and energy services (-0.9%) as key downward influences.){kind=link}

Markets

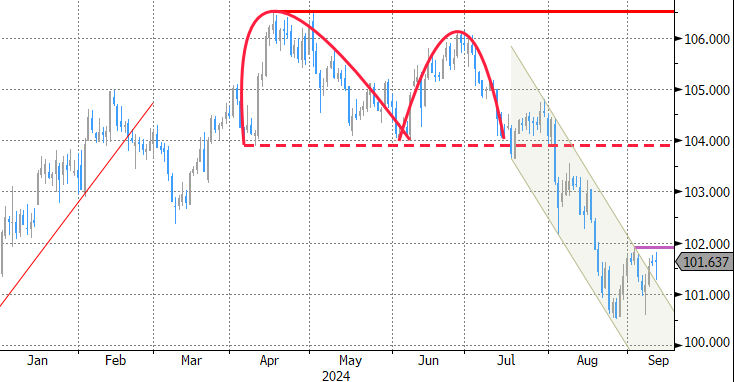

US August inflation is another piece for the Fed’s puzzle next week. Headline CPI rose again and as expected by 0.2% M/M with the Y/Y-figure slowing as anticipated from 2.9% to 2.5%. Core CPI accelerated from 0.2% M/M in July to 0.3% while consensus was looking for a 0.2% pace as well. Core CPI stabilized nevertheless as hoped at 3.2% Y/Y. Details showed energy (-0.8% M/M) and energy services (-0.9%) as key downward influences. Food prices rose by 0.1% M/M and services excluding energy by 0.4% M/M (4.9% Y/Y). Shelter costs accelerated to 0.5% M/M (5.2% Y/Y) and was the main (upside) factor in today’s inflation print. The so-called supercore services inflation gauge accelerated from +0.21% M/M to +0.33% M/M (4.46% Y/Y, flat). Rates markets were initially wrongfooted by the small upside core CPI release with headlines screaming that it takes the case of a 50 bps rate cut by the Fed off the table next week. Others argue “more noise than news” or “hardly a game-changer” and that’s also how we’ll likely interpret today’s market action by the end of the trading day. The jury is still out for the outcome of next week’s FOMC meeting. The US 2-yr yield initially spiked by around 10 bps, reversing yesterday’s decline, but as we close our report there’s only half of the gain left. Increases at longer tenors stretch from 1 bp (30-yr) to 3.5 bps (5-yr). German yields are flat on the day going into tomorrow’s ECB meeting where we expect Lagarde and co to cut the deposit rate a second time by 25 bps but refrain from committing to more action in October. EUR/USD dipped from 1.1050 to currently 1.1015. The trade-weighted dollar is unchanged for the day at 101.65. For now, first resistance at 101.92/102 stays out of reach. USD/JPY this morning briefly touched its lowest level YTD on hawkish comments by BoJ Nakagawa (140.71) before returning to opening levels around 142.12. Key US stock market open with losses of up to 0.9% for the Dow Jones. Oil prices try to regain the $70/b barrier (Brent) after their non-stop slide this month from levels just above $80/b.

News & Views

In comments during a four-day trip in China, Spanish Prime Minister Pedro Sanchez indicated that his country is considering a change in its position on imposing additional tariffs on the import of electric vehicles produced in China. “We have need to reconsider – all of us, not only the members states but also the Commission – our positions towards this movement”. The comments are a sign of growing division among European members states as the European Commission prepares to add additional levy’s by the end of October. Tariffs in the commission’s proposal might be raised by up to 37.6%. The measures are a response against Chinese car makers benefiting from unfair state subsidies and the country flooding the EU with its excess car production. In response, China also started anti-dumping investigations, amongst others, into EMU dairy and pork exports. Spain is an important exporter of pork to China. A qualified majority of member states is necessary to block a decision of the commission on tariffs.

In a speech earlier today, assistant governor Sara Hunter of the Reserve Bank of Australia assessed that labor market conditions, while easing, remain relatively close to full employment. In particular, she saw strength in hours worked, underemployment and participation somewhat surprising. The unemployment rate has gradually increased to 4.2% from a cycle low of 3.5% last year. From the current point in the economic cycle, the RBA expects employment to continue to increase, but a slower pace than population growth. This might further ease labour market conditions. An ongoing strong labour market was one of the reason for the RBA to keep policy restriction at its current level (policy rate at 4.35%). The RBA has its next policy meeting on September 24 and is not expected to already join the global easing cycle of other centrale bankers. Markets attach a 75% probability to a first rate cut at the December meeting.

Graphs

US 2-yr yield: dead cat bounce?

Trade-weighted dollar (DXY): still no real test of first resistance at 101.92/102

EUR/GBP: unmoved by UK eco data for second straight session

US 10-yr real yield: accumulating bets on less restrictive policy