from the BoC meeting next week to build on cuts already delivered in each of the prior two meetings in June and July. Comments from Governor Macklem will likely again err on the dovish side, continuing to emphasize a softening economic backdrop that makes it more likely that inflation will keep trending lower.){kind=link}

We expect another 25-bps cut to the overnight rate (to 4.25%) from the BoC meeting next week to build on cuts already delivered in each of the prior two meetings in June and July. Comments from Governor Macklem will likely again err on the dovish side, continuing to emphasize a softening economic backdrop that makes it more likely that inflation will keep trending lower.

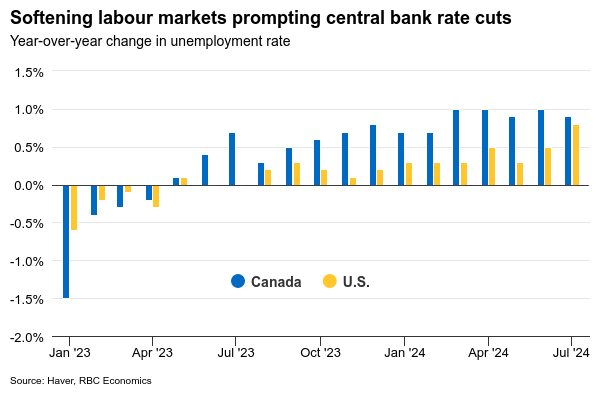

CPI prints, although still important to the BoC’s consideration, are backward-looking and lag the economic backdrop that has continued to soften. The 2.1% annualized increase in Q2 GDP was above the 1.5% gain that the BoC expected in the July MPR but still left per-capita output down for the seventh in the last eight quarters. The unemployment rate is up almost a percentage point from a year ago – and we expect another increase (to 6.6%) in August to be reported next Friday as employment continues to grow at a slower pace than the size of the labour force.

Governor Macklem reinforced after the last rate cut in July that the central bank is convinced inflation will continue to drift lower even if “there could be setbacks along the way,” but July CPI data also surprised on the downside. Moving forward, the hurdle for more BoC rate cuts from what are still-elevated levels is low. Our own base-case assumes another 150 basis points of cuts (including the expected September reduction) by mid-2025.

While the decision for the BoC to pivot to lower interest rates this year was likely relatively easy, the economic backdrop for the U.S. Federal Reserve has been more complicated. Resilient U.S. GDP growth and a flare-up in inflation pressures earlier this year has kept the Fed on the sidelines for longer than other advanced economies. But a downside surprise in U.S. labour market data in July jolted worries that a feared more significant labour market slowdown may have started, with a rise in the unemployment rate breaching thresholds usually only seen during U.S. recessions (the so-called ‘Sahm’ rule.)

For now, slowdown has been more of a ‘normalization ’ than a crumbling in the broader economic backdrop with the unemployment rate rising but to levels that are still low. And we expect a surge in temporary layoffs in July will at least partially reverse in August. Further sharp deterioration in labour market conditions is not in our base case and, as Powell made clear at Jackson Hole, would not be welcomed by Fed policymakers. If, however, next week’s report was to show a significant number of those ‘temporary’ layoffs have shifted into permanent job losses, that could prompt more interest rate cuts than our current assumption for two 25 bps cuts (September and December Fed meetings) this year.

Week ahead data watch

We look for Canadian employment to edge up 10k in August after two consecutive small declines in June and July. But with the population still growing rapidly, and a large pullback in the labour force participation rate in July is not likely to be repeated, we look for job growth to be outpaced by labour force growth and for the unemployment rate to rise to 6.6%.

We expect the July Canadian trade surplus to increase to $2.0B in July, with exports expanding by 1.3% and imports down by 0.8%. Much of the export growth is expected to have come from higher motor vehicle shipments (4%), and higher oil prices boosting the energy trade balance.

U.S. trade deficits likely widened to $79.1 B in July. According to the advance trade report, goods deficits widened by $6.1B from June to July, given imports were up 2.3% m/m, and exports of goods came in flat.