moving forward. On the press conference following the meeting, Governor Ueda had turned much more hawkish and the building of an economic momentum fostering 2% selfsustained inflation no longer seems to be the only thing that matters. Instead, the yen has taken centre stage. Earlier, FX moves was just one of many parameters, the BoJ monitored when gauging inflation momentum and it was never the key factor. An obvious example of this was the Friday 26 April policy meeting, when a dovish governor Ueda did not pay much attention to a very weak yen. As a result, USD/JPY tested 160 the following Monday and the Ministry of Finance ordered the BoJ to step in to prop up the yen. Now Ueda says, "FX moves are more likely to affect inflation than before". So why this turnaround? The BoJ has intervened for USD161 billion since they stepped in for the first time in September 2022. It is a costly affair to defend the yen and intervention was probably never meant to be a long-term solution.){kind=link}

- The BoJ has taken up a much more aggressive strategy and we no longer expect them to wait for all the pieces to fall in place before tightening policies further.

- We expect the BoJ will hike its policy rate to 1% within the coming 12 months.

The rate hike on 31 July was pivotal for how we see the Bank of Japan (BoJ) moving forward. On the press conference following the meeting, Governor Ueda had turned much more hawkish and the building of an economic momentum fostering 2% selfsustained inflation no longer seems to be the only thing that matters. Instead, the yen has taken centre stage. Earlier, FX moves was just one of many parameters, the BoJ monitored when gauging inflation momentum and it was never the key factor. An obvious example of this was the Friday 26 April policy meeting, when a dovish governor Ueda did not pay much attention to a very weak yen. As a result, USD/JPY tested 160 the following Monday and the Ministry of Finance ordered the BoJ to step in to prop up the yen. Now Ueda says, “FX moves are more likely to affect inflation than before”. So why this turnaround? The BoJ has intervened for USD161 billion since they stepped in for the first time in September 2022. It is a costly affair to defend the yen and intervention was probably never meant to be a long-term solution.

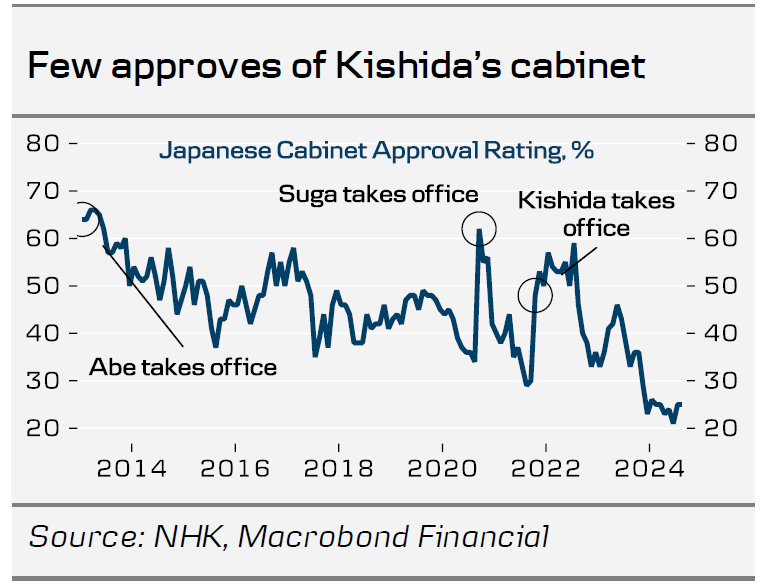

The hawkish turnaround should perhaps also be viewed in the light of a very low approval rating for PM Kishida and his cabinet. Just 25% approved in August, below the so-called danger level of 30%, an uncomfortable situation for Kishida considering recent history and the upcoming Liberal Democratic Party leadership election in September. Excluding Shinzo Abe’s eight-year reign from 2012-2020, the last seven prime ministers have only had about one year in power.

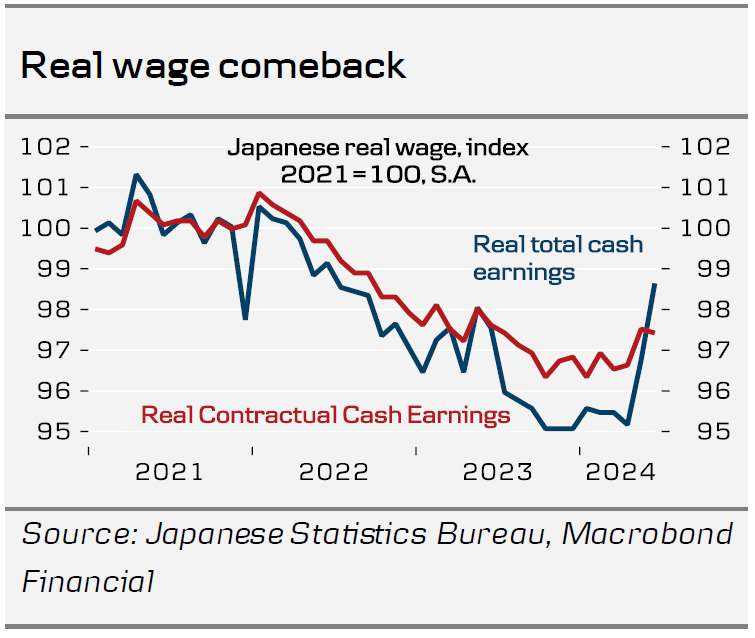

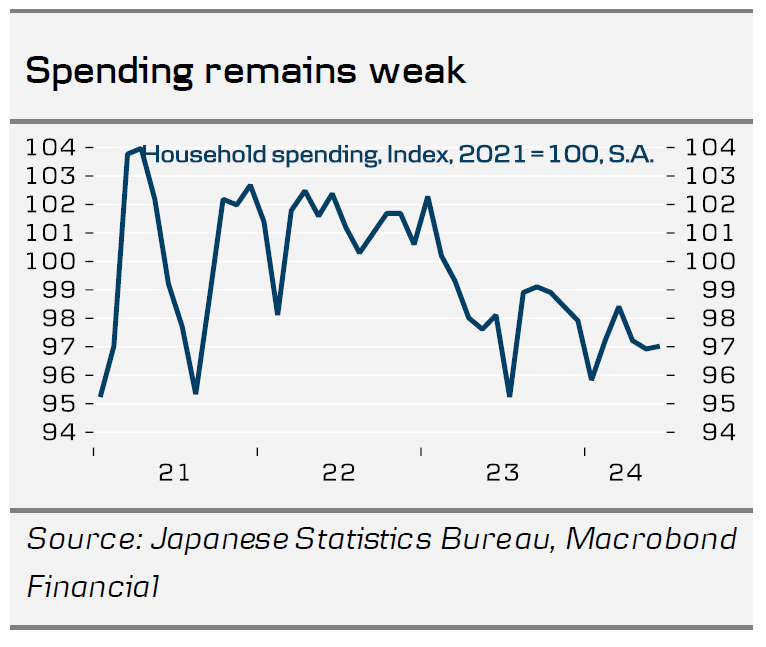

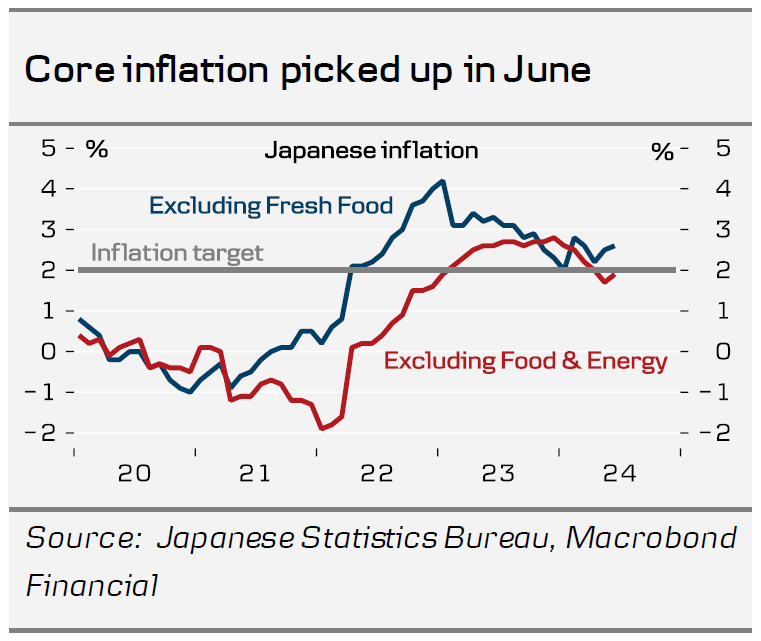

A very weak currency is usually not popular with the public and in Japan it creates quite visible inflation due to the status as a major energy importer. Gasoline for instance costs JPY175 per litre now, which is about JPY25-30 more than pre-pandemic levels. That is a big price increase in 4-5 years. Back in May, a poll from the private think tank, Teikoku Databank, showed 64% of companies see the weak yen as having a negative impact on their profits. Afterall, most Japanese companies are not in a position to exploit the advantages of a weak currency on export markets but only experience the flip side, which is higher import costs. About half of the respondents saw USD/JPY at 110-120 as an appropriate level. Largely, a weak currency benefits major exporters at the expense of consumers. That process can create inflation but will be painful for consumers until business profits are passed on to employees. We have seen the beginning of that process with the spring wage increases and real earnings recovered most of the lost purchasing power from 2021, in Q2. A lot of the June pay increases are one-off payments, though, and growth in real contractual cash earnings remains modest. The reality for most consumers is still that much of their purchasing power has been eroded and that is also key to understand why real household spending was still down 1.4% yoy in June.

If the long-term goal to sustainably reach the inflation target was the only game in town, we think this would bode for a cautious approach, and hiking rates again only when private spending shows signs of picking up. It seems, however, that the BoJ has come under pressure to incorporate the yen more explicitly in its policy decisions. Even if household spending shows only modest improvement, we expect the BoJ to hike by another 25 bps this year followed by another 25bps in Q1 and Q2. Given the recent global, and particularly Japanese, market turbulence, we expect the BoJ will be a bit more cautious at the fall policy meetings, though. This is based on our expectation that investors’ Fed pricing is too aggressive and US treasury yields will trade higher again, adding some renewed headwinds for the yen.

US outlook remains key for the yen

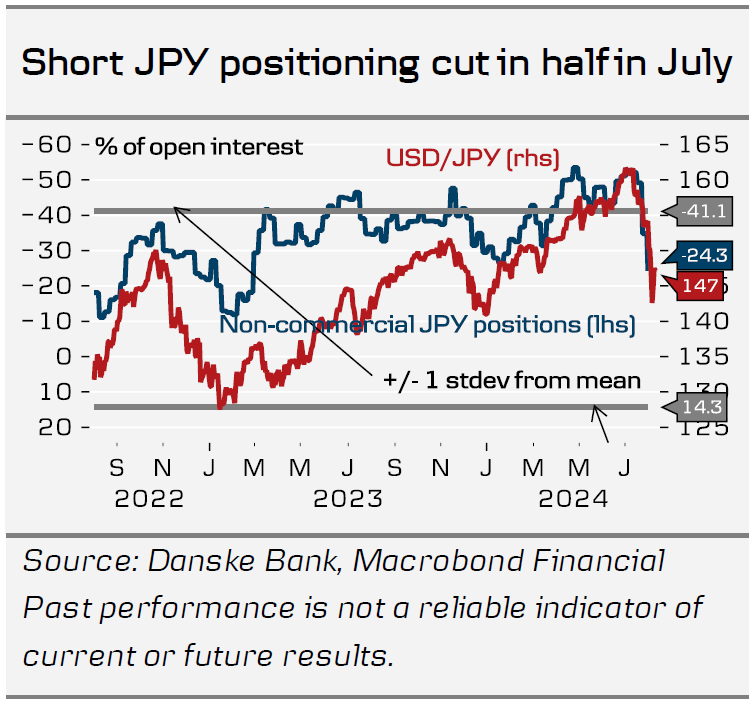

As mentioned above, USD/JPY has experienced some extreme swings over the summer, resulting in notable JPY appreciation. Since 1 July, the JPY has strengthened by around 10% against the USD, pushing USD/JPY below 150. Several factors have supported the Japanese currency, including a massive unwinding of carry trades, lower US rates, declining oil prices, more strategic Japanese FX intervention, and a hawkish hike from the BoJ. The prospect of narrowing rate differentials between Japan and other G10 economies is currently a significant tailwind for the JPY, making it the clear outperformer in the G10 space. It seems that global factors have a greater influence on the JPY than domestic developments in Japan. Consequently, whether the BoJ hikes 1-3 more times over the coming year may not impact USD/JPY as much as changes in US yields or oil prices. We believe there is further room for decline in USD/JPY over the strategic horizon and remain bearish on the cross. If we are heading for more volatile times, the carry trade will lose its attractiveness, as evidenced by the halving of short JPY positions in July. Additionally, the tail risk of a US recession, which could force the Fed to lower rates quickly and aggressively, might prompt USD/JPY to decline sharply, even if the BoJ stops further hikes. However, in the near term, with the recent strong rally, we could see a temporary reversal as we expect the dovish repricing of the Fed to reverse. With USD/JPY having already dipped to 141.70 last week before bouncing back above 145.00, we suspect the market will remain in “sell rallies” mode if there is a significant bounce, even if risk assets manage to sustain a rebound. Overall, we see USD/JPY declining below 145 on a 12-month horizon.