn’t impressed by the dovish RB turn. A large part was discounted. EUR/SEK holds near lowest levels since June at 11.31.

The OECD published its interim economic outlook today. With robust growth in trade, improvements in real incomes and a more accommodative monetary policy in many economies, the outlook projects global growth persevering at 3.2% in 2024 and 2025, after 3.1% in 2023. Inflation is projected to be back to central bank targets in most G20 economies by the end 2025. Headline inflation in the G20 economies is projected to ease to 5.4% in 2024 and 3.3% in 2025 (6.1% in 2023, with core inflation in the G20 advanced economies easing to 2.7% in 2024 and 2.1% in 2025. OECD Secretary-General Cormann sees the global economy starting to turn the corner. Downside risks include a larger than expected impact on demand from tight monetary policies and persisting geopolitical and trade tensions. Rebuilding fiscal space is key to be able to react to future shocks and future spending pressures, including from population ageing and needed investments in the digital transformation and the climate transition.

Graphs

EUR/SEK: krona holding up well even as Riksbank signals to speed up pace of policy easing/normalization.

EUR/USD setting new YTD top. Considerations of global easing outweigh poor EMU data.

EUR/GBP: sterling taking a breather after recent outperformance against the euro (and the dollar).

EUR/CZK: Krone shows no directional trend. CNB maintains 25 bps easing pace.