{kind=link}

Markets

Spotting significant market moves is like looking for a needle in a haystack today. We give it our best shot anyway by diving into a bumper bond sale taking place in Italy. The southern country’s 30-yr auction drew a record €130bn+ in demand, allowing it to tighten the final terms from BTPS+15 bps area to BTPS+13. It eventually raked in an amount of €8bn. Italian bonds (marginally) outperform regional peers with spreads easing 2 bps (10-yr). It’s 30-yr bond yield is hovering near the recent lows just north of 4.2%. Yields in core areas including the US and Germany trade little changed. US Treasuries gained a slight upper hand over Bunds in early US dealings with yields easing 1.5 bps at the front. Currency markets are an ocean of calm. EUR/USD oscillates around the 1.104 opening levels. The trade-weighted dollar index takes a breather at 101.65 after some proper gains over the previous two trading gains. The Norwegian krone outperforms G10 peers. The Scandinavian currency’s recent track record was poor with EUR/NOK moving from 11.6 end of August towards but below 12. Slightly weaker than expected Norwegian headline inflation this morning nudged EUR/NOK within inches of that psychologically important figure. But lacking strength for a technical break higher, it triggered some return action instead (EUR/NOK currently offered at 11.90). Sterling reversed some earlier gains after a slightly better than expected labour market report this morning to trade virtually unchanged at EUR/GBP 0.844 and GBP/USD 1.307. The slow start of the week after today is giving way for hopefully some more live action. The eco calendar from tomorrow on heats up with the first (and probably only) presidential debate starring Trump and Harris at 3am CEST, followed by US inflation numbers in the afternoon. The ECB takes center stage on Thursday with a second 25bps rate cut all but certain.

News & Views

Czech inflation slowed from 0.7% M/M in July to 0.3% in August, though consensus hoped for a sharper slowdown to no growth. Main price drivers were “alcoholic beverage, tobacco” and “food and non-alcoholic beverages”. Prices of goods in total increased by 0.1% (0.5% Y/Y) and prices of services by 0.5% (5% Y/Y). Actual rent prices rose by 0.3%. Annual inflation remained stuck at 2.2% Y/Y. In the Y/Y-comparison, the impact of higher food prices was offset by lower fuel prices. The biggest influence came again from “housing, water, electricity, gas and other fuels”. Today’s inflation number compares with a 1.8% Y/Y forecast in the Czech National Bank’s summer forecasts. Core inflation (2.4% Y/Y) is also somewhat higher than predicted, as is monetary policy-relevant inflation (2.1% instead of 1.7%). The CNB commented that core inflation is being driven by wage growth in the domestic economy, which is affecting services prices in particular. Partly offsetting this is a decrease in the profit mark-ups of producers, retailers and service providers. The recent property market recovery has been reflected in faster growth in imputed rent. Today’s release didn’t alter market thinking on the outcome of the next, September 25, monetary policy meeting (25 bps rate cut). EUR/CZK made another minor attempt to dive below 25, but failed as it has been doing since the end of August.

It was the other way around for Hungarian inflation. From a similar 0.7% M/M-pace in July to flat price growth in August (vs +0.2% consensus) with the Y/Y-number falling back in the tolerance band around the central bank’s 3% inflation target (3.4% Y/Y from 4.1% vs 3.6% consensus). Details showed stable food prices in August while services prices rose by 0.4% and rents by 0.9%. Prices for clothing and footwear and for electricity, gas and other fuels, fell. It’s welcome news for the central bank who skipped a rate cut in August, hoping to find the right settings in September. Inflation developments, the reaction function of the Fed/ECB and risk perception (HUF) are key in the decision making process. Only the latter is becoming an issue in continuing the cutting cycle with EUR/HUF yesterday spiking to 397 on reports that PM Orban intends to raise spending going into 2026 elections, potentially derailing public finances.

Graphs

EUR/CZK: Czech crown attempt to strengthen beyond 25 fails as higher-than-expected inflation had no strong enough legs

EUR/HUF: forint is trying to look for a bottom after a recent drop amid resurgent fiscal spending worries

Italian 30-yr yield nearing the lower bound of a sideways trading range. Today’s auction drew record demand

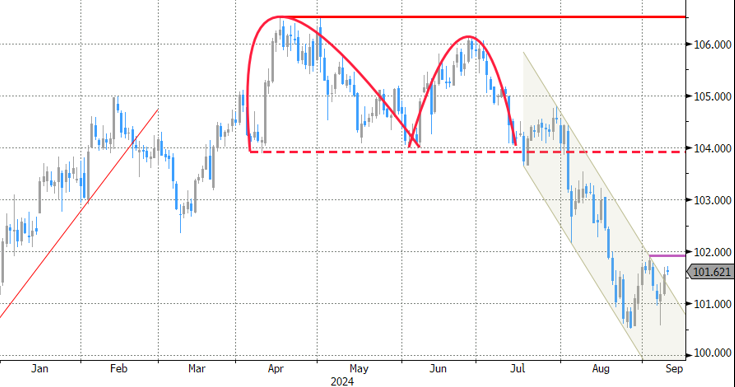

DXY has set its sights on first resistance around 102. Will inflation numbers tomorrow do the trick?