. Core inflation reaccelerated to 0.5% M/M and 3.6% Y/Y (from 0.1% and 3.3%). Similar story applied to services prices rising by 0.4% M/M and 5.6% Y/Y (from 0.5% and 5.2%).){kind=link}

Markets

Focus this morning briefly turned from this evening’s Fed meeting to tomorrow’s BoE policy decision following August UK CPI data. The report was almost exactly in line with expectations. Headline inflation rose 0.3% M/M and 2.2% (from -0.2% M/M and 2.2% in July). Core inflation reaccelerated to 0.5% M/M and 3.6% Y/Y (from 0.1% and 3.3%). Similar story applied to services prices rising by 0.4% M/M and 5.6% Y/Y (from 0.5% and 5.2%). While core services inflation is affected by some highly volatile components like airfares, today’s data still show too much stickiness for the Bank of England to take another advance on the hoped-for further cooling of inflation. Admittedly, at least part of the MPC is probably keen to turn the focus from inflation to growth. A new reassessment can only take place on the basis of the next Monetary policy report at the November 7 policy meeting. UK gilts underperformed Bunds and Treasuries with yields rising 6 7 bps across the curve. Markets for now only see room for further gradual easing by 25 bps steps in Q4 and Q1 next year. Sterling outperforms the dollar (GBP/USD 1.3215) and the euro (EUR/GBP 0.8415 from 0.8430). A test of the 0.8400/0.8383 support area might be on the cards. Even so, if the BoE holds such cautious approach against the background of weak UK activity data stay weak (cf last week’s rather poor July production/GDP data), it’s doubtful that ‘longer-lasting’ interest rate support will be a big help for sustained further sterling gains.

In global markets outside the UK, the countdown to this evening’s Fed interest rate decision caused some further mild profit taking on recent protracted easing bets. US yields add between 2 bps (2-y) and 3.5 bps (30-y). German Bunds slightly underperform treasuries with yields rising between 2.5 bps (2-y) and 5.5 bps (30-y). ECB Nagel, while supporting the start of easing, indicated that the ECB will have to show ‘staying power’ to fully reach to 2% target. In this process, he warned that policy rates certainly won’t go down as quickly and sharply as they went up. The dollar is losing a few ticks (DXY 100.8, EUR/USD 1.1135, USD/JPY 141.75). Equities show no clear trend (Eurostoxx -0.4%, S&P 500 unchanged) With respect to this evening’s Fed decision, we prefer a scenario of Powell and co starting with a substantial reduction of policy restriction (50 bps) to avoid an unnecessary weakening of the labour market. Current high policy yield levels allow to do so. It still leaves the Fed the option to make a revaluation on both inflation and growth with the policy rate above neutral (end this year/early next year). In this scenario, an assumed additional cumulative 75 bps of easing signaled in the median dot plot for the remainder of the year might still support recent dynamics of markets staying asymmetrically sensitive to softer than expected activity/labour market data. The message from the dots for 2025 might be much less aggressive than what markets are currently discounting, but it’s probably too early as a driver for markets in the near term. In this context we also stay cautious on the dollar.

News & Views

South African inflation slowed to 0.1% M/M in August from 0.4% in July and below 0.2% consensus. In Y/Y-terms, headline inflation fell below the 4.5%-midpoint of the South African central bank’s inflation target (3%-6%) for the first time since April 2021. Core inflation was flat in August but slowed from 4.3% Y/Y to 4.1%. Today’s benign inflation print cements the case for a first 25 bps by the SARB since hitting the current peak at 8.25% in May of last year. Fortunes of the South-African rand improved since the start of the summer on global USD-weakness as markets prepare for less restrictive monetary conditions. Emerging market currencies tend to profit from these prospects in general. USD/ZAR is setting new YTD lows today below 17.60.

US housing starts rebounded by 9.6% M/M in August, coming off a 6.9% drop in July. In absolute numbers, the 1356k annualized rate is the highest since April. New construction of single-family homes increased almost 16% to an annualized 992k pace (3 month best). Starts of multifamily projects declined for the first time since May. Overall building permits, a pointer for future construction, rose by 4.9% M/M (from -3.3% M/M) with the annualized rate of 1475k being the best since March. Both figures beat market consensus..

Graphs

EUR/GBP: Sterling outperforms the euro (and the dollar) as BoE for now has little room to cut interest rates aggressively.

USD/ZAR: rand profits from easing of global financial condtions even as softer inflation opens the door to SARB easing.

US 2y yield: Markets await Fed’s ‘nihil obstat’ to discount more frontloading

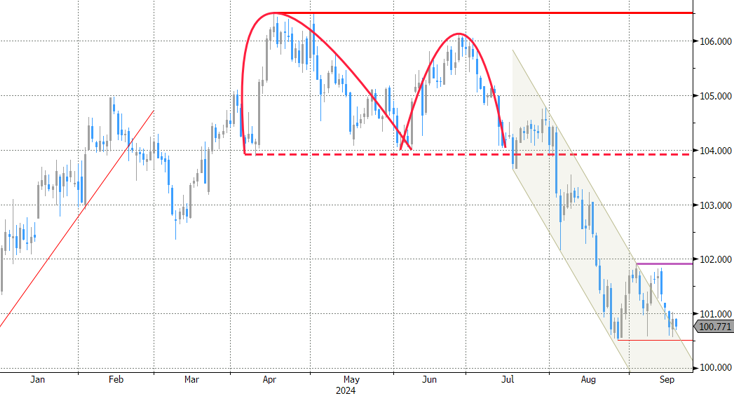

DXY TW USD ready to attack key support