{kind=link}

- The RBNZ cut the OCR to 5.25% at its August policy meeting by unanimous decision.

- We think the RBNZ only seriously considered the option of cutting the OCR by 25bps at this point. The Governor noted that there are further meetings this year where further adjustments can be made.

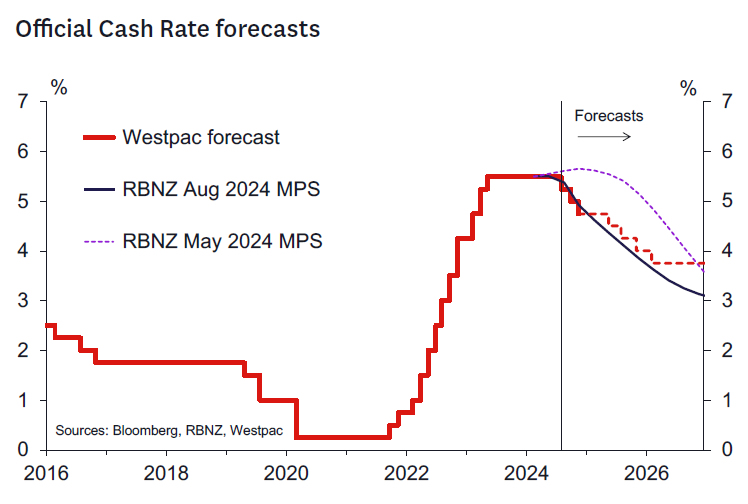

- The revised projections lowered the OCR track significantly. The track implies that the next easing will occur at the October Monetary Policy Review, and a total of 75bp of cuts are forecast by end 2024.

- The track implies the RBNZ’s monetary policy strategy is to more quickly ease policy over the next 6-12 months. The RBNZ aims to reach neutral OCR levels of around 3% by 2027 as previously expected – but reaches there more quickly.

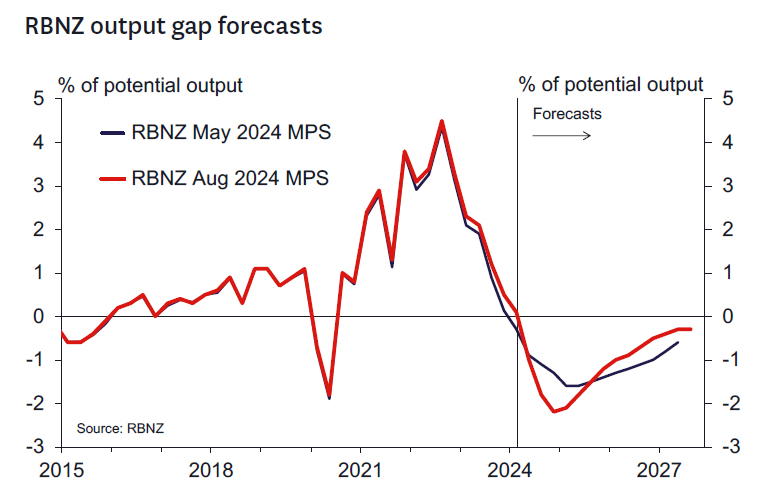

- The RBNZ’s near-term forecasts for economic growth have been revised down significantly. A wider output gap and looser labour market gives them confidence that inflation will ultimately fall.

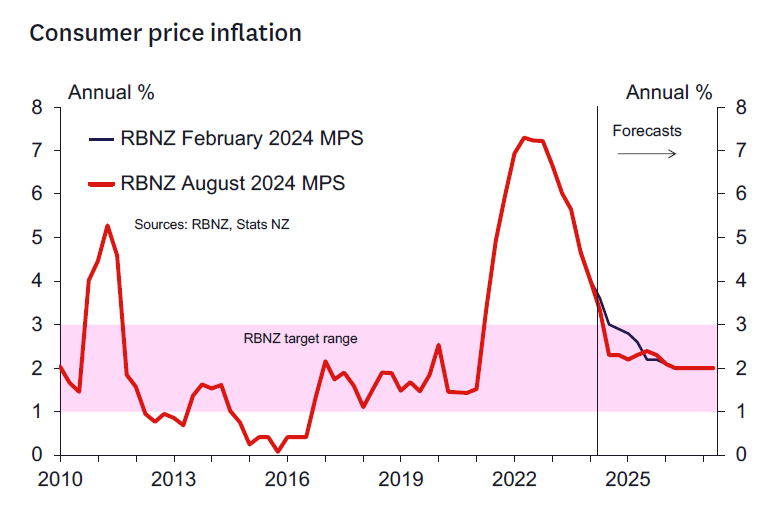

- Inflation is forecast to fall back inside the 1-3% band in the September quarter of this year and is still not projected to return to 2% until Q2 2026.

- The RBNZ assesses the risk profile for inflation as balanced – and now two sided. We think the risk profile is decidedly to the upside for non-tradables inflation pressures.

- Today’s RBNZ update leaves us comfortable with our forecast of two further 25bp cuts in October and November. We will review our forecasts beyond then in coming days.

Key take out: OCR cut 25bps and further easing seems likely this year

The RBNZ unexpectedly cut the OCR to 5.25%. The decision to cut by 25bps today was reached by consensus and so no vote was taken.

As widely expected, the RBNZ’s projected track for the OCR was revised significantly lower from that seen in the May MPS.

- The projected average OCR in Q4 this year was revised down 73bps to 4.92%, at face value implying three 25bps rate cuts by the end of this year.

- The projected OCR for Q4 2025 was revised down 129bps to 3.85%, implying a further around 100 bps of rate cuts next year.

- The forecast for Q4 2026 was revised down 57bps to 3.12%, implying around three 25bps cuts in that year.

- The RBNZ assumes the OCR reaches around 3% in Q3 2027 (the final quarter of the forecast).

According to the RBNZ, the most important driver of the revised view were a significant downgrade in the near-term growth outlook (as we had foreshadowed in our recent Economic Overview). This weaker growth profile and resultant weaker output gap has increased the MPC’s confidence that inflation will continue to fall to the mid-point of the 1-3% target range over a similar timeframe as previously expected. Indications of weaker price intentions and inflation expectations have further buttressed the RBNZ’s confidence that domestic inflation pressures will ultimately normalize.

Risks

We think the RBNZ’s revised growth forecasts are well balanced in the short term. The RBNZ has included a relatively firm bounce back in the economy over 2025 compared to our forecasts. Having said that, the much easier interest rate profile compared to our more conservative OCR forecast assumptions explains some of that relative optimism. Interestingly, the RBNZ does not see the front-loaded easing profile impacting on house prices significantly in the next year. There could be some upside risks there in coming quarters given the generally strong inverse relationship between interest rates and house prices.

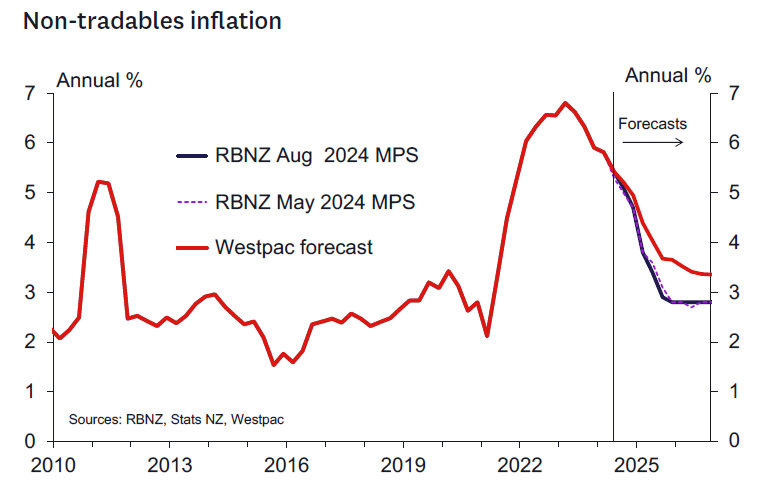

The risks around their short-term inflation projections also look well balanced, although from early 2025 the RBNZ has an optimistic view on how quickly non-tradable inflation will fall. We are not so sure about that, and it will be up to the data to confirm this is going to occur.

Westpac’s OCR call

We remain comfortable with the previous forecast of two further 25 bp cuts to the OCR over the balance of the year (from the lower 5.25% starting point). Hence, we expect the OCR to end 2024 at 4.75%. Beyond that we will make a full assessment in coming days.

CPI inflation to fall below 3% sooner than expected

Underlying the downward revision to the RBNZ’s interest rate projection is a better contained outlook for inflation. Inflation surprised the RBNZ to the downside in the June quarter and it’s now expected to fall below 3% in the September quarter. That’s sooner than the RBNZ had assumed in May, and in line with our own forecasts for inflation over the remainder of this year.

Further ahead, the RBNZ is sounding increasingly confident that inflation will settle close to the 2% midpoint of their target band (though this still isn’t expected to be reached until mid-2026). We’re also expecting to see inflation trending back towards 2%. However, there are some key areas where we think the RBNZ might be surprised.

First, and most importantly, is the ‘stickiness’ in domestic inflation. The RBNZ expects that domestic inflation will drop back sharply over 2025 as capacity pressures ease. They’ve also allowed for a faster easing in price setting behaviour (i.e. inflation expectations) and more moderate increases in the prices for items like insurance. We’re less optimistic about how quickly domestic inflation will ease and expect that it will continue to surprise the RBNZ to the upside (as it has done over the past year).

Balanced against that risk of persistent domestic inflation, imported inflation (i.e. tradables) has fallen well short of the RBNZ’s forecasts. The RBNZ is projecting a reacceleration in imported inflation next year after some sharp falls recently. In contrast, we expect that it will remain soft for some time. That will help to keep overall inflation and inflation expectations contained.

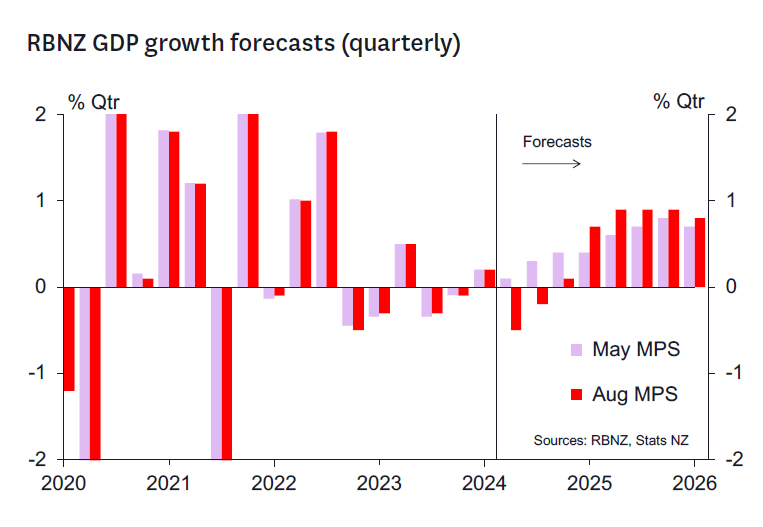

Near-term GDP growth forecasts revised down

A key driver of today’s decision was a sharply downgraded view of the near-term outlook for activity, with crucial implications for the labour market (see below) and the output gap. Indeed, the RBNZ’s forecasts for GDP growth in Q2 and Q3 were revised down by a cumulative 1.1ppts and at -0.5%q/q and -0.2%q/q respectively are nearly identical to the estimates that we included in our recent updated Economic Overview. As a result, while the RBNZ has again revised down its estimate of the economy’s potential growth rate, the RBNZ now expects the output gap to turn more negative over the coming year, troughing at -2.2% of GDP in Q4 this year, rather than a trough of -1.6% of GDP in Q1 next year.

Given the much easier monetary conditions included in these projections, the RBNZ’s forecasts also build in a much stronger cyclical rebound in activity next year. Indeed, the RBNZ now expects GDP to grow 3.3% over the 2025 calendar year up from 2.4% in the May MPS. As a result, the output gap is expected to shrink to -1.2% of GDP by the end of next year, which is slightly smaller than the -1.4% of GDP output gap projected in the May MPS. It is worth noting that this rebound is quite a bit stronger than forecast in our recent Economic Overview, albeit with our forecasts based on firmer monetary conditions than implied by the RBNZ’s revised projections.

The RBNZ’s labour market view

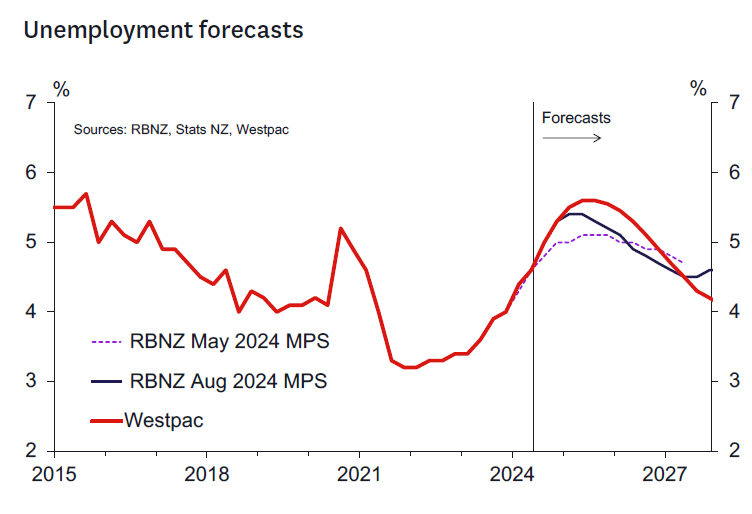

The RBNZ acknowledged the softening in the labour market, particularly in the near term – the sharp slowdown in job vacancies and the fall in filled jobs in the last few months were among the high-frequency activity indicators that the RBNZ highlighted in its Statement. They expect the unemployment rate to rise further in the coming quarters, reaching a peak of 5.4% in early 2025. That’s higher than their previous forecast of a 5.1% peak, though it’s within the range of forecasts that the RBNZ has produced over the last couple of years. Along with that increasing slack in the labour market, the RBNZ expects a faster moderation in wage growth.

RBNZ takes relatively sanguine view on impact of Budget 2024

The August MPS is the first to be released since Budget 2024 was unveiled in late May, and so the first to fully incorporate an estimate of the full impact of the new Government’s policies. The RBNZ’s view on the impact of fiscal policy is set out on Box B of the MPS. The RBNZ notes that spending reductions in the public sector will reduce inflationary pressure, and income tax threshold changes will increase inflationary pressure. A fiscal multiplier of 0.5 is assumed to apply to both spending reductions and tax revenue reductions – in line with estimates derived from past research in New Zealand, but this assumption is recognised as a source of uncertainty. The RBNZ also noted that tax cuts can also increase labour supply and affect wage bargaining, which may partially offset the inflationary pressure from higher spending.

Given that the May MPS had already implicitly accounted for a share of the lower government spending, the RBNZ’s updated assumptions about fiscal policy have added slightly to medium-term inflationary pressure. However, those effects have clearly been swamped by other economic developments. Overall, the RBNZ concluded that the net impact for monetary policy is expected to be small and is highly uncertain. Over coming months, the RBNZ will refine its estimates in light of the emerging data.

Key domestic data to watch ahead of the RBNZ’s October Review

The next RBNZ policy review will take place on 9 October. In addition to any important economic or financial developments offshore, there are several domestic economic data releases that will have a significant bearing on the outcome of that meeting. The most important are:

- The Q2 GDP report (19 September): The outcome of this report will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap and perhaps also its view on near-term growth momentum.

- The Q3 QSBO survey (1 October): The focus will be on indicators of spare capacity and cost/ inflation pressures. It will also be interesting to see if confidence, hiring and investment indicators are lifting from low levels as monetary conditions ease.

- Selected price indexes for July/August (15 August/12 September): These indexes will cast light on some of the most volatile components of the CPI and thus on the certainty that the Q3 CPI (16 October) will show inflation back inside the 1-3% target band.

- Employment indicators for July/August (28 August/30 September): Developments in the labour market will remain a key focus for the RBNZ and these indicators will provide insight into the likely outcome of the Q3 labour surveys (released 6 November).

- The August Electronic Card Transactions report (12 September): This release will capture the first month of retail spending since the personal tax cuts took effect.

In addition to the above, key monthly activity indicators such as the Business NZ manufacturing and services indexes and the ANZ Business Outlook survey will also be of interest.