and Holzmann (Austria) did so last week. Kazimir (Slovakia) today said that the next move (down) “must almost surely wait until December”. De Guindos and Lane, the VP and chief economist respectively, doubled down on president Lagarde’s message of gradualism and data-dependency.){kind=link}

Markets

A range of ECB speeches in the wake of last week’s policy decision confirmed the different approach of Frankfurt – in all likelihood – is taking compared to the Fed. Kazaks (Latvia) and Holzmann (Austria) did so last week. Kazimir (Slovakia) today said that the next move (down) “must almost surely wait until December”. De Guindos and Lane, the VP and chief economist respectively, doubled down on president Lagarde’s message of gradualism and data-dependency. The latter added that there should be optionality about the easing speed though. It is nevertheless an increasingly stark contrast with the kind of frontloading the Fed may be prepping for. With 42 bps of cuts priced in for Wednesday, markets attach a +/- sizeable 65% probability of a large inaugural cut. Not delivering on these bets could unsettle markets. That leads some to believe that if there is no unofficial communication in the next several hours (through the likes of WSJ), the Fed will (have to) start off big. The heated topic keeps US yields in the defensive. The first unexpected positive reading since November 2023 of the NY Fed’s manufacturing survey (11.5 from -4.7 with the 6-month ahead gauge at the highest since March 2022) did little to alter the move but kept the intraday lows away. Front end outperformance brings about a decline of 2.7 bps (2yr). The long end eases <1 bps. Bund yields are marginally down 0.7-1.3 bps across the curve in sympathy. The US dollar hangs in the ropes once again. The trade-weighted DXY is testing December 2023 support around 100.6. EUR/USD jumped beyond 1.11 and fell just short of a test of a first intermediate resistance around 1.1139. USD/JPY hit a new YtD low with the 140 barrier looking shaky. Sterling captures a nice bid against USD (Cable tests 1.32) and the euro (EUR/GBP 0.843). The Bank of England is meeting on Thursday but is expected to leave the policy rate unchanged at 5%.

News & Views

Eurostat published Q2 labour cost data today. They rose by 4.7% Y/Y for the euro area and by 5.2% Y/Y for the EU, respectively down from 5% Y/Y and 5.5% Y/Y in Q1. On a country level, the highest increases in hourly wage costs for the whole economy were recorded in Croatia (+17.6%), Bulgaria (+15.4%), Romania (+15.0%), Hungary (+13.2%) and Poland (+13.0%). Two more EU Member States recorded an increase above 10%, namely: Latvia (+11.0%) and Lithuania (+10.9%). In the EMU, the cost of hourly wages & salaries increased by 4.5% Y/Y while the non-wage component increased by 5.2% Y/Y. On a sectoral level, wages went up by 4.5% in services, by 4.8% in industry and by 5.3% in construction. Today’s data add to evidence that underlying price pressure in the euro area remains sticky, preventing the ECB from making monetary policy less restrictive at a rapid pace.

• The National Bank of Poland today published core inflation data for the month of August. The Polish statistical office already published general CPI data earlier, with headline CPI at 0.1% M/M and 4.3% Y/Y. The NBP publishes four core calculations. Core inflation excluding food and energy prices came in at 0.3% M/M and 3.7% Y/Y (down from 3.8%). Other measures remained modest at 0.1% M/M for CPI ex administered prices (2.9% Y/Y), 0.1% M/M also for the series excluding most volatile price components (4.8% Y/Y) and the 15% trimmed mean average at 0.2% M/M and 4.0%. The NBP targets inflation at 2.5% with a 1.0% +/- tolerance band. Polish headline inflation in July jumped above the NBP’s tolerance band as the government phased out some inflation shield measures. Higher headline inflation, a loose budget and strong wage growth are mentioned by the NBP as factors preventing a rate cut in the near term. Still some MPC members recently opened de door to start discussion in the first quarter of next year.

The Bank of International Settlements (BIS) published its quarterly review, titled “carry off, carry on”. One of the main lessons is that the unwinding of leveraged positions, including carry trades, which triggered short-lived bouts of extreme market volatility and FX movements early August isn’t going the be a one-off. “It’s part of the bigger picture, the inevitable withdrawal symptoms that markets suffer as they transition away from the extraordinary period of exceptionally low interest rates and ample liquidity”, according to BIS head of the monetary and economics department Borio. Markets have become hypersensitive to growth-related news surprises and the associated revisions to expectations of the policy stance ahead. In contrast to equity markets, volatility in credit markets remained subdued and conditions generally benign.

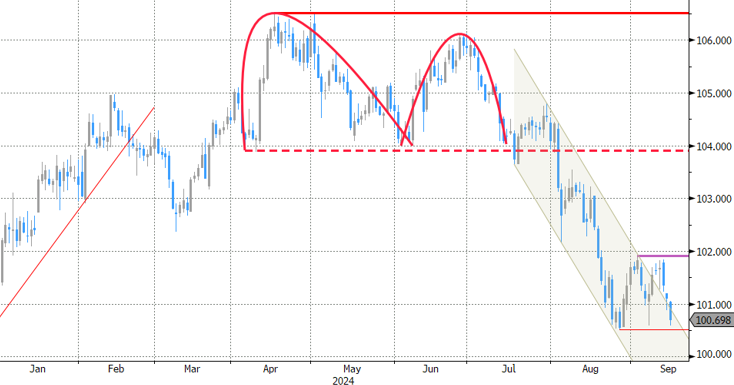

Graphs

US 2y yield tests March 2023 low as odds for big Fed start rise

DXY: trade-weighted dollar index suffers under loss of yield support

Vix equity volatility index eases from recent highs but remains at elevated levels compared to recent history

EUR/PLN nears the recent lows as PLN investors try to figure out the NBP easing intensions