{kind=link}

- The Fed announced its first rate cut with a relatively balanced rhetoric

- History points to a high probability of back-to-back moves

- Dollar/yen and Treasury yields tend to drop until the second rate cut

- Barring a major event, stocks’ positive performance could continue

The Fed commenced its monetary policy easing cycle in aggressive fashion by announcing an almost unanimous decision to cut rates by 50bps. The markets were surprised with the US dollar suffering the most. Both the accompanying policy statement and the press conference were relatively balanced as Chairman Powell tried very carefully to avoid scaring the market by talking down the US economy.

The Fed is probably on a preset course, despite Powell advertising the meeting-by-meeting approach shared by other central banks. The dot plot revealed two additional 25bps rate cuts penciled in by Fed members for 2024, slightly below market expectations for another 72bps of easing this year. What does history tell us about the timing and size of the second Fed cut?

Is it standard practice for the Fed to announce back-to-back rate cuts?

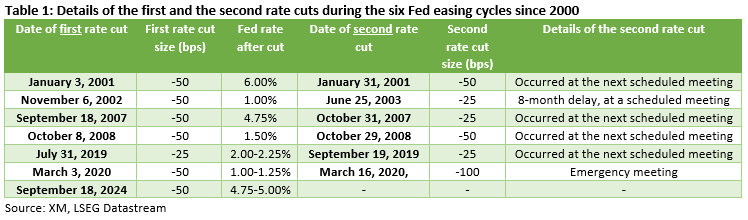

Continuing from a previous special report where six easing cycles were identified since 2000, table 1 below presents the details of the Fed’s first and second rate cuts. As made evident, Fed members decided to cut rates again at the next scheduled meeting in four of the six examined cycles, increasing the possibility for a November 7 rate move.

Interestingly, Fed decisions varied from a 100bps rate cut in 2020, during the outbreak of the Covid pandemic, to just 25bps moves in 2002, 2007 and 2019, when the US economy was not falling off a cliff. Also, the time between the first and the second Fed rate cuts fluctuated from just 13 days in 2020 to almost 8 months in 2002, as the Fed traditionally tries to act appropriately in order to meet its dual mandate.

The next Fed meeting is scheduled for November 7, two days after the US presidential election day. Quite possibly, the result of the election might not be yet finalized, especially if the Republican presidential candidate is losing the battle. This raises the possibility of the Fed refraining from announcing another rate cut until the new president is declared. However, the market is convinced that the November rate cut is a done deal, and it is even assigning a sizeable 43% probability for another 50bps move.

How did the market perform between the first and second Fed rate cuts?

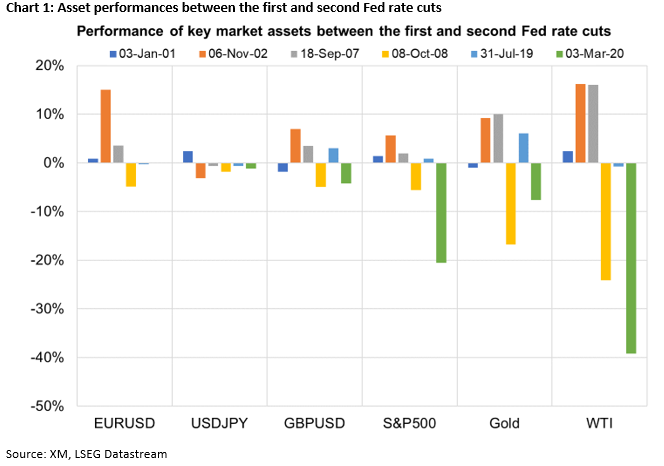

Chart 1 below presents the performance of key market assets in the period between the first and the second Fed rate cuts. Interestingly, dollar/yen dropped by an average of 1.5% in the last five easing cycles, a performance that could repeat this time around as the Bank of Japan is still open to further rate hikes in 2024.

Similarly, US treasury yields tend to fall in the examined time period, with one grave exception. In 2008, yields rose by 20bps as the US administration borrowed heavily from the bond market in order to fund its relief programmes.

Performance for certain assets depends on the underlying economic conditions

As seen in chart 1 below, the remaining assets exhibit a relatively mixed performance. However, digging through the results there is a common pattern emerging in pound/dollar, S&P 500 index, gold and WTI oil price. In periods of distress like 2008 and 2020, these four key assets tend to drop aggressively. For example, the S&P 500 index fell by 5.6% and 20.6% respectively in these two instances, and WTI oil prices collapsed.

In periods of normal economic conditions, like the current situation, the Fed has traditionally opted for a more relaxed approach in terms of its rate cuts. As a result, in 2001, 2002, 2007 and 2019, pound/dollar, S&P 500 index, gold and WTI oil exhibited a stronger tendency to rally. More specifically, the S&P 500 index increased by an average of 2.4% in these four periods, while both gold and WTI oil showed a decent appetite for double-digit jumps.

Putting everything together, dollar/yen and the 10-year US treasury yield tend to decrease in the period between the first and the second Fed rate cuts. The performance of other key assets like pound/dollar, the S&P 500 index, gold and WTI oil depends on the underlying economic conditions. As such, in both 2008 and 2020 these assets dropped aggressively, while during the period between the first and the second Fed rate cuts in 2001, 2002, 2007 and 2019, they recorded strong gains.