{kind=link}

Markets

Markets rallied in the wake of yesterday’s benign July producer price inflation (0.1% M/M for headline and 0% for core). Stock markets extended their comeback after last Monday’s melt down with key US gauges adding 1% (Dow) to 2.4% (Nasdaq). US Treasuries rallied as well, with investors piling up on bets that the Fed will start its cutting cycle with a 50 bps rate cut rather than a 25 bps move. A cumulative 100 bps of rate cuts is discounted at the US central banks’ remaining three policy meetings this year. Though we don’t fight current sentiment, it’s fair to say that no Fed governor talked about a potential 50 bps move so far. On the contrary. Atlanta Fed Bostic (voter) yesterday indicated that he’s looking for a little more data before supporting a rate cut. For now, he sticks with his timing of a first move only by year-end. “We want to be absolutely sure. It would be really bad if we started cutting rates and then had to turn around and raise them again.” He adds that he is definitely concerned by the rise joblessness but points out that it is more due to a larger supply of workers rather than a slump in demand. Markets ignored the Bostic comments. The PPI rally eventually pushed US yields 4.2 bps (30-yr) to 8.7 bps (2-yr) lower. German Bund yields lost 3.2 bps (30-yr) to 5.2 bps (2-yr). EUR/USD in first instance dipped from 1.0940 to 1.0920 on a very weak German ZEW investor survey before the pair rebounded to just below 1.10 driven by USD weakness. Today risks becoming a repeat of yesterday as US July consumer prices line up. Consensus expects 0.2% M/M increases for both headline and core CPI gauges with the Y/Y print stabilizing at 3% and dipping from 3.3% to 3.2% respectively. Yesterday’s solid UK labour market update is followed by lower than expected July inflation figures. Headline CPI fell by 0.2% M/M (vs -0.1% M/M) with the annual figure rising to 2.2% from 2% (vs 2.3% forecast). Core CPI slowed to 0.1% M/M and 3.3% Y/Y (from 3.5% Y/Y). The more benign inflation print suggests the BoE’s close call to cut its policy rate by 25 bps early August was the right one with follow-up action becoming very likely. EUR/GBP spikes from 0.8540 to 0.8570.

News & Views

The Reserve Bank of New Zealand lowered its policy rate by 25 bps to 5.25%. It was the first cut since hitting the 5.5% peak rate in May of last year. Markets were split in the run-up to the meeting, attaching a 1/3 probability to an unchanged policy rate scenario. Updated projections show a clear intentions to trim the policy rate further this year, unlike previous May projections which hinted at a potential final rate hike. The OCR rate is set to average 4.92% in Q4 2024 (from 5.65%), 3.85% in Q4 2025 (from 5.14%) and 3.13% in Q4 2026 (from 3.7%). The RBNZ continues to see a 3% policy rate at the end of the forecasting horizon. In its policy statement, the MPC for the first time indicates that annual CPI is returning to within the 1%-3% target band. Surveyed inflation expectations, firms’ pricing behavior, headline inflation, and a variety of core inflation measures are moving consistent with low and stable inflation. Services inflation remains elevated but is also expected to continue to decline, both at home and abroad, in line with increased spare economic capacity. Updated annual CPI forecasts show a 2.3%-2.3%-2% path for the 2024-2026 period from 2.9%-2.2%-2% in May. In the meantime, economic growth remains below trend with a broad range of indicators suggesting that the economy is contracting faster than anticipated. On top, further downside risks to output and employment have become more apparent. At the press conference, RBNZ governor Orr indicated that the MPC contemplated to option of a 50 bps rate cut but eventually settled on a low-risk start to the easing cycle as they feel in a strong position to move calmly. NZD swap rates dropped by 5 bps (30-yr) to 11 bps (2-yr) after the decision with NZD money markets discounting a cumulative 75 bps of additional policy rate cuts at this year’s remaining two meetings. The kiwi dollar reversed yesterday’s gains, dropping back from 0.6080 to 0.60.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU data rolled in, dragging the long end of the curve down. After breaking below 2.34%-2.4% eyes now turn to 2.12-2.16%.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is continuing to move better in to balance. There was no pushback against market pricing back then (75 bps cuts in 2024, 100 bps in 2025). The pivot weakened the technical picture in US yields with another batch of weak eco data pushing the 10-yr sub 4%.

EUR/USD

EUR/USD tested the topside of the 1.06-1.09 range as the dollar lost interest rate support at stealth pace. A September rate cut is highly likely and markets increase bets on future easing on incoming weak US data. The risk-off these data trigger (sharper than expected slowdown?) offset the interest rate losses for USD. EUR/USD is moving south within the 1.07-1.09 range.

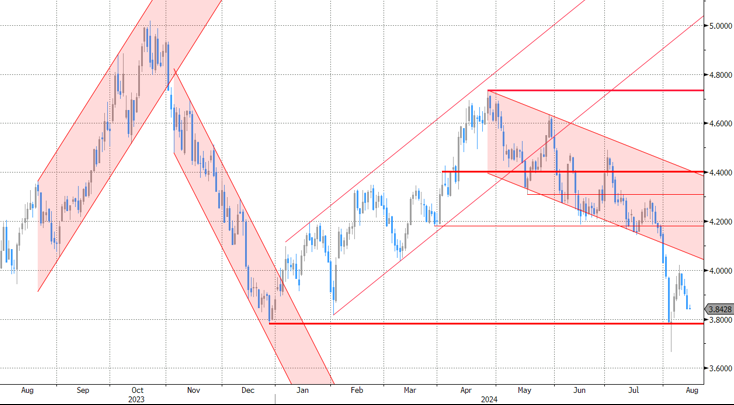

EUR/GBP

The Bank of England delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually and on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Risk-off proved a more important driver of GBP recently. We may see a return to the 0.85-0.86 sideways trading range that dominated 2024H1.