{kind=link}

U.S. Highlights

- The July report for the Consumer Price Index showed headline inflation fell below 3% for the first time since March 2021.

- U.S. retail sales surpassed expectations in July, rising 1.0% month-on-month.

- Federal Reserve Chair Jerome Powell’s remarks during next week’s Jackson Hole Symposium will headline the week.

Canadian Highlights

- Bad news for Canada’s international trade this week, as the U.S. hiked softwood lumber duties and Canada’s two major rail lines halted shipments of certain goods ahead of a potential lockout.

- Housing activity took a breather in July after a strong showing in June. Still, the soft patch will likely prove to be temporary amid falling interest rates and a resilient economy.

- The marquee event on next week’s data calendar is the July inflation report. We expect core inflation to have eased, leaving the door wide open for a September rate cut.

U.S. – Inching Towards a Pivot

A relative state of calm presided over financial markets this week as incoming economic data continued to support the case for the first Federal Reserve rate cut in September. Inflation data for July showed that the annual change in prices fell below 3% for the first time since March 2021, while retail sales for the month came in above expectations. In response, equity markets rose on the week with the S&P 500 up 3.7% as of the time of writing, while U.S. Treasury yields steadied with the two-year yield roughly unchanged at 4.08%.

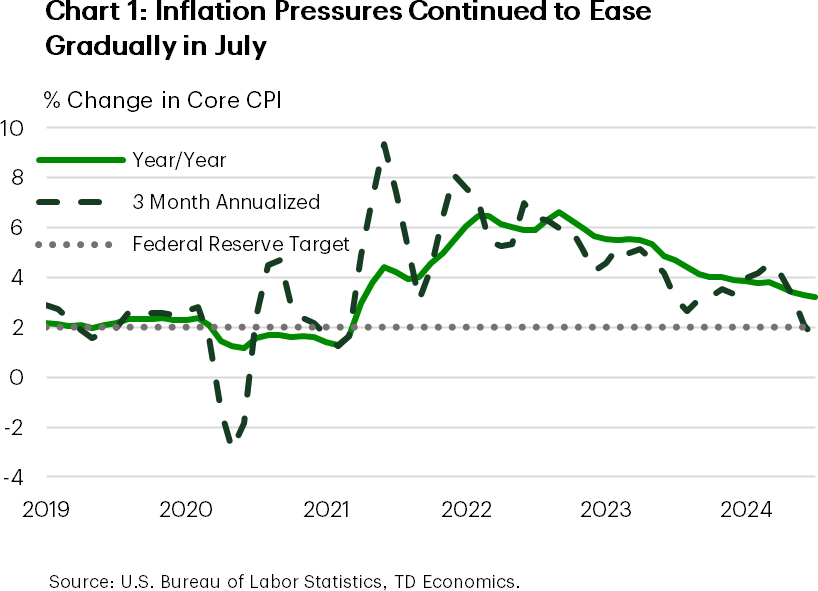

The Consumer Price Index (CPI) report for July showed that inflation picked up slightly relative to June in monthly terms, primarily driven by an uptick in shelter costs. However, the monthly increase in headline and core inflation was still below the level consistent with the Federal Reserve’s 2% target. As a result, the 3-month annualized percentage change in core CPI fell to its lowest level since early 2021 (Chart 1). While the Fed’s preferred inflation metric, core PCE, sat at 2.6% in June, momentum in CPI inflation continues to indicate that inflation pressures will likely ease further moving forward.

This was also evidenced by the Producer Price Index (PPI) report released this week, which showed that upstream production costs decelerated in July. Annual growth in producer prices had been rising through the first half of the year, which contributed to the slowing in the disinflation progress as these costs were likely passed on to consumers. Therefore, the reversal in this trend in July, especially if sustained, would likely provide further relief to consumer price growth moving forward. Taken together the trends in the July reports for PPI and CPI inflation support the case for the Federal Reserve to begin to gradually reduce interest rates at their next meeting in September.

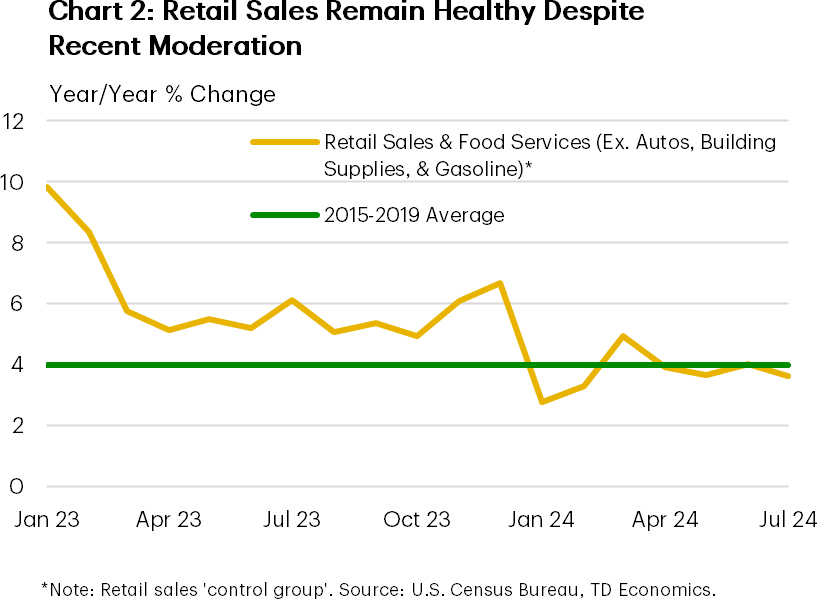

Fortunately, the moderation in price growth seen recently has not required a decline in consumer demand. As indicated by July retail sales, spending rose more than expected to start the second half of the year. This was in part driven by a rebound in auto sales after a cyber attack against a dealership software firm depressed sales in June. Still, sales in the ‘control group’, which excludes the more volatile spending categories, remained healthy in July (Chart 2). The economy has exited a period of exceptionally strong demand and maintained stable momentum, but the Federal Reserve will be cognizant of the balance of risks moving forward.

In the leadup to the Federal Reserve’s annual Jackson Hole Symposium next week, the slate of Fed speakers was relatively light this week. Governor Bowman, who is the only voting member of the FOMC who spoke this week, noted that upside risks to inflation remain and that caution would be warranted in considering future policy adjustments. Fed Presidents Bostic (Atlanta) and Musalem (St. Louis) broadly echoed these concerns, although both noted that interest rates would likely be lower in the second half of the year. Financial markets pared back their expectations for an outsized 50 basis-point (bps) cut in September this week, converging closer to our expectation for a 25bps cut, while they await further guidance from Chair Powell’s remarks scheduled for next Friday.

Canada – Housing Data Caps Eventful Week

This week’s data calendar was somewhat limited, but bad news for Canada on softwood lumber and rail shipments is likely to impact the international trade picture. Financial markets largely took their cues from developments south of the border, as a pair of generally soft U.S. inflation reports reinforced that Fed rate cuts were coming. This sentiment kept yields lower in the U.S. and Canada. Meanwhile, solid U.S. retail spending and labour market data injected some optimism about the economy, lifting equities in both countries.

Softwood lumber was back in the headlines. In the latest salvo in a longstanding dispute, the United States hiked its duty on Canadian softwood lumber entering its borders to 14.54% from 8.05%. This change will mark the first increase in some time, although is unlikely to meaningfully swing the overall export outlook given that lumber accounts for less than 2% of total Canadian international merchandise exports. Still, B.C. and New Brunswick (where lumber makes up a higher share of total exports) will feel an outsized impact. It’s also worth noting that that lumber shipments plunged in the wake of the 2017 Trump tariffs on softwood lumber, and volumes have yet to re-gain this lost ground.

Elsewhere, Canada’s two main railways began halting shipments of certain goods this week ahead of a potential lockout of over 9k engineers, conductors, and yard workers on August 22nd. There is still time to strike a deal, although a work stoppage wouldn’t be unfamiliar terrain, as there have been several in the past. A few common threads emerge when these periods are examined: GDP gets directly impacted by a decline in rail transportation, which is quickly recouped when the stoppage ends. Industries like manufacturing and agriculture feel an impact given these goods get shipped on rail lines, and the federal government can and will step in to legislate parties back to work.

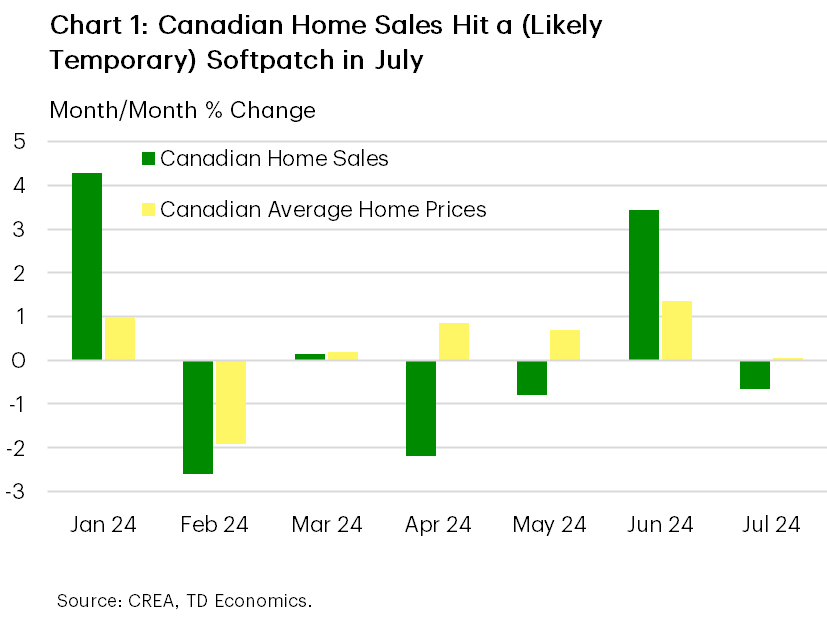

This week also offered a glimpse on how housing markets performed in July. As it turns out, last month was fairly subdued for resale activity, with sales dipping month-on-month and prices flat (Chart 1). This is despite another Bank of Canada rate cut in July, and a significant drop in bond yields during the month. Of course, even with these declines, interest rates were hovering around multi-year highs. Notably, July’s sales decline only gave back a small portion of June’s hefty gain, and nowhere is it said that home sales had to go up in a straight line after rates began dropping. We view July’s soft patch for housing as temporary, with firm gains in home sales and prices likely in the second half.

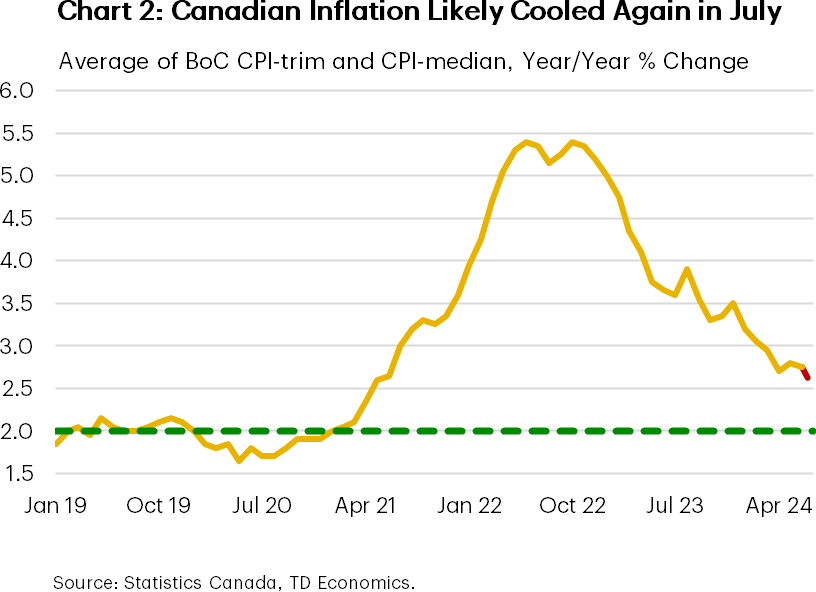

Next week’s data slate will be highlighted by the July inflation (CPI) report (Chart 2). We expect it will show continued progress towards the Bank of Canada’s 2% inflation target. Both headline and the average of the Bank’s preferred core measures could tick lower to around 2.5%, marking the softest reading since 2021. This would leave the door wide open for another Bank of Canada rate cut on September 4th.