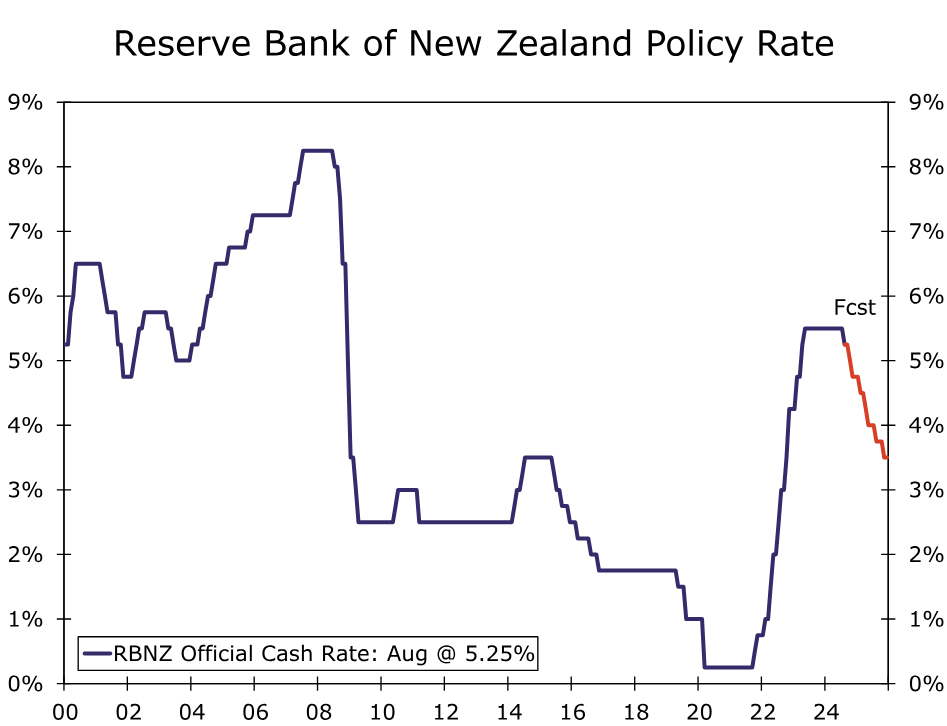

kicked off its rate cut cycle at this week's meeting, lowering its policy interest rate by 25 bps to 5.25%. The decision was a mild surprise, with an overall majority of analysts (including ourselves) expecting the central bank would remain on hold.){kind=link}

Summary

- The Reserve Bank of New Zealand (RBNZ) kicked off its rate cut cycle at this week’s meeting, lowering its policy interest rate by 25 bps to 5.25%. The decision was a mild surprise, with an overall majority of analysts (including ourselves) expecting the central bank would remain on hold.

- Several factors contributed to the pivot to monetary easing. The RBNZ cited slowing inflation and declining inflation expectations. Moreover, weak sentiment surveys and mixed labor market figures suggest spare capacity in the economy is likely to continue building, giving the central bank greater confidence that inflation will return to the target range in a timely fashion.

- In addition to reducing interest rates at this week’s meeting, the RBNZ revised its projection for its policy interest rates to reflecting a faster pace of easing, reaching 3.85% by Q4-2025. Given the central bank’s evident comfort in lowering interest rates this week (ahead of updated inflation figures), we see no significant impediments to further near-term rate cuts. We expect 25 bps rate cuts at each and every meeting through May 2025, as well as 25 bps rate cuts in August and November of next year. That would see the policy rate end 2024 at 4.75%, and end 2025 at 3.50%.

- A weak New Zealand economy and pronounced period of RBNZ monetary easing means we expect the New Zealand dollar to be an underperformer among the G10 currencies over the medium-term. We expect, at best, only modest gains in the NZ currency versus the greenback through the end of 2025.

Reserve Bank of New Zealand Kicks Off Its Rate Cut Cycle

The Reserve Bank of New Zealand (RBNZ) sprung a mild surprise at this week’s monetary policy announcement, delivering a 25 bps policy rate cut to 5.25%. The consensus forecast from analysts had been for the central bank to hold rates steady, although a sizable minority had expected the RBNZ to move at this week’s meeting. The RBNZ’s decision also represents a relative rapid pivot from the central bank—while the RBNZ’s July announcement was reasonably balanced, as recently as May the central bank had delivered a hawkish statement, including an upward revision to it projected policy rate path, suggesting at that time there was still at least some risk the central bank could hike rates further.

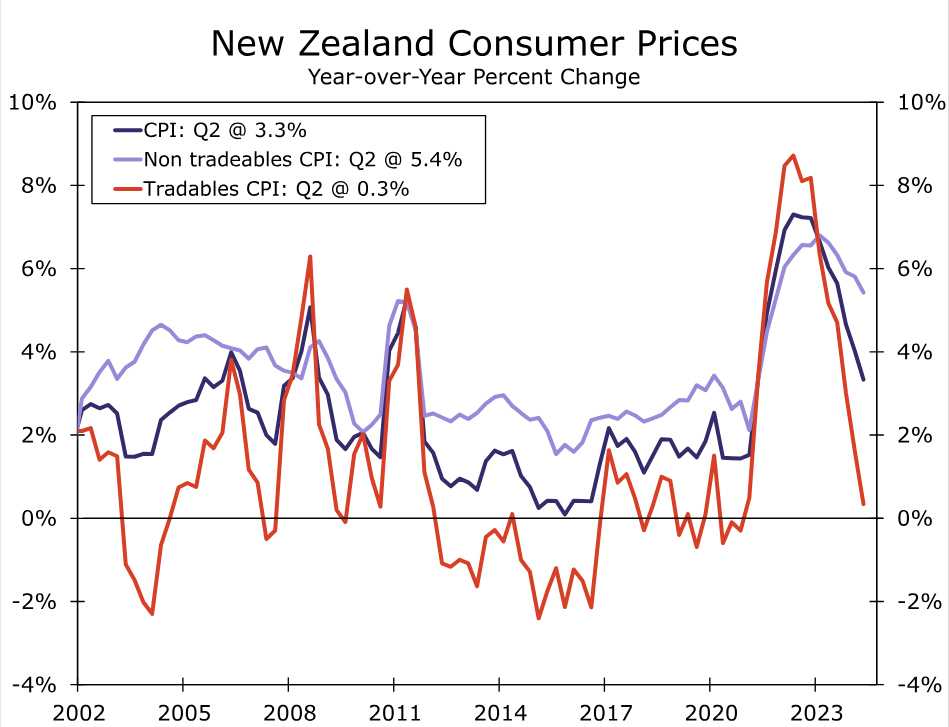

What then has changed between May and August for the RBNZ to lower its policy rate this week? On the price front, Q2 inflation surprised slightly to the downside, slowing to 3.3% year-over-year. To be sure, much of the deceleration was driven by tradables inflation, with non-tradables inflation showing a more gradual deceleration. Importantly, survey-based measures have also shown declining inflation expectations, while the Q2 Quarterly Survey of Business Opinion also showed a net 23% of firms increasing prices during the quarter, down from a net 35% that raised prices in Q1.

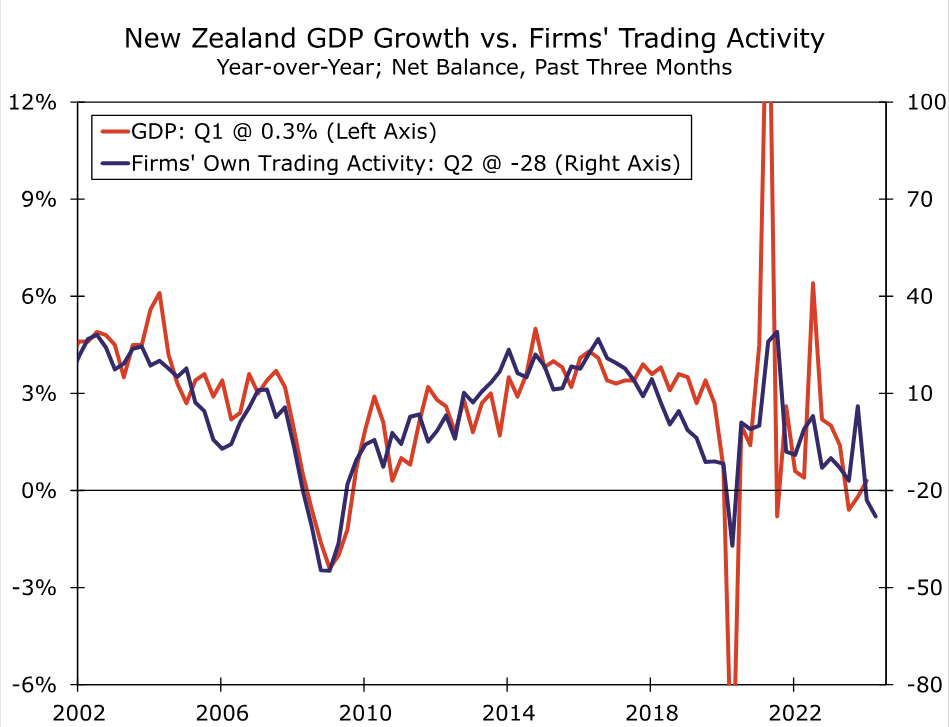

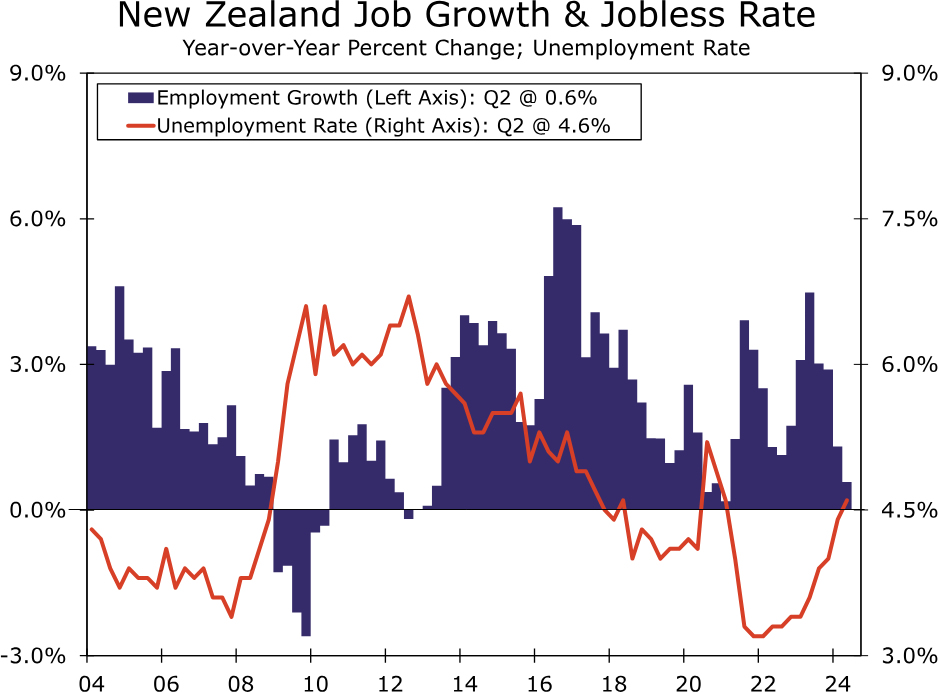

The most recent indicators on economic activity suggest the growth environment remains very weak, supporting the notion that lessening demand and increasing spare capacity should continue to see inflationary pressures abate in the quarters ahead. Although Q1 GDP rose a modest 0.2% quarter-over-quarter, a wide range of survey data point to an underwhelming economy through Q2 and into Q3. The Quarterly Survey of Business Opinion showed an increase in net pessimism to 44% in Q2, from 25% in Q1. Meanwhile, a net 28% of businesses reported a decline in their own trading activity in Q2, compared to a net 23% that reported a decline in Q1. This latter metric is particularly significant, given that firms’ assessment of their own trading activity has often proved to be a reliable indicator of overall GDP growth. Other recent survey data also include a decline in the June manufacturing PMI to 41.1 and a fall in the June services PMI to 40.2. Finally, we interpret the Q2 labor market report as relatively weak overall, including a drop in full-time employment and hours worked, as well as a rise in the unemployment rate.

Against this backdrop, the RBNZ lowered its near-term GDP outlook, and now forecasts negative GDP growth in both Q2 and Q3. The central bank also see a higher peak in the unemployment rate than previously, reaching 5.4% by early next year. It is this larger buildup of spare economic capacity that gives the RBNZ some greater confidence that inflation is heading sustainably towards its inflation target range (indeed, the central bank sees headline inflation slowing sharply to 2.3% year-over-year in Q3-2024).

Overall, the combination of slowing inflation and weak growth saw the RBNZ offer several important perspectives as part of its August monetary policy deliberations:

- The weakening in domestic economic activity has become more pronounced and broad-based, and that a broad range of high-frequency indicators point to a material weakening in domestic economic activity in recent months.

- Signs of slower inflation and reducing inflation expectations, combined with the weaker high-frequency indicators of economic activity, provide more confidence that headline inflation is returning to the target band in the September 2024 quarter.

- The downside risks to output and employment previously highlighted by central bank policymakers have become more apparent.

- Recent indicators give confidence that inflation will return sustainably to target within a reasonable time frame. With headline CPI inflation expected to return to the target band in the September quarter and growing excess capacity expected to support a continued decline in domestic inflation, the Committee agreed there was scope to temper the extent of monetary policy restraint.

Not only did the RBNZ lower interest rates at this week’s meeting, but revised its projections for the policy interest rate path lower, signaling the likelihood of a series of rate cuts in the quarters ahead. The central bank projected an average policy rate of 4.92% for Q4-2024, falling to 3.85% by Q4-2025 and 3.13% by Q4-2026. Given the central bank’s evident comfort in lowering interest rates this week (ahead of the Q3 inflation figures), we see no significant impediments to further near-term rate cuts, and now forecast 25 bps rate cuts at the October and November meetings. Beyond that the cadence of RBNZ’s easing (either a pause, or a step up to 50 bps increments) will likely depend on the degree of progress of disinflation. So long as inflation trends continue to moderate, our base case is also for 25 bps rate reductions in February, April and May next year. By the second half of next year and as the central bank moves closer to a more neutral policy interest rate, we expect a more gradual quarterly frequency of policy moves and anticipate rate cuts at the August and November 2025 meetings, which would see the RBNZ’s policy rate end next year at 3.50%. A weak New Zealand economy and pronounced period of RBNZ monetary easing means we expect the New Zealand dollar to be an underperformer among the G10 currencies over the medium-term. We expect, at best, only modest gains in the NZ currency versus the greenback through the end of 2025.