. Consumer price index readings, excluding MIC, have been trending around the 2% inflation target since January.){kind=link}

The easing of Canadian inflation pressures has slowed in recent months. On Tuesday, we expect annual price growth for both the headline and excluding food & energy measures to hold steady at 2.7% and 2.9%, respectively, in July. Shelter inflation still accounts for a disproportionate share of the increase, but that has been slowing with lower interest rates leading to a deceleration in mortgage interest costs (MIC). Consumer price index readings, excluding MIC, have been trending around the 2% inflation target since January.

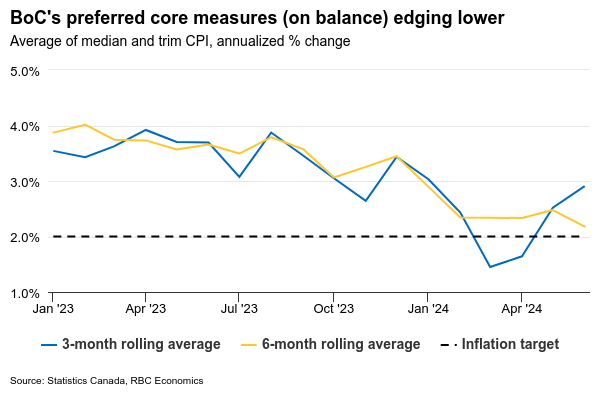

The Bank of Canada is focused on where inflation is going rather than where it has just been. The closely watched three-month rolling average in the BoC’s preferred median and trim core inflation measures (designed to look through monthly volatility and provide a better gauge of underlying price growth trends) likely ticked higher for a second straight month as a meagre monthly increase in April drops out of that calculation. But earlier softer readings mean that annual growth rates in those measures should continue to edge lower. There was concern that initial interest rate cuts from the BoC could reignite rapid house price growth, but the response in housing markets to the 25 basis point cuts in June and July has been muted with signs that rent price growth has also begun to slow.

More importantly, a still weakening economic and labour market backdrop should suggest inflation pressures in Canada will further unwind. Per-capita gross domestic product is continuing to decline in Q2 this year. The unemployment rate is up almost a percentage point from a year ago in July as job openings fall, and wage growth is easing as a result. BoC Governor Tiff Macklem reiterated that confidence has increased that inflation will continue to drift lower even if “there could be setbacks along the way” after cutting rates in July. That means a low hurdle against the BoC cutting rates from levels that are still sharply above what it views as normal in the long run. We think the BoC will cut rates by 25 bps in each of the upcoming meetings in September and October.

Week ahead data watch:

Canadian retail sales likely dropped by 0.3% in June, driven by a price-related sales decline at gas stations. That was partially offset by higher auto sales that edged higher by 0.7% on a seasonally adjusted basis.

A potential rail strike or lockout at both of Canada’s major rail companies could begin as early as August 22 if an agreement isn’t reached with the union. Historically, there have not been disruptions from both major rail companies at the same time. Rail shipping accounts for about 0.5% of GDP. Trucking activity would rise in the event of a strike, but it cannot replace rail shipments, particularly for products like grains. Relatively high levels of inventories in the manufacturing sector could blunt the immediate downstream impact of transportation disruptions, but a shutdown of any significant length (e.g., more than a week) could have a substantial impact on the broader macroeconomy.