{kind=link}

- US equities rebounded from a selloff earlier in the week, ending slightly higher. However, caution remains due to upcoming economic data releases.

- The Japanese Yen is heading for its first losing week in six, impacted by a peak in short-position unwinding and dovish BoJ comments.

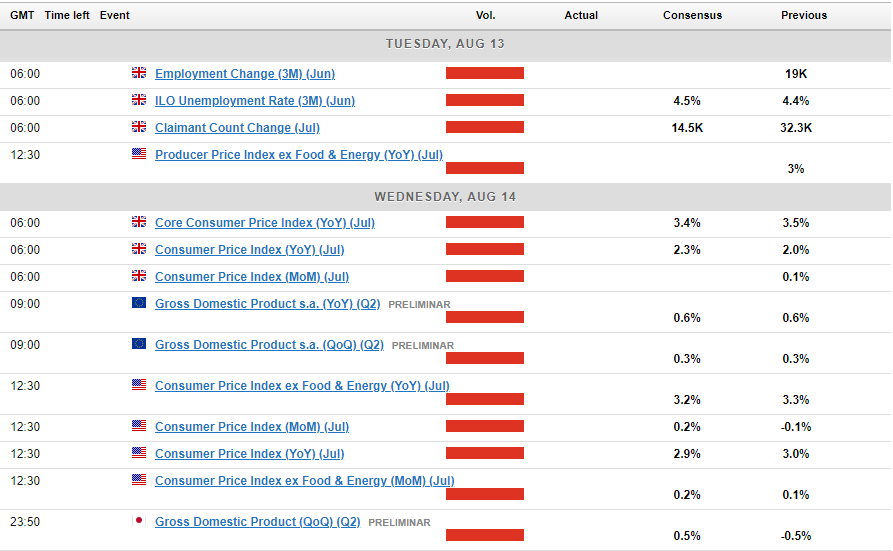

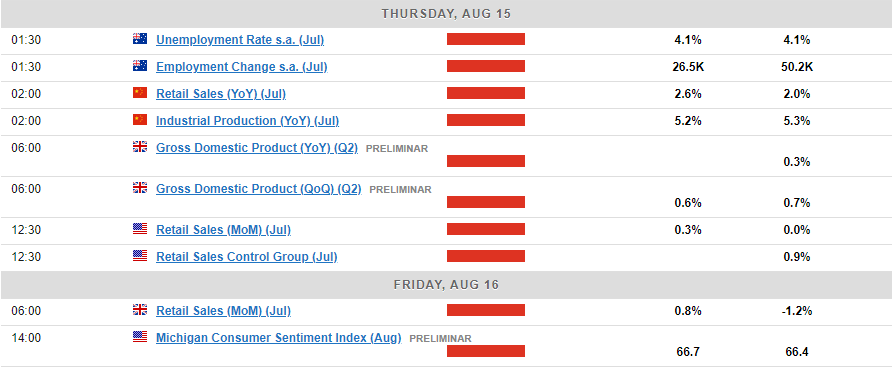

- The upcoming week features significant data releases, including US and UK inflation, Chinese economic figures, and the RBNZ interest rate decision. Markets are cautious due to recessionary fears and concerns about China’s economic recovery.

Week in Review: Tumultuous Week Comes to an End

A tumultuous week for markets is set to end on a positive note. US equities have bounced back from an early-week selloff and are trading slightly higher for the week as of now. However, traders are exercising caution with a slew of high-impact economic data releases on the horizon.

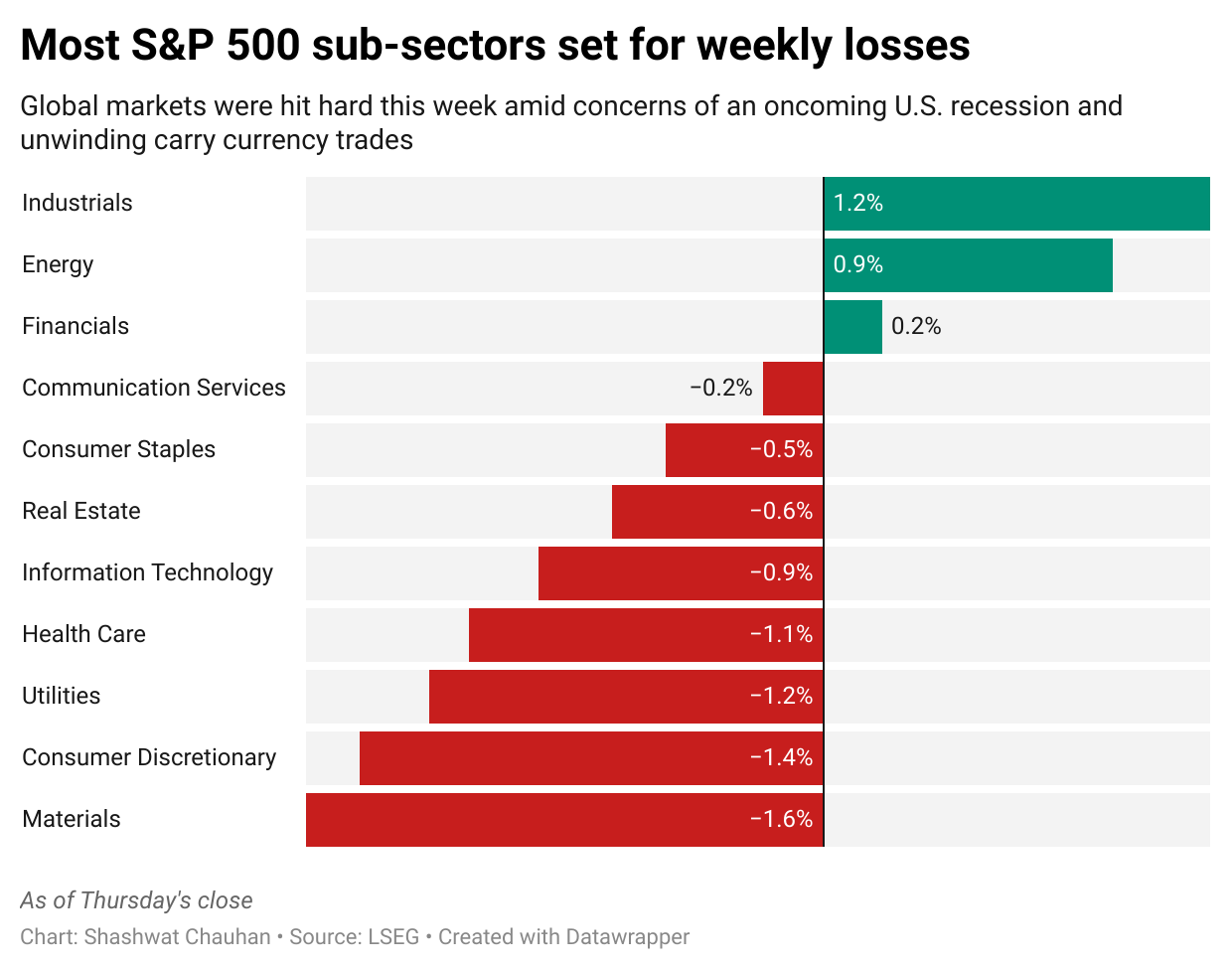

Although US indices have recovered, several sub-sectors within the S&P 500 are still poised for a weekly loss.

Source: LSEG

In the commodities sector, gold seems poised to end the week in the red but showed strong recovery towards the end of the week. Conversely, oil prices have had an impressive week, up 2.7% at the time of writing.

OPEC+ comments this week suggested that the group might postpone their planned October production increase if market conditions remain unstable. This news likely contributed to oil’s gains this week after four consecutive weeks of losses.

On the FX front, the Dollar Index is slightly down for the week at the time of writing. A robust recovery in the US Dollar during the latter part of the week wiped out gains seen by some of its G7 counterparts.

The Japanese Yen continues to be a point of interest and is on track for its first losing week in six. The unwinding of short positions seemed to peak on Monday, dragging USD/JPY to a low of 141.67. However, as sentiment improved and the unwinding phase concluded, the yen struggled to gain traction for the rest of the week.

This coupled with some dovish testimony from BoJ officials weighed further on the Japanese Yen.

The Week Ahead: Data Heavy Week to Test Markets

The upcoming week promises to be blockbuster with a host of high impact data releases. We have the US and UK inflation data prints coupled with data out of China and Japan. Last but not least we have the Reserve Bank of New Zealand (RBNZ) interest rate meeting.

Markets remain cautious heading into the new week. Data will no doubt be scrutinized as recessionary fears have not fully abated yet. Chinese data in particular will be of particular interest given the slowdown and recession fears have been sparked somewhat by a slower than expected recovery from the world’s second largest economy.

Asia Pacific Markets

In Asia, China’s major economic data releases are scheduled for the coming week. On Thursday, the People’s Bank of China will set the Medium-Term Lending Facility (MLF) rate.

Additionally, China will release 70-city housing price data and key economic activity figures. A smaller decline in property prices and stabilization in tier-one or two cities would be a positive step in restoring confidence. Retail sales are expected to recover slightly after last month’s post-pandemic low, while industrial production and FAI may also stabilize this month.

Japan will release its 2Q24 GDP on Thursday, expected to rebound to 0.5% quarter-on-quarter seasonally-adjusted (slightly below the 0.6% market consensus). However, this is unlikely to fully offset the 0.7% contraction seen in 1Q24. June manufacturing activity was weaker than anticipated due to another auto safety issue, affecting auto-related sectors. On the positive side, household spending and facility investment should see improvement.

Following the comments by BoJ policymakers it will be interesting to gauge the market reaction to Japanese data as this will be the first set of key data following the rate hike.

Europe + UK + US

Looking to the Euro Area, the US and UK and the calendar comes back to life following a quiet week.

There is a host of UK high impact data which includes the employment data, UK CPI, GDP and Retail sales. The GBP continues to hold the high ground with positive data likely to keep the GBP elevated.

The US also delivers its July CPI data in the week ahead and given the repricing of Federal Reserve rate cuts will be of particular interest. The week wraps up with US retail sales and Michigan consumer sentiment data.

Q2 Euro Area GDP preliminary numbers will also come out this week. This is a key gauge for market participants to keep an eye on as the global growth slowdown weighs on the minds of traders.

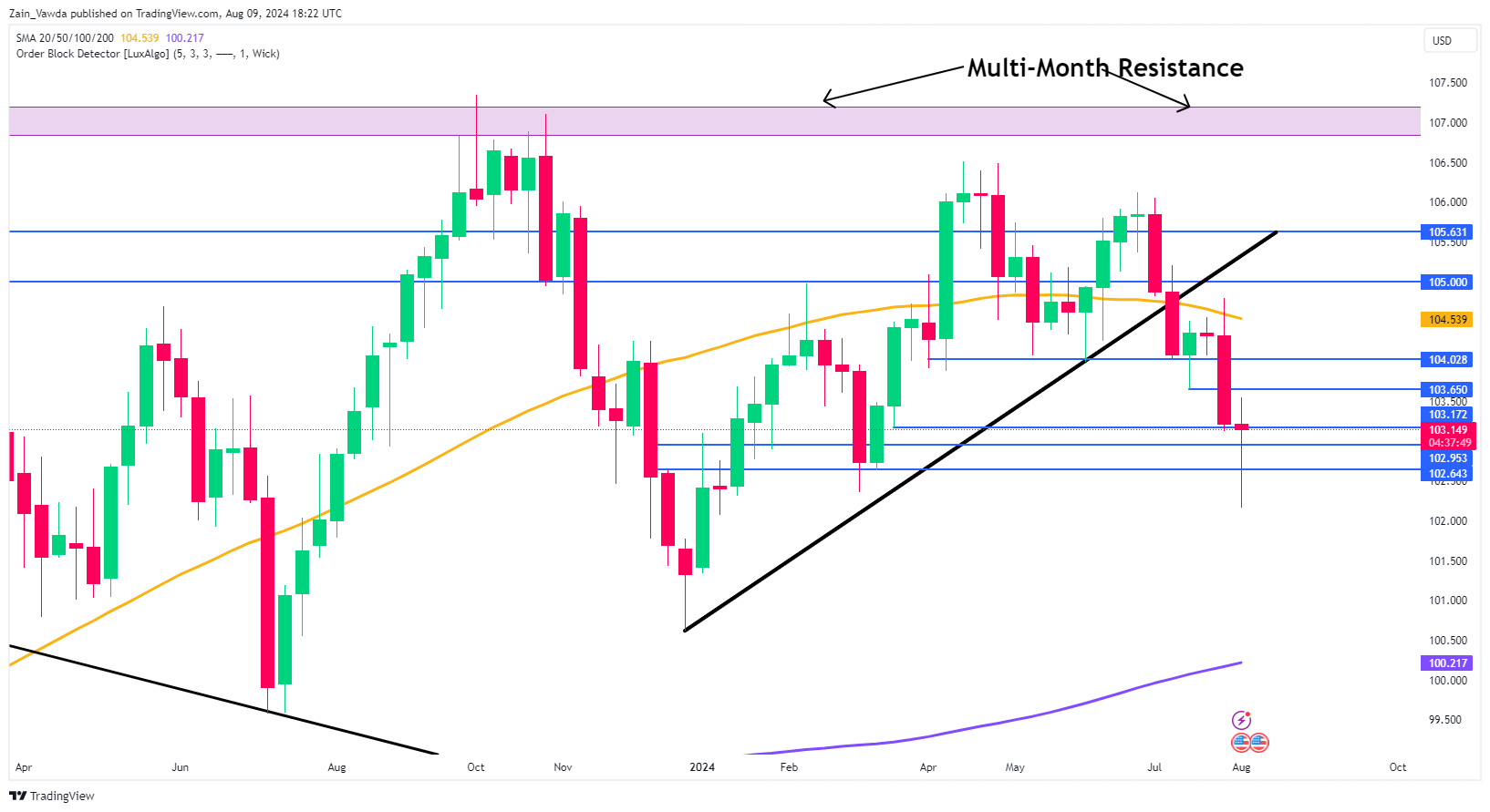

Chart of the Week

The chart of the week I’m focusing on is the US Dollar Index (DXY), which remains a significant force in the financial markets.

After an early week selloff, the DXY has rebounded to trade nearly flat as we head into next week. The substantial downside week is promising for bulls, but the DXY still faces downside risks.

Currently, the DXY is just below key resistance at 103.17, with the next point of interest around 103.65.

A downward move from here would need to break supports at 102.95 and 102.64 before this week’s lows at 100.64 come into play.

US Dollar Index (DXY) Weekly Chart – August 9, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 103.00

- 102.64

- 101.50

Resistance:

- 103.50

- 104.29

- 105.00